In 2021 we saw a big wave of crypto-related companies going public in stock markets worldwide. Miners were listed left, right, and centre along with the second-biggest exchange by volume, Coinbase (according to CoinMarketCap). On top of that, we have many pre-existing companies venturing into the growing sector. Therefore, it's good to look at those companies that stand to benefit from the growth of cryptocurrencies in general. Often times you can find big gains by looking at not the ones in the spotlight but rather the ones that will benefit from someone else being in the spotlight.

Another benefit of buying crypto-related stocks is simplicity. I know Coin Bureau has got you covered with a video on the best tax tools for crypto, but there's no denying that often dabbling in crypto is a lot more exhausting than stocks. I'll go through some of the best crypto-related stocks in this article. I'll try to pick those with high correlation to crypto and those with low correlation but high potential. But before getting into this, I want to emphasize that none of this is investment advice, and I won't be getting into valuations.

Why Should You Consider Buying Crypto-Related Stocks?

You already have a few reasons in the introduction, but I thought I'd elaborate on the first reason a little bit. Let's take as an example the gaming industry. Let's say that games are the core of the gaming industry. That doesn't mean that there aren't any other industries and companies that will benefit from gaming. First of all, we have hardware manufacturers. We need something to play the game on, like a console, phone, or a computer to play the games. Then if we take it a step further, we have those who make the components for those consoles like chip manufacturers.

Furthermore, most of the games played nowadays are online, which means you're likely to need an internet connection to play those games. If we continue this, we could go on forever. However, the important thing to realize is that so many sectors are connected, but naturally, the further to go, the weaker the link. The telecommunication companies won't be as reliant on gamers and game developers as, for example, gaming computer manufacturers will be. Therefore, choosing companies that are somewhat related to another sector can reduce the risk while still being exposed to the industry.

Often the obvious answer isn't the best.

Often the obvious answer isn't the best. The next reason to consider investing in crypto-related stocks is the potential to make additional rewards compared to crypto. Much of this has to do with how the companies are valued. I know I said I won't be talking about individual valuations, but I'll just explain how the extra profit can be found and then it's up to you to do the calculations. Though it's not a company, the best example is the Grayscale. Bitcoin Trust (GBTC). You might have heard that this is now trading at a historically high discount calculated by looking at the market price and the net asset value. This discount opens up the possibility that when prices rise, and GBTC becomes more popular, the discount might erode away, leaving you with whatever gains the underlying asset has made plus the discount. Of course, this doesn't always happen, and it might even be the other way around. However, the possibility that something like this can happen makes it potentially profitable for you as an investor. Companies that can have similar situations like GBTC are, for example, miners.

Crypto Mining: Marathon Digital Holdings

Marathon Digital is the largest publicly traded miner by market cap. Of course, other miners are good too, and some might even be better. However, what makes Marathon Digital stand out from the crowd is its extremely aggressive growth. In 2021 they mined 3,197 BTC, an 846 % increase from the previous year. In December alone, they mined 484 BTC. If you're fast, you calculated that if they continue the December rate, they'll mine a total of 5,808 BTC in 2022. That would already be a significant increase from 2021, but Marathon has something else in mind. Their latest report highlighted that by mid-2022, their hash rate should grow to 13.3 EH/s, and by the end of 2022, it should be up to 23.3 EH/s. That's a tremendous increase considering that currently, they only have 3.5 EH/s deployed.

By doing some simple calculations, we could calculate that if they produced 484 BTC a month with 3.5 EH/s, they could theoretically mine about 3,000 BTC a month with 23 EH/s. That would be 36,000 BTC for the entire year of 2023, and with a price of $40,000 per BTC, it would mean $1.44 billion in revenue. Unfortunately, it isn't that simple. First of all, when more miners join the network, the difficulty in producing one BTC will rise, meaning that you'll make fewer BTC with the same amount of hash rate. Second, we can't be sure that everything in the deployment of miners goes smoothly or that nothing happens to the existing miners. They could either face serious delays due to supply chain issues, or they could potentially decide to purchase even more miners. Thirdly, we have no idea what the price of BTC will be. Naturally, the hope is that BTC will be over $100k, more than doubling the calculated revenue. However, if a bear market hits, the price could go as low as $20,000 or even lower.

Here you can see Marathon's Bitcoin production per mind. As you can see the BTC mined isn't constant even though their hash rate was about 2 EH/s the whole year. Image via Marathon Digital.

Here you can see Marathon's Bitcoin production per mind. As you can see the BTC mined isn't constant even though their hash rate was about 2 EH/s the whole year. Image via Marathon Digital.The point is that the calculations are extremely hard to do since there are many moving factors. However, because of the transparency of Bitcoin in nature, you can consistently follow how the difficulty is adjusted and how miner revenue looks. You can also follow the price of Bitcoin and make assumptions from that. But when doing these calculations, I would always use the lowest number you believe is possible of all variables to avoid any bearish surprises. Don't make calculations based on a BTC price of $500k since it won't do you any good. Instead, prepare for the worst-case scenario. Also, if you want to calculate the profitability, you need to factor in costs. Marathon supposedly has a break-even price of $6000 per BTC, meaning you need to subtract that from the revenue.

Furthermore, I think it's important to point out that Marathon also holds a large number of BTC on its balance sheet. Currently, it's about 8,000, but the expectation would be that they'll keep at least some of their future earnings in BTC. That means that on top of the future earnings, they'll also receive the potential capital gain from Bitcoin, something to consider as well when doing your calculations.

Then lastly, before addressing some risks, we'll look at what analysts think. According to MarketBeat, six analysts are following Marathon, and they all give it a buy rating. In addition, the consensus price target is $55, which leaves a potential upside of 150%. Now naturally, I wouldn't look too much at this since, especially for this stock, there are so many moving variables that I don't think anyone can with any certainty calculate.

As you can see the correlation between Bitcoin and MARA is extremely. However, MARA tends to move even stronger than BTC meaning it should do better in uptrends. Image via TradingView

As you can see the correlation between Bitcoin and MARA is extremely. However, MARA tends to move even stronger than BTC meaning it should do better in uptrends. Image via TradingView I don't believe it comes as a surprise to anyone, but there are many risk factors for Bitcoin miners. The first is obviously the price of Bitcoin, which I already pointed out. The second, and equally as important, is environmental concerns. Marathon is based in the USA. If Bitcoin mining were to be banned due to environmental concerns, it would be catastrophic. However, what's more likely than that is regulations around the use of fossil fuels. According to Marathons latest report, they should be carbon neutral by the end of 2022, which is excellent, but any sudden changes to regulation could mean delays. The third risk is regulation in general. Now we've all heard of the weird legislation going into effect in the US, which would potentially classify miners as brokers and require them to collect KYC from all the transactions, which is impossible. Naturally, legislation like this causes threats to miners, and you need to consider them when analyzing a company.

Bitcoin: MicroStrategy

This is another company often talked about in crypto circles. MicroStrategy is a business intelligence company led by Michael Saylor. However, something which has taken a far more prominent role in the company is its Bitcoin strategy. Currently, MicroStrategy owns 122,478 BTC purchased at an average price of $29,861, according to their investor day presentation last December. That translates to about $4.5 billion at today's prices. On the other hand, their business intelligence business makes about half a billion in annual revenue.

Due to their aggressive investments in Bitcoin, the company's stock almost completely mirrors the price of BTC. Still, there might be opportunities to buy if MicroStrategy falls significantly more than Bitcoin resulting in it trading under its Bitcoin holdings value (kind of like GBTC). That's currently the case; their market cap is only $3.8 billion. However, it's, of course, not that simple. MicroStrategy has a large amount of debt which means not all their holdings are technically theirs, only those left after they pay their debt. On top of that, their debt is also a potential risk. If the price of Bitcoin was to fall a lot, it could cause them to have to file for bankruptcy.

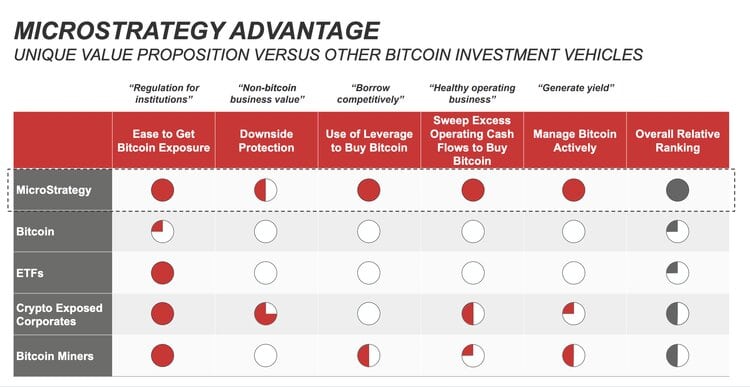

Here are the benefits of holding Microstrategy compared to other Bitcoin related products according to their investor day presentation. Image via Microstrategy Investor day presentation

Here are the benefits of holding Microstrategy compared to other Bitcoin related products according to their investor day presentation. Image via Microstrategy Investor day presentation The positive with MicroStrategy compared to holding Bitcoin itself is similar to what the miners have. Miners produce more Bitcoin when mining. On the other hand, MicroStrategy has an underlying business that produces cash flow. That cash flow can then be used to purchase more BTC. That means that if Bitcoin rises, you'll be exposed to the upside move as well as the additional BTC being produced. However, there is the risk that MicroStrategy is left at a discount since other companies like miners give you the same potential upside.

Crypto Exchange: Coinbase

To quote what Goldman Sachs said about Coinbase, it's "the blue-chip way" to gain crypto exposure, and that seems about right for a plethora of reasons. First, unlike the previous two companies, Coinbase has indirect exposure to many cryptocurrencies. Second, Coinbase is the second-largest exchange based on volume according to CoinMarketCap, which means BTC isn't the only thing traded there. Naturally, BTC and ETH account for a high percentage of all trades. Still, many more cryptos are available, and Coinbase is looking to expand its offering aggressively.

Secondly, Coinbase has multiple revenue streams on top of trading (although that accounts for a significant portion). On top of trading, they have custody services, blockchain rewards, earn campaigns, interest income, and other services. Then if the existing ones aren't enough, they are planning to offer derivatives trading, and they're building an NFT marketplace of their own. Many believe that the NFT platform itself could become a huge business. That's based on the already extremely high volume seen on OpenSea (over $3.5 billion in January). Coinbase also announced a partnership with Mastercard, which will make it possible for customers to purchase NFTs with their Mastercard. That is hugely bullish for both Coinbase and NFTs since it would make them much more easily accessible.

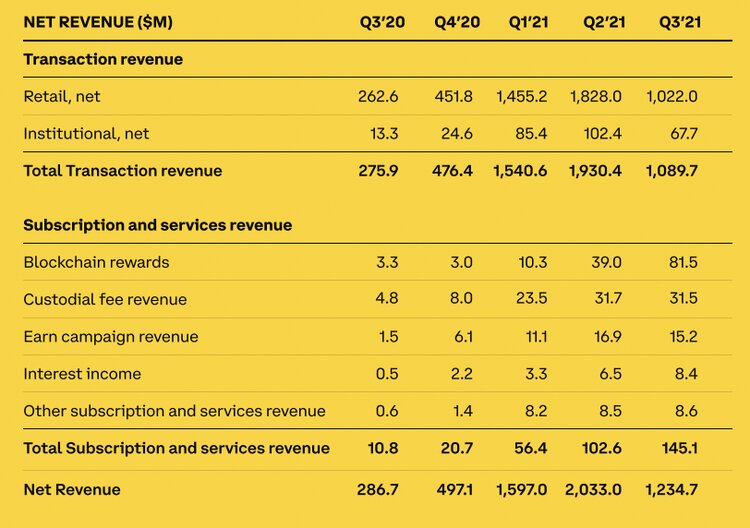

Here's a look at Coinbase's revenue from different sources. What I believe is that the share that comes from trading will be caught up by all the other ventures Coinbase has going on. Image via Coinbase Q3 Earnings

Here's a look at Coinbase's revenue from different sources. What I believe is that the share that comes from trading will be caught up by all the other ventures Coinbase has going on. Image via Coinbase Q3 Earnings As you can see, Coinbase is building a comprehensive offering of crypto-related services, which is why it could be considered a blue-chip. At least that’s what analysts are betting on. As a result, Coinbase has a consensus rating of Buy and a potential upside of roughly 150 %. However, there are more bearish analysts, too, and one of them comes from Mizuho. They believe that Coinbase will face significant headwinds in the mid-term due to low volume in cryptocurrency trading.

That also brings us to the risks of Coinbase. First of all, cryptocurrency is a risk itself. Since Coinbase’s whole business model is around cryptocurrency, it’s one to think about. Secondly, here too, there are strong regulatory concerns. One of the biggest concerns is the SEC going after unregistered securities. Currently, Bitcoin is the only crypto cleared by the SEC which means that many of the coins trading on Coinbase could be considered securities. Now that’s a big concern since an exchange with only Bitcoin isn’t likely to be all that popular. Thirdly, there’s heavy competition from others. There’s no doubt that Coinbase has gotten a slight head start with all the publicity due to its IPO, but there’s also no denying that others are catching up. For example, both Crypto.com and Coinbase have done large marketing campaigns in the US and other countries to gain market share. Meanwhile, Coinbase has been quite shy about informing big-name partnerships.

Payments: Block

Block, formerly known as Square, is the next step from those pure crypto plays. Block consists of 5 different divisions: Square, Cash App, Spiral (formerly Square Crypto), TIDAL, and TBD54566975. The first two divisions account for the majority of Blocks, roughly $13 million in 2021 revenue so far. Square provides commerce solutions, business software and banking services. Cash App is probably known for many, but for those who don’t know, it’s a mobile payment service. I won’t dive into these divisions too much since Spiral is more crypto centred. However, it’s important to understand that those two divisions are the biggest for Block, and those will also be the biggest contributors to the future share price of Block. Both Square and Cash App also play a significant role for cryptocurrency since Square has the opportunity to help merchants accept crypto, and Cash App already allows customers to buy Bitcoin directly from their app.

Also Cash App is active in the crypto industry and many famous sport stars have started accepting their salary in Bitcoin through Cash App. Image via Business Insider

Also Cash App is active in the crypto industry and many famous sport stars have started accepting their salary in Bitcoin through Cash App. Image via Business Insider The leading reason why Block is moving heavily into crypto with all the rebranding and new products is the founder and CEO, Jack Dorsey. Dorsey is known to be kind of a Bitcoin maximalist, and he’s also the former CEO of Twitter and the founder of Twitter. While Dorsey is considered a brilliant person, I immediately have to point out him as a potential risk for the success of Block. Dorsey is driven by his own vision. If he only focuses on Bitcoin, the company might miss out on many opportunities.

My thesis is further backed by what Spiral is doing in crypto. The greetings you get from entering their website is “Making bitcoin more than an investment”, not crypto, rather Bitcoin. However, I’m not saying that what Spiral is doing is terrible; it’s actually the opposite. They have many exciting developments, the latest of them being creating their own Bitcoin mining machines. It’s just that there is more than one cryptocurrency, and others might even be better suited for monetization than Bitcoin. Also, I need to explain what TBD54566975 is; it’s also crypto-related. This division is building an open developer platform to make it easier for others to access Bitcoin and other blockchain technologies.

To have a closer look at these projects offered by Spiral I suggest you visit their website. image via Spiral.

To have a closer look at these projects offered by Spiral I suggest you visit their website. image via Spiral. The strength of Block lies with its existing business and strong userbase. A clear lack in cryptocurrency is user-friendliness, and that's precisely what Block and other payment companies like PayPal can offer. The point with crypto is to eliminate the middleman, but that's not very likely, at least in the short term. Therefore, Block has the opportunity to help merchants with their Square division and consumers with Cash App. Also, these two divisions will live even if cryptocurrency takes a huge beating, meaning that your investment will have some diversification out of crypto. Still, the heavy move towards crypto, or Bitcoin, that Block is doing does mean that you will have good upside since Block isn't that big yet and has a lot of room to grow.

Then lastly, about the analysts and risks. Block gets a consensus rating of Buy and a potential upside of 110 %. The risk with Block is the end to its massive growth, which might impact the share price quite negatively. This is actually seen with PayPal, which just released its quarterly earnings. They predicted slower user growth, and the stock plummeted by almost 20%. Another risk is the already mentioned heavy Bitcoin focused mindset.

Payment Companies: Visa & Mastercard

Don't think there's much need for a thorough introduction, but here's a short one. These two are financial service companies known for their payment cards. The investment case for these is quite similar to what it is for Block with slightly less risk. If Block concluded that the company is likely to survive without crypto, you could rest assured that Visa and Mastercard will be standing and growing without crypto.

Both Visa and Mastercard are huge companies. Visa with a market cap of half a trillion dollars and Mastercard a little behind that with $380 billion. Revenues for the two companies are $21 billion and $18 billion in 2021, meaning they're not that cheap when looking at traditional valuation metrics (price/earnings, price/sales). However, they both have strong positions, and they're unlikely to be shaken off from their market-leading positions. Currently, one viable competitor for both of them seems to be cryptocurrency which makes it logical that they are trying to get in early and capture some value rather than being overrun.

Visa X Crypto.com is probably what most of us think of when hearing Visa and crypto in the same sentence but Visa does have a much bigger role in the industry. Image via Crypto.com

Visa X Crypto.com is probably what most of us think of when hearing Visa and crypto in the same sentence but Visa does have a much bigger role in the industry. Image via Crypto.com Many see their investments in the space as minor compared to the rest of their business, but so is the whole cryptocurrency sector compared to the global payment network. There's no denying that both of these companies are taking aggressive steps in entering the crypto market. To look at Visa first, they have been forming credit card partnerships all over the place, with one of the most used ones being in partnership with Crypto.com. In the last earnings call, it was stated that over 100 million vendors in their network are accepting crypto payments and that in the previous quarter, crypto card transactions grew to $2.5 billion. That's a huge increase and a surprisingly large number compared to the total volume of $50 billion. It's also more than likely to keep growing since Visa is even looking to create a universal payment channel that would support stablecoin transactions from multiple blockchains. This would be extremely bullish since it would allow for near-instant and low-cost transactions regardless of the distance between the sender and the receiver. Currently, it can already be done with cryptocurrency, but as mentioned above, we'll likely need some kind of middleman for some time. And hey, you can't forget that Visa also purchased a Cryptopunk last year.

It's not everyday you see a multi billion dollar company buying a jpeg for $150k, which means I had to include a picture of it. Image via Bloomberg

It's not everyday you see a multi billion dollar company buying a jpeg for $150k, which means I had to include a picture of it. Image via Bloomberg Mastercard has also moved into the crypto sphere. One of their big announcements is the one already mentioned with Coinbase. On top of that, they also have many card partnerships. Last year, when they announced the move to crypto, they stated that they're looking to directly support certain digital assets on their network. They, too, seemed to be quite focused on stablecoins. In the same announcement, they also mentioned that they have multiple patents related to blockchain, which might benefit them in the future. It was also interesting to read that their motivation to start developing in crypto is simply because consumers want it. They have analyzed their networks data and see that their cards are increasingly used for crypto-related purposes. There are two ways to act when you see a trend: either you embrace it and join it (Visa & Mastercard) or deny it until it's too late (many banks).

The crypto-related risks for Visa and Mastercard are, in my opinion, relatively small. The most significant risk I see is that people want to cut these payment services and instead use crypto on the ground level. However, as I've mentioned, that seems to be far away. But there are other risks than crypto-related ones, which is why you should do your own research before investing in any of these companies. Then lastly, looking at what analysts have to offer, Visa gets a consensus rating of 'Buy' and a potential upside of almost 16%. Mastercard also gets a consensus rating of 'Buy' but a slightly smaller upside of just under 10%.

Chip Manufacturers

Nvidia, AMD, Qualcomm, Intel, and others. There are many chip manufacturers, and they're all likely to benefit from cryptocurrency adoption. They're also likely to be the ones who benefit the most from the metaverse. The investment case is quite apparent. We need electronic devices to access both crypto and the metaverse. The metaverse, in particular, will also need high-quality chips for the experience to be seamless.

I mentioned many projects because I'm not a tech genius, and I can't in any way tell you who has the best product for different purposes. Nvidia is by far the most popular when it comes to gaming, and they're likely to benefit from the metaverse and play-to-earn move. But one missed step, and someone else might take the lead, leaving them with outdated chips. Nvidia also needs a separate mention since they have a GPU made explicitly for mining. However, sales for that one dropped significantly after the initial hype. Regardless of the news, it didn't seem to be stopping Intel. Intel is also coming out with its own crypto miner. While these miners seem bullish, they add the proof-of-work risk for chip manufacturers already mentioned with mining companies.

Here's a look at the performance's of these stocks. As you can see Nvidia and AMD have outperformed Qualcomm and Intel by a lot. Image via TradingView.

Here's a look at the performance's of these stocks. As you can see Nvidia and AMD have outperformed Qualcomm and Intel by a lot. Image via TradingView. I believe that chip manufacturers will benefit increasingly from the digital transformation we’re making, and cryptos are part of that. Nowadays, everything has the word “smart” in front of it and contains some kind of chip. Naturally, more demand for chips means more supply needs to be provided. But, as I already mentioned, I can’t tell which one will be winning, and that’s the biggest risk for all of these companies. We’ve seen companies like Apple starting to use their own in-house chips rather than those from Intel. Does this mean Apple will produce chips on a larger scale in the future? Maybe, maybe not, but there’s a risk it will happen.

Conclusion

There you have a handful of crypto-related stocks. Naturally, there are a ton more out there, and new ones are coming all the time. For example, as mentioned, there are multiple different mining stocks, and I strongly recommend you look into many of those before making any decisions. Then for Block, I would view PayPal as a suitable replacement if you like that one more.

Lastly, to look at the example I gave earlier where you can move further away while still having exposure to the wanted asset, this could have been done even further than I did here. However, the effect is negligible when you go too far, and there’s no point in me rambling about those companies. Take as an example Alphabet (parent company of Google). They’ve formed some partnerships in the blockchain and crypto space. Their other businesses are also likely to benefit from the metaverse and crypto to some extent. However, to an almost $2 trillion market cap company, the effects of crypto are relatively small, and the investment from a crypto standpoint is quite pointless.

This was what I had to say, and now it’s up to you to go and do your own research on the companies I’ve listed here and see if you find any of them worth the investment.