To the uninitiated, cryptocurrency begins and ends with Bitcoin. This isn’t entirely surprising. Bitcoin grabs most of the headlines, with its moves to ever-greater all-time highs and its adoption by the likes of Tesla and PayPal.

It gets bankers hot under the collar and has books written about it. It’s the most evangelised of all the cryptos, with a seemingly endless procession of fervent disciples falling over themselves to proclaim it as the saviour of humankind. To them and plenty of others, Bitcoin is the original and still the best.

Once you delve a little deeper into crypto though, you’ll quickly notice that not only are there thousands of other projects out there, but that one name in particular crops up time and again. It won’t be long before you come to realise that Ethereum is behind much of what is going on in crypto besides Bitcoin. There is, in fact, a strong case to be made for Ethereum being as important a project as Bitcoin and perhaps even more so.

Image via Shutterstock

Image via Shutterstock A glance at the likes of CoinGecko will show you that Ethereum has a market cap second only to Bitcoin’s and is some way clear of its nearest rivals in this regard. But to view Ethereum and its native ether (ETH) coin as the second biggest crypto is to massively underestimate the whole project.

ETH is only one part of what Ethereum is about: this is not merely some altcoin we’re talking about here. The Ethereum project’s ambitions, what it has achieved so far and what it hopes to achieve in the future, make Bitcoin seem a little one-dimensional by comparison.

Crypto’s Base Layer

The world of crypto has been throwing up plenty of stories recently. Yes, there’s all the Bitcoin-related hoo-ha, but also the explosion of decentralised finance (DeFi) and the recent frenzy around non-fungible tokens (NFTs). These latter two talking points owe their existence largely to Ethereum, which has for years been providing the platform for thousands of other crypto projects to build on top of.

Ethereum was conceived and built to be a complete crypto ecosystem, offering a blockchain that could host all manner of other platforms and currencies. On its website, Ethereum describes itself as ‘a technology that’s home to digital money, global payments and applications,’ that functions as a ‘digital economy’ in its own right.

Ethereum's landing page. Image via Ethereum.org

Ethereum's landing page. Image via Ethereum.org The technology that Ethereum has developed has spawned thousands of projects already, with more appearing all the time. Indeed, many of the biggest and most valuable crypto projects and tokens - some with multi-million dollar market caps themselves - run on the Ethereum network. While Bitcoin concerns itself with the storage and transfer of value, Ethereum is geared towards the creation of value and the continued growth of the cryptocurrency space.

Yet for all its success, Ethereum is facing some daunting challenges. It has become bloated by its sheer functionality, with its network slowing to a crawl under the weight of all the traffic it is having to handle. Change is coming, though seemingly at a snail’s pace. All the talk now is of Ethereum 2.0 – the next iteration of this almighty project that, it is hoped, will help it achieve its full potential.

This piece will look at what is expected of Ethereum 2.0 and why it is so hotly anticipated by the crypto community. We’ll examine the problems it is intended to fix, what its implementation could achieve and why we’re still waiting for it to go live. But before all that, we need to take a closer look at the current state of the Ethereum project, as well as examine its history and what it has achieved so far.

Ethereum: A Potted History

The Ethereum project was first outlined in 2013 by a nineteen-year-old programmer named Vitalik Buterin. This absurdly precocious Russian-Canadian university dropout is now a legend of the crypto space, despite being still only in his twenties. Buterin conceived Ethereum with the idea of bringing a ‘general-purpose flexibility’ to the blockchain, his aim being to build a platform that others could use to build their own programs and applications.

The V-dawg himself. Image via cnbc.com

The V-dawg himself. Image via cnbc.com Several other figures were involved in the founding of Ethereum, the most notable being Charles Hoskinson (later the founder of Cardano) and Dr Gavin Wood (author of Ethereum’s Solidity programming language and later the founder of Polkadot). These two both left the project because of differing opinions as to how it should proceed.

The Ethereum network went live in July 2015, in the wake of a crowdfunding round the year before. Wood’s contribution was instrumental to the network, as it was he who designed the Ethereum Virtual Machine (EVM), ‘the environment in which all Ethereum accounts and smart contracts live.’ The ins and outs of the EVM are too complex to be detailed here, but it essentially allows for these aforementioned smart contracts to be written, which in turn, allows for applications to be built on Ethereum.

Smart contracts are important to understand as they have limitless potential and astronomical use cases as they allow traditional sectors to be ported into blockchain. To learn more about them, check out our educational piece: What are Ethereum Smart Contracts.

Smart contracts are self-enforcing and they function in a similar way to a vending machine. Put in some money, select a product and the machine dispenses it. Programmers are able to write smart contracts which can then form the basis of programs and applications running on top of the Ethereum blockchain. Again, the complexity of smart contracts is a matter for a more in-depth piece, but the important thing to know is that Ethereum is designed to allow developers to use its network for their own projects.

Image via Shutterstock

Image via Shutterstock This functionality enabled Ethereum to grow rapidly, as projects flocked to use its platform. The ETH coin was designed to be used by these developers to pay for their usage of the network, though Ethereum was designated as a non-profit by Buterin in 2014. As the network grew in popularity, so ETH began to be used more by all of those developers and users interacting with Ethereum. This usage is what propelled ETH’s value upwards, despite the coin having no fixed supply.

Dapps, DeFi and Stablecoins

Projects that run on Ethereum are known as decentralised applications (dapps), which function in the same way as the apps we know and use every day, but with no single point of authority. By using Ethereum’s blockchain, they are able to store transaction history and other data immutably, without having to resort to the expensive process of building their own blockchains.

The field of dapp development has grown rapidly since Ethereum’s inception and thousands of projects now have dapps running on the network. Dapps have flourished in a number of sectors, most notably finance, technology, gaming, art and collectables. These dapps are sometimes referred to as being part of Web3 – the next iteration of the internet in the age of blockchain.

Uniswap Trading Volumes on the rise. Image via Uniswap

Uniswap Trading Volumes on the rise. Image via Uniswap Dapps now offer everything from crypto-based financial services to online games and virtual worlds. They can be used for web browsing, betting, buying art or streaming music. Many Ethereum-based dapps have become big-hitting crypto projects in their own right, helped in large part by another aspect of Ethereum’s platform: the ability to create and issue other tokens.

As a result of this functionality, dapps can launch their own tokens using Ethereum’s ERC-20 token standard. These tokens run on Ethereum’s blockchain but can be traded on the open market along with most other cryptocurrencies. As a result, many of the top 100 cryptos (and plenty others besides) are tokens that run on the Ethereum network. These include projects like Tether (no.4 at the time of writing), Uniswap (no.8) and Chainlink (no.10) meaning ERC-20 tokens are traded in huge volumes every single day.

Ethereum’s popularity as a developer blockchain has put it at the forefront of the decentralised finance (DeFi) revolution, which has seen thousands of projects spring up to challenge the world of traditional finance. DeFi essentially eliminates financial middlemen, allowing people to conduct financial transactions in a peer-to-peer manner, with no cut being payable to intermediaries.

Image via Shutterstock

Image via Shutterstock 2020 saw an explosion in DeFi’s popularity, with new users pouring money into protocols that let them take out loans, loan out their crypto to others, trade coins and tokens on decentralised exchanges and much more besides. The DeFi sector now has over $41 billion locked into it and every one of the top protocols runs on Ethereum.

The Ethereum network is also heavily used by those trading and using stablecoins – cryptocurrencies pegged to the value of a real-world currency (usually the US dollar) or other assets. These pegged values help mitigate much of the risk involved with trading other, more volatile cryptos and their use has become increasingly widespread.

According to a recent Consensys report, three-quarters of all stablecoins now run on Ethereum, with the network handling over $1 trillion in transactions in 2020. Once again, much of crypto’s heavy lifting is being done by just one platform.

Riding the NFT Wave

More recently, it’s been impossible to avoid all the hype surrounding non-fungible tokens (NFTs) which have been making headlines for commanding some truly insane prices.

NFTs are digital tokens representing digital assets. They’re stored on a blockchain and contain an immutable record of who owns them. They’re built using smart contracts and can be coded so that, when sold on, a proportion of the sale price goes to the original creator, even if they aren’t the seller at that time. As such, many artists and musicians are taking advantage of them to sell their works – again without the need for intermediaries.

Image via Shutterstock

Image via Shutterstock Opinion is divided over NFTs. Some see them as a promising step towards putting power back into the hands of creators and rewarding them properly for their work; others view them more as a sign that Satan and his legions may finally be at the gates. There’s no denying however, that, once again, Ethereum is the driving force behind this new crypto sector.

Two new Ethereum token standards – ERC-721 and ERC-1155 have been developed to create NFTs, while most are bought using ETH and are stored on the Ethereum blockchain. It seems that every new innovation in crypto has Ethereum humming away in the background.

Too Popular for its Own Good

Ethereum has had its share of setbacks. A hack in 2016, which exploited a weakness in one of the projects built on top of it, resulted in $50 million worth of ETH being stolen. The decision was taken to split the Ethereum blockchain (a process known as a hard fork) in order to recover the stolen funds. The fork became known as Ethereum Classic and the project still operates to this day.

Hacks and hard forks are part and parcel of life in crypto and Ethereum emerged relatively unscathed from its encounter with them. More pressing however is the extent to which the Ethereum network is now buckling under the strain of all the traffic it is having to handle.

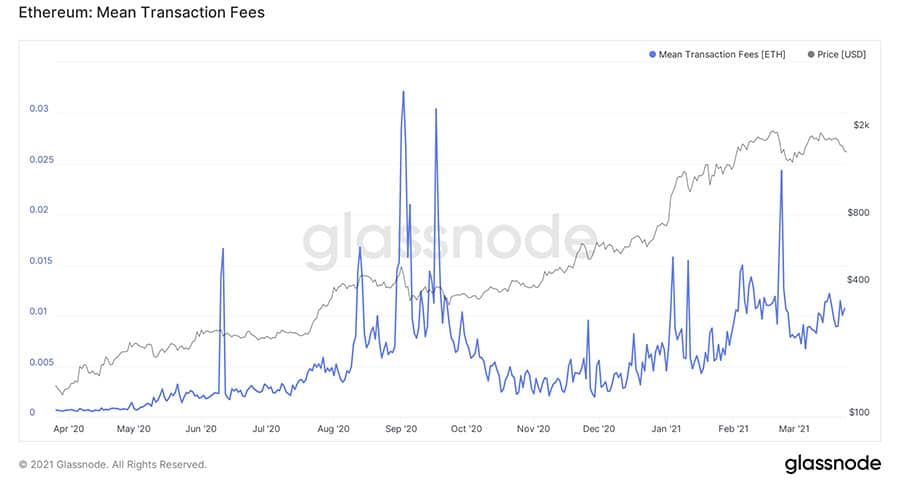

Transactions Fees through the roof. Image via glassnode.

Transactions Fees through the roof. Image via glassnode. This problem has become so acute that the Ethereum network can become unusable at times. Transaction speeds have slowed to a crawl (the network can only handle 15 transactions per second) and the fees payable to have these transactions executed (known as ‘gas fees’) can be astronomical at times of heavy usage. In short, Ethereum has become a victim of its own success, weighed down by all the users it has attracted in its short life span.

This state of affairs has been going on for some time and has led to the creation of a number of projects that are seeking to knock Ethereum off its lofty perch. These ‘Ethereum killers’ include the likes of Charles Hoskinson’s Cardano and Gavin Wood’s Polkadot, both of which are developer blockchains similar to Ethereum but designed with far higher transaction capacities and the ability to handle more traffic.

As early Ethereum developers, both Hoskinson and Wood could see that the project was going to suffer scalability issues as it grew. While neither Cardano nor Polkadot is ready to challenge Ethereum’s dominance just yet, they are built without Ethereum’s flaws and will continue to grow if Ethereum isn’t able to get its house in order soon.

Understanding Ethereum’s Problems

By now you’ll have read the word ‘blockchain’ several times over the course of this piece alone. If you’ve spent any time in crypto, you’ll have heard it a whole lot more. Blockchain technology underpins all cryptocurrency. It provides a means to safely store and record all the transactional and historical data of a crypto, while ensuring that it can never be tampered with. Thus the integrity of the system is maintained and dishonesty made all but impossible.

The Bitcoin Network distributed across numerous nodes. Image via Shutterstock

The Bitcoin Network distributed across numerous nodes. Image via Shutterstock The most well-known blockchain is, of course, Bitcoin’s. A network of individual computers (nodes) is spread across the globe and each node verifies every transaction that takes place on the network. When a certain number of transactions have been verified, they are grouped together into a block.

In order to keep the network secure, each block is encoded with a long sequence of letters and numbers, known as a hash. Each block carries its own hash and a copy of the hash of the preceding block. These matching hashes enable a new block to be added to the chain. When a new block is produced, the user that created it is rewarded with a set number of bitcoins. These block producers are known as miners and the process of deciding on which miner creates a new block is known as network consensus.

To arrive at the matching hash involves solving a complex mathematical problem, which can only be done using brute force computing power. The more power a miner uses, the greater their chances of solving the problem first and being able to mine the new block. This is why many have expressed concern about the vast amount of electricity the Bitcoin network uses.

This method of achieving network consensus is known as proof of work, with the work in question being the computing power expended to arrive at the matching hash number.

Bitcoin’s code was written so that the complexity of the problems to be solved to create a new block increased as more blocks were mined. As a result, the Bitcoin network has become slower and more energy-intensive as its popularity has grown. The proof of work consensus mechanism has become obsolete as Bitcoin has grown.

The Ethereum network is now suffering from similar problems to Bitcoin’s because it too uses proof of work to achieve network consensus. High demand and heavy traffic have made blocks on Ethereum harder to mine, meaning the whole process has become slower and more expensive.

Ethereum miners need to use more power to produce blocks and thus let the network move forward, meaning that the gas fees they charge have become higher. The result is a network that slows to a crawl when lots of people are trying to use it.

These are the problems that Ethereum 2.0 is designed to solve.

ETH 2.0 – Let’s Get Going

To bring Ethereum into the mainstream and serve all of humanity, we have to make Ethereum more scalable, secure, and sustainable.

This is Ethereum’s stated aim for ETH 2.0 and an acknowledgement that the current state of the network is inadequate. The process of upgrading Ethereum to ETH 2.0 is a long one and not due to be completed until next year. It has been divided into three separate stages, which we will examine in a minute. Before that, we need to understand the new type of blockchain consensus mechanism that Ethereum is moving to.

We’ve already noted the drawbacks to a proof of work blockchain. In order to combat this wastefulness and inefficiency, Ethereum is moving towards becoming a proof of stake (PoS) blockchain – one where consensus is achieved in a much more efficient and less intensive way.

Image via Shutterstock

Image via ShutterstockOn a proof of stake blockchain, those nodes that want the chance to mine new blocks and claim the rewards can stake their crypto for a chance to become what is known as a ‘validator.’ This works much like a lottery: the more tickets you buy (the more you stake) the greater your chance of winning. One validator is then chosen at random to mine the new block and claim the reward, which is usually a cut of all the fees paid for the transactions contained within the block.

This way of achieving consensus eliminates the need for multiple miners to use huge amounts of power in order to be allowed to mine a new block. However, Ethereum’s switch to this new system is not straightforward and will be conducted in three discrete stages.

Stage 1: The Beacon Chain

This first stage actually went live in December 2020, generating considerable excitement in the Ethereum community and beyond, as the switch to ETH 2.0 seemed finally to be underway.

The Beacon Chain is focussed on allowing staking to take place on Ethereum – this will then allow stakers to run validator software and participate on the PoS blockchain. The Ethereum team are hoping to attract as many validators as possible, in order that control over the network is not concentrated into the hands of too small a number of validator nodes. This decentralisation will, it is hoped, address the issue of network security.

The Beacon Chain’s staking functionality will also help pave the way for the next stage of ETH 2.0, which will rely on a PoS system being in place in order to work.

Stage 2: Sharding

In order to improve Ethereum’s scalability and allow it to handle more transactions, extra chains, known as shard chains, will be introduced in order to lighten the load of the main chain. The plan is to eventually have 64 shard chains running in parallel, thus vastly increasing the amount of traffic the network as a whole is able to handle.

Sharding. For all we know, this is exactly what it'll look like. Image via Ethereum.org

Sharding. For all we know, this is exactly what it'll look like. Image via Ethereum.org The shard chains will eventually be randomly assigned validators by the Beacon Chain. This will further increase network security as no two validators would be able to collude to take over a shard. The spreading out of the network over these shard chains will not only enhance speed and security, but should also eventually allow people to run an Ethereum client from a laptop or smartphone, thus securing the network still further.

Sharding is expected sometime this year, ‘depending on how quickly work progresses after the Beacon Chain is launched.’ Once in place, this will allow for the final stage of ETH 2.0 to take place.

Stage 3: The Docking

Both the Beacon Chain and the shard chains will run separately from the Ethereum mainnet, which will continue to use a proof of work consensus. The docking will join the mainnet with the Beacon Chain and the shard chains, finally moving the whole Ethereum network to a PoS consensus.

This coming together of all aspects of ETH 2.0 will see the good ship Ethereum made ‘ready to put in some serious lightyears and take on the universe.’ Insert theme from 2001: A Space Odyssey here.

The docking; last but not least. Image via Ethereum.org

The docking; last but not least. Image via Ethereum.org This final stage of Ethereum’s long-awaited upgrade is expected to take place either towards the end of this year or in early 2022.

To Infinity… and Beyond?

Amidst all the excitement of Bitcoin’s price increases over the last year and the bull market the whole crypto market has been enjoying, it hasn’t gone unnoticed that ETH’s price has skyrocketed too – up an astonishing 1,200% since this time last year. This dwarfs Bitcoin’s 850% rise and reflects the importance of Ethereum to the entire crypto universe.

Much of ETH’s rise can perhaps be attributed to prevailing market sentiment, with crypto as a whole enjoying a boom year while the rest of the financial world came close to imploding. Yet much of ETH’s continued success can be put down to excitement about the coming of ETH 2.0 and it’s no surprise that the price really started to climb after the rollout of the Beacon Chain in December.

ETH over the last year. Image via Coin Market Cap

ETH over the last year. Image via Coin Market Cap The fact is that anyone with a decent working knowledge of crypto knows how big Ethereum has become and how central it is to so much of what is going on in crypto. Half the projects out there probably wouldn’t exist without it and any balanced portfolio is almost certain to hold at least one asset that runs on Ethereum.

Perhaps the best indicator of Ethereum’s success is the number of projects that are looking to take it on, as it huffs and puffs its way towards its new dawn. Cardano and Polkadot have been mentioned already, but Algorand, Stellar, Tezos and NEAR Protocol are amongst others with an eye on Ethereum’s crown. The original smart contract blockchain cannot afford to rest on its laurels.

ETH 2.0 has been a long time coming and we’re not there yet. Despite some fixes being made to the network in the meantime (watch Guy's recent video if you want to learn more about them), Ethereum is still some way off from fulfilling its massive potential.

But, assuming the careful rollout of ETH 2.0 goes according to plan, Ethereum looks set to scale new heights in the years ahead. There is a palpable sense amongst many in crypto that the best is yet to come: at least, those who aren’t too busy shilling Bitcoin.