How Interest Rates Impact Everything

With rampant inflation happening around the world, one of the ways often used to curb that inflation is interest rates. It is one of the few tools available to bring down demand to balance it more accurately with supply. Interest rates have both a direct and indirect impact on our daily lives. We hope that, by the end of the article, you will have gained a broad understanding of the impact of interest rates in almost all aspects of the economy. That includes the various asset classes for investment, including crypto. You'll also get some insight into how your own decisions are affected by interest rates (whether you are aware of it or not), and what you can do to take advantage of the current rising rates.

Why are Interest Rates Important

Before we dive in to understand its importance, let's start with the basics. Interest rates are the cost of borrowing money, expressed as a percentage of the loan amount. essentially it is a charge to the borrower for the use of an asset. Some sources have expressed interest rates as the "cost of money".

Interest rates, by themselves, don't affect the economy as much as you think. It's the combination of interest rates and credit that affects the economy. Credit is something created out of thin air between a lender and a borrower. When someone agrees to pay back a loan, that's when credit is created for that transaction. When the loan is paid back, the transaction is considered settled, and the credit disappears. If you'd like to find out more about how the economic machine works including the role of credit, there's a great video made by Ray Dalio that explains it in a clear manner.

That said, the volume of lending and borrowing is very much dependent on interest rates. In order for an economy to be healthy, there needs to be a certain level of lending and borrowing happening at any given time. This is because people usually borrow money to do things with, such as invest in a business, buy an asset, etc. This creates demand, which in turn creates supply to meet the demand. However, if there's too much borrowing and not enough is paid back, then we have a problem.

Interest Rates for Consumers

As a consumer, interest rates affect the financial decisions we make, mainly in whether we will save or borrow. Low-interest rates encourage us to make better use of our money through spending or investing while high-interest rates make it a no-brainer to save more. When we spend, money circulates within the economy, passing from one pair of hands to the next. When we save, money is deposited into a bank or it gets invested.

It's important to note that money doesn't just sit in the bank as a deposit. The bank will use it to lend to others. However, high-interest rates result in less borrowing, which reduces the probability of the money being loaned out. This results in less money floating around in the economy.

On a personal basis, it may influence our spending habits as we may spend less and decide to save more when rates are high. When rates are low, we are more inclined to spend more because money is considered cheap. If we're looking to buy a big-ticket item, we may defer buying it when rates are high as borrowing is expensive. We might want to put more money in as a down payment on the upfront cost so that we won't have to borrow as much.

Those who already carry some kind of debt are incentivised to pay off their debt as quickly as they can when rates are high. Low rates mean that debt repayment is slower because people may feel that the money is better used elsewhere rather than to pay off the debt.

Interest Rates for Businesses

As a business owner, business decisions often revolve around the factors that can bring in more profit or cut costs. One thing influencing these factors is the current interest rate. It's no exaggeration to call it an invisible hand that guides businesses. This is because the kinds of activity undertaken or choices available largely depend on what interest rates are prevailing.

If the business wants to expand operations, buy new equipment or hire more staff to meet demand or anticipate future demand, these actions are best done when interest rates are low. Aside from expansions, consumers are apt to spend more when rates are low, which brings forth new demand, setting the business on a positive cycle. Listed companies may even see their share price rise due to good profits.

When rates are high, not only would the business not be taking on more debt, but it would also want to pay down existing debt as quickly as possible without affecting profit margins, because it costs more to pay the debt. Sometimes though, businesses can't afford to make payments on their debts when interest rates are too high, even if the increase is only 1% or less. When that happens, they might even have to look for ways to cut costs, including letting staff go, which further exacerbates the situation.

The reason for this is that high rates do not encourage spending by consumers, which leads to declining demand and even less need for supply. Henry Ford is well-known for the sentiment of wanting his own workers to be able to buy the cars they make. When your own staff can't afford to buy the products you make, assuming it's not luxury items, you know that things are pretty bad.

Interest Rates for Investors

Investors look at money as a product and the cost of money is interest rates. The basic cost is the Ten-Year Treasury Notes rate, also known as the risk-free rate. Shares and other assets are usually seen as riskier assets in comparison, thus the investor would like their investments in those areas to generate higher returns than what is given by the Treasury Notes. The rate of return from these assets is known as the risk premium. If the Treasury rate is 2%, and investors want to get at least 4% from shares, then the total rate of return they need is 6%.

What affects the risk premium may also be affected by interest rates. As we saw in the consumer's behaviour, higher rates lead to less demand, hence less supply. When that happens, the share price of the company falls due to less profit. There are also other factors affecting the risk premium such as a capable staff in the top management team resigning, or a company having trouble servicing its debts.

The cascading effect brought on by the rise and fall of interest rates is something that investors are very much concerned with when evaluating the investments on hand or what to invest in the future.

Interest Rates and Countries

When we view interest rates through the lens of a country, the decisions being made are influenced by different factors compared with those affecting consumers. In essence, there are three main areas of concern:

Central Banks and Interest Rates

A nation's central bank is the bank of banks. It is where banks go to borrow money. The central bank is also in charge of determining the interest rates used in the country. This figure is what banks would get for deposits and pay for borrowing money from the central bank. It is also used as a guideline by the banks to decide how much they will offer to lenders and charge borrowers.

When the central bank sets a high interest rate, it incentivizes consumers to deposit money into the bank. This is because you can get a decent yield from bank deposits, which is pretty much risk-free money. The desired effect leads to money taken out of circulation from the economy, thus decreasing the amount of money available to be used. Less money floating around equals less money chasing for goods, so prices go down and inflation is kept in control. Most central banks around the world agree that it's better to err on the side of inflation, thus a 2% inflation rate is a common target for central banks.

If rates are too low, it may look good for the economy as people spend more, leading to economic growth. However, it's also very easy for things to tip over, leading to over-borrowing, or over-leveraging. An example of that is using a 20% down payment to get the mortgage for your first house, then using the first house as collateral to get your second house, and before you've finished paying the mortgage for both, you decide to take on a third property using both houses as collateral. If you want to find out more about how leveraging works to disastrous effects, check out Guy's video on the Evergrande property crisis.

Another way for the central bank to keep the economy chugging along is the privilege of being able to create money out of thin air. They do that by printing money, which used to be a physical act of churning out new dollar bills. Nowadays, it's just a matter of a few clicks on a computer. The essence of the act remains the same.

This is an important point to take note of because that "printing" increases the amount of cash chasing for goods currently in circulation. Most goods aren't produced as quickly as it takes for the extra cash to appear in the economy. Eventually, there will reach a point where there is more cash available to pay for things. This is how inflation happens.

How smoothly the economy runs is in large part influenced by the decisions made by the central bank. What makes the job of the central bank tough is how to strike the optimal balance so that there isn't too much or too little money sloshing around in the economy. Too little credit could stifle growth but control inflation while too much credit is good for the economy but encourages inflation.

As we continue to look at the other areas affected by interest rates, you will also see the actions and options available for central banks to take to deal with these issues.

Fiat Currencies and Interest Rates

If there was ever a classic example of "I say so" money, it's fiat currencies. This is because each country has its own currency that is only valid for its own borders, but mostly useless outside those borders. The exceptions here are the U.S. dollar and the euro, which we'll touch on later.

However, it's not always been like this because currency used to be backed by gold. A paper bill is only worth as much as its printing cost. What gave it value in the past was that it could be exchanged for gold at a certain rate set by the government. When the gold standard was abolished, what backed the currency was the economic strength of the government. What gives a government strength is its perceived ability to set sound economic policies, keep the national debt at manageable levels, and ensure the health of the governmental bond market, to name a few. Aside from economic considerations, other factors such as the government's ability to protect the country's borders and its citizens are also taken into consideration.

The local currency of each country is also a product that is traded in its own market, known as the Forex market, short for Foreign Exchange. The buying and selling of currency is a trillion-dollar business and interest rates play a big role here. Each trade always involves a pair of currencies since you need one kind of currency to buy another kind. Carry trades, as they are known, is when buyers buy a high-interest currency against a low-interest currency and earn a daily interest between the difference. What makes a currency considered high or low interest is also relative to the currencies of other countries.

It's fair to say that while everyone is primarily focused on the health of their own countries, everyone also keeps an eye on what their neighbours or competitors are doing when it comes to setting interest rates. This is because countries also compete for foreign cash investments with each other. In order to attract foreign investment, rates are lowered, making investing in that country attractive. Conversely, rates are raised to stop money from flowing out of the country.

Global Trade and Interest Rates

All countries import and export goods with each other. What they import is not necessarily something they don't have or produce, it could be that what they produce could be sold for a higher price and they can import the cheaper version for internal use. However, some countries are in a position to import more than they export and the reverse is true for others. Import-driven countries need their currency to be on the high end so that the goods they buy will be cheaper. Export-driven countries, on the other hand, need a low currency so that what they produce is affordable to other countries.

At this point, we need to talk about the world's reserve currency, which is the U.S. dollar. Since much trade is carried out using U.S. dollars amongst countries, the closer a currency matches the U.S. dollar, the stronger it becomes. This is good news for the importers but bad for the exporters. Countries that stack up weakly against the U.S. dollar need to use more of their own currency to buy things for their citizens. In some cases for export-heavy countries, they have a vested interest in keeping their currency weak against the dollar so that their products are more saleable to other countries. Combined with low-interest rates, countries with a strong currency are tempted to purchase more as it can be seen as a kind of discount. However, this is also a delicate balance because it would also make their own imports expensive.

What's clear is that it's important for every country to have a healthy balance of U.S. dollars in their national coffers. In a worst-case scenario, you run into a situation like Sri Lanka, where the national coffers don't have enough U.S. dollars to buy fuel and other necessities. Guy did a video about the Sri Lanka's situation and what it means for the rest of us if you would like to find out more.

The strength of the U.S. dollar is determined by the rates set by the Federal Reserve, which is the central bank for the U.S. A strong U.S. dollar also makes it difficult for nations to service their debt to other nations since they need to use more of their local currency to pay down the debt. The U.S. is also the no. 1 creditor nation worldwide, i.e. they lend the most money to other countries. When U.S. interest rates go up, not only do other countries need to worry about paying debts to other nations, they also have to worry about their own debt to the U.S. This is why when the Fed announces rate changes, the world listens.

Speaking of the world's reserve currencies, there have also been some fierce debate about a different kind of currency replace the U.S. dollar , one that's more government-agnostic. If this is of interest, you can check out our article on whether it's possible for bitcoin to become the world's reserve currency.

Interest Rates and Investments

Interest rates have a direct impact on all forms of investment. First of all, it affects how much money goes into investments. The higher the rates, the less money is available for risky assets. In a strong economy, marked by low inflation and high job security, people are more inclined to invest as there is more disposable cash on their side. The inverse is also true. We'll look closer at how three areas of investments are affected by the rise and fall of interest rates.

How Interest Rates Impact Stock Markets

Interest rates affect the stock market in two ways: through the share price and through the effect on investors.

You might have noticed that anytime a hike in interest rates is announced, the stock market will usually experience a drop. How precipitous the drop is depends on whether the increase has been anticipated by the market. If everyone expects an increase of 1% and the announcement says 1.5%, the drop will be a lot bigger. If the actual rate increase is less than expected, equity markets might remain about the same or even have a mini-rally. This is because the signal being given suggests that things aren't as bad as expected, thus there is no need for a big hike.

When interest rates are high, borrowing money becomes an expensive activity. Companies need to get more profit to service their debts. This makes it less profitable for investors. High-growth stocks, including small companies, start-ups, and companies that use borrowed funds to fuel growth, get hit the hardest. At the same time, the high-interest rates dampen demand, thus generating less business for companies, which means the share prices don't go up as much. Another bad piece of news for investors.

Companies that are more established or have a larger war chest, are able to weather high-interest rates better. Their debts remain serviceable without eating too much into profits, and while they are also affected, the disruption is less intrusive compared to companies that rely on high leverage borrowing.

Oddly enough, although most people are familiar with the mantra of "buy low, sell high", when share prices fall, it's not many that are willing to pick up what could be bargain deals. Perhaps the reason is that they may not have the cash to buy these stocks as they might be busy servicing their own debt or doing some serious budgeting for their own finances.

Another reason could simply be attributed to human nature, driven primarily by fear. When stocks start falling in a high-interest environment, no one wants to buy too soon because they are waiting for the bottom. When will the bottom arrive? No one knows.

Not only that, there is also fear that some businesses might not make it out alive. This makes investors less inclined to invest in them, not wanting to throw good money after bad. Yet it's precisely these times that one can see the real backbone of a company. Those who truly believe in the company's ability to weather tough storms and vote with their wallet might see great returns when the storm passes over. Companies will also have to prove that they have what it takes for that trust to not be misplaced.

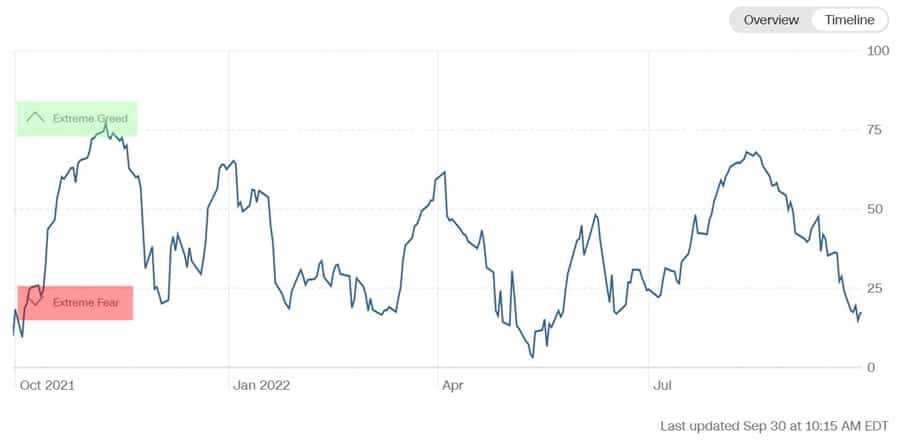

This see-saw of emotions oscillating between fear and greed is played out most obviously when interest rates are running hot. A sneak-peek at the Fear and Greed Index pretty much sums up the whole story.

Extreme fear creates opportunities, extreme greed means time to sell.

Extreme fear creates opportunities, extreme greed means time to sell.

Interest Rate Impact On Bond Markets

Any mention of bond market usually brings to mind one of two: the governmental bonds and those issued by private companies. The former makes up the lion's share of the bond market while the latter is but a smaller portion. Regardless, bonds usually do quite well in a high-interest rate environment. This is because bond yields rise with rates, and they are usually seen as a safe alternative to stocks.

Governmental bonds are the most risk-free investments you can make. You're basically lending the government money and it promises to pay you back based on a pre-determined time including some interest. During WWII, wartime bonds were a popular offering and a way for the government to raise money instead of raising taxes.

It's been a staple in many investors' portfolios, representing the safe part of their investments. However, with the low rates prior to 2022, bonds were considered a terrible investment as they paid next to nothing. When inflation came along and rates weren't up yet, it was like losing money and made quite a bit of a dent on the more conservative portfolios. When interest rates started going up, that's when bonds felt less like the losers they were a few years ago. Needless to say, rising interest rates are good for the bond market because people see it as a good place to park cash.

When it comes to company bonds, the story is slightly different. Instead of lending money to the government, you're lending it to the company. Bear in mind that the price of bonds is not about the future growth of the company issuing them, but the interest rate of what the bond pays. The growth of the company is important insofar as it signals the probability of the company being able to pay back the loan within the appointed period.

The interest rates for short and long-term bonds, whether for government or companies, differ - as they should. The former offers less yield than the latter. In the kind of environment we find ourselves facing currently, where every few months brings about fresh new rate highs with a healthy ladle of uncertainty thrown into the mix, short-term bonds might be a good place to park some extra cash. Use it to weather any rate changes and once the money is available, you can rethink your strategy and see what you can take advantage of in the current environment.

Interest Rate Impact On Cryptocurrencies

As an asset class, cryptocurrency is considered high-risk due to the speculative nature of the asset. The thing is, anything can be a cause for speculation. What makes some assets more suitable for speculation than others is the basis for the speculation to occur. As long as there is some factual foundation to rest on, speculation can grow as high as what people are willing to believe or extend their imagination to. Where there is speculation, the greater fool theory follows closely behind, and that's where profits can be made.

Crypto represents one of the latest in financial technology that can bring about improvements with the potential to upend how society operates as we know it. That in itself is fertile ground for speculation to grow and thrive.

Of course, announcements about rate hikes affect crypto in a fashion similar to the stock market. When interest rates are high, the appetite for speculation is dampened as there is less of a need to put oneself out on a limb to chase high yields. When rates are low, and if coupled with high inflation, people feel like they have nothing much to lose, thus are more willing to be involved in risky activity. This in turn affects the market pricing for the assets. The sentiment is best characterised by the Crypto Fear and Greed Index.

Interest Rates and the Housing Market

Without a doubt, interest rates play a major factor in the housing market. Prices rise when rates are low and stop rising, or even fall, when rates are high. Very simply, people think twice about buying a house when they look at how much is required to service the mortgage. Affordability is the first thing under consideration, followed by the measurement of risk and reward. How much will the price of the property have gone up by the time I'm ready to sell? Would it be enough to cover the costs of owning the property?

Once upon a time, a down payment made for a property could be as high as 30% (or more), while the interest rate charged to borrow the rest could go up to 15%. In those days, the general assumption is for people to buy what they can afford while also having a reasonable time to pay back the loan, which will then enable them to enjoy the property for the rest of their days.

As interest rates got lower, and house prices got higher, people were encouraged to take on more debt while requiring less upfront money. Even if they are able to pay off the mortgage sooner than anticipated, low-interest rates might prompt them to rethink how best their money can be allocated to good use. This is all well and good. However, when interest rates go up, it changes the equation a fair bit. Not only does the cost of the mortgage payments go up, but whether the debt itself is serviceable also gets thrown into question.

Interest rates also greatly affect property investors. Just like any other business, what they can get in credit by leveraging their assets as collateral is determined by how costly it is to borrow and repay the loan. The best-case scenario is to borrow when it's cheap and to have paid it all back (or at least most of it) by the time the rates go up.

How Interest Rates Impact Inflation

Inflation, in the most basic sense, is when you have too much cash chasing for the same amount of goods. At this point, it's important to make a distinction between value and price. The price paid for an item does not necessarily reflect the value of the item. Part of the value comes from the cost of producing it. Inflation affects the price but not the value.

When interest rates are high, people might not choose to deposit the money into the bank but instead use it to invest in other things. This is because they believe they can get a better return than what they get from the bank. As we all know, every investment comes with risk, some bigger than others. Usually, investments with higher risk come with greater rewards. The least-risky option is bank deposits. If that's the case, then money still remains in circulation which does nothing to alleviate inflation. When that happens, the central bank has no choice but to keep raising interest rates, hoping to suck more money out of the system.

On the other hand, that same interest rate is also the basis for what borrowers need to pay back for the loan. If the interest rate is at 1%, the rate for borrowing could be 3%. Repaying a loan also takes money out of circulation because the money goes back into the bank. You can imagine people having a hard time paying back their loans if the interest rates are too high. And too much money taken out of the economy can lead to deflation, which is also undesirable.

Some of you might wonder: why 3% Why not 2 or even 1.5% for the borrowing rate? That's a valid question. The answer is that this affects credit in the economy. As we read earlier, credit is something that can stimulate the economy by creating demand which leads to supply meeting the demand. Too little credit and the economy runs the risks of stagnating whilst too much credit forms bubbles in the economy.

Conclusion

One of the invisible factors buffeting us in modern times is interest rates. What we see in the form of bank rates is but the tip of the iceberg. Almost every economic activity is influenced by it as it is the cost of money. Our everyday lives are also shaped a fair bit by it, whether we like that or not. One thing that can help us is to go with the flow and let our actions be guided by the gentle nudging coming from the rates. Where possible, have some spare cash around to pick up some good investments. While some may be of the opinion that cash is trash, in the short-term, it's still very useful and to have some sitting in the bank is not a bad idea. Sometimes, maximizing what you have may lead to the opposite result when interest rates go up. Planning for both low and high rates is the safest bet in the long run.

Frequently Asked Questions

Interest rates influence individuals' saving and spending decisions in an indirect manner. They may consider whether to spend or save more based on whether the rates are low or high. High rates encourage saving, low rates encourage spending.

Not necessarily. Interest rates are a tool like any other. It's how people react to the interest rates and their subsequent behavior that may or may not bring on undesired or unintended outcomes. Too much money floating in the economy leads to inflation, which is bad in general. Therefore, high-interest rates let people think twice before borrowing and also encourage saving.

When this happens, the most immediate effect is that people don't borrow as much because borrowing becomes expensive. Those who already have debt would be inclined to pay them back faster, if possible. If interest rates remain too high, then the economy is also in danger of slowing down because people would spend less, which leads to lesser demand and in turn, less supply. It could also lead to a deflationary situation, which is also undesirable.

Yes, they do. High-interest rates make investing in cryptocurrencies a higher-risk activity than if the rates are low. This is because, in the game of chasing yield, people are less likely to deal with riskier assets when the presumed reward does not outweigh the risks involved. If a similar yield can be obtained with less risk, people are likely to go with the less-risky option.

Disclaimer: These are the writer’s opinions and should not be considered investment advice. Readers should do their own research.