If I had to choose the one area that excites me the most in crypto, I would have to say DeFi. As much as I love GameFi and Metaverse projects because they are innovative and well…fun, they are an entertaining convenience, not a necessity. Unless our collective society is happy to accept another 300 years or so of being taken advantage of by the legacy financial system, and billions of people are content with not having access to a bank account, we need a revolution, we need DeFi, which makes me excited to be bringing this Euler Finance review to you today.

A Brief Intro to DeFi Lending and Borrowing

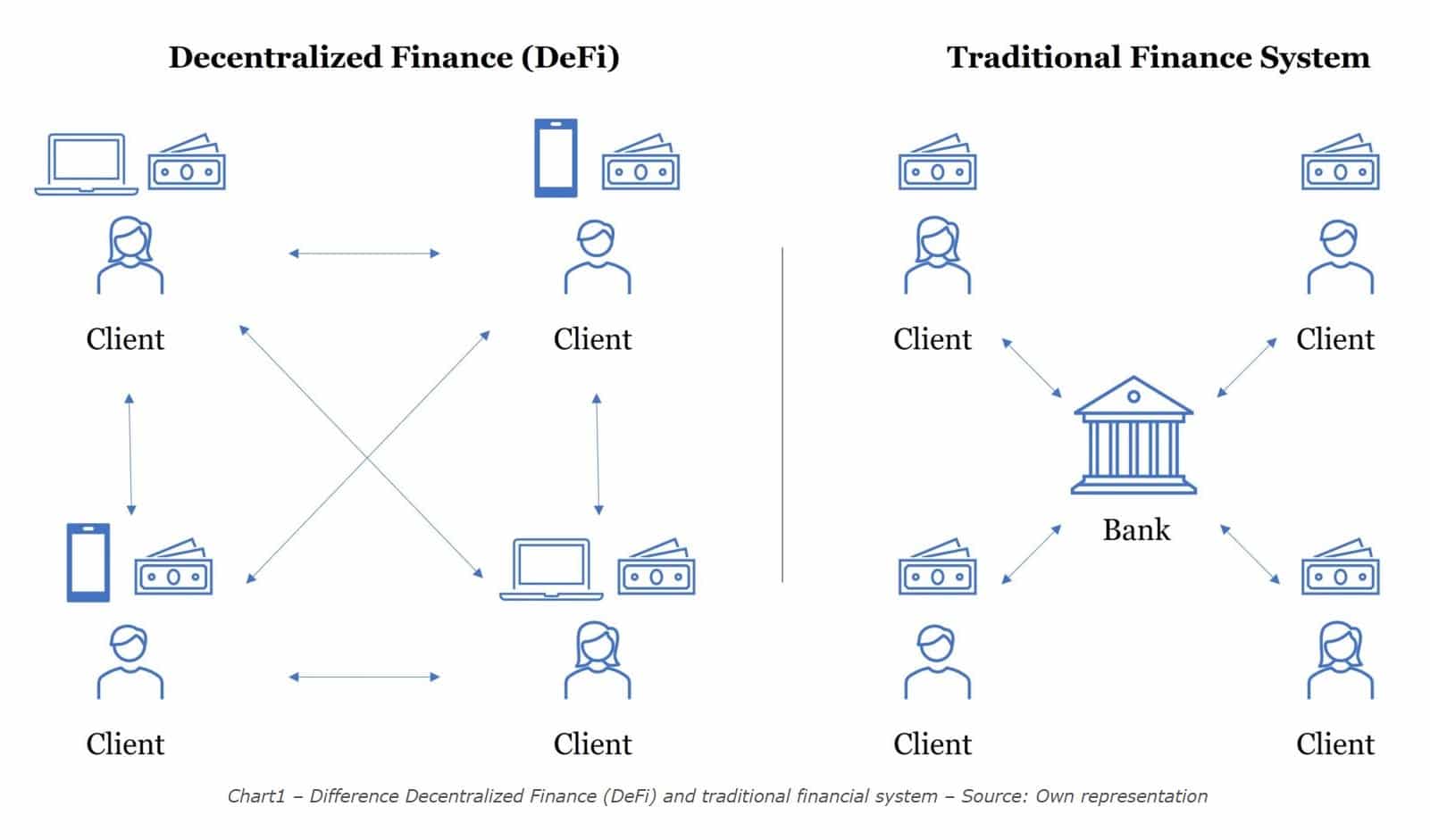

The ability to lend and borrow assets efficiently is a key cornerstone of any financial system. In the world of traditional finance, the process is typically facilitated by trusted and permissioned third-party banks and institutions. These banks essentially enslave borrowers and become the financial overlords over people who need to come crawling to them for borrowing purposes.

Okay, dramatics aside, that was the old way of doing things and now we have better solutions with DeFi protocols such as Aave, Compound Finance and Euler Finance. In the world of DeFi, trusted and permissioned third parties are no longer needed, the banking overlords have been replaced by trustless and permissionless lending protocols running smart contracts on the blockchain. This makes for an exponentially more efficient process for lenders and borrowers to meet the needs of one another while cutting out the significant fees charged by third parties and the draconian restrictions often imposed on us by centralized authorities.

Here is a great graphic from MoreThanDigital that sums up how this looks:

Image via morethandigital.info

Image via morethandigital.info

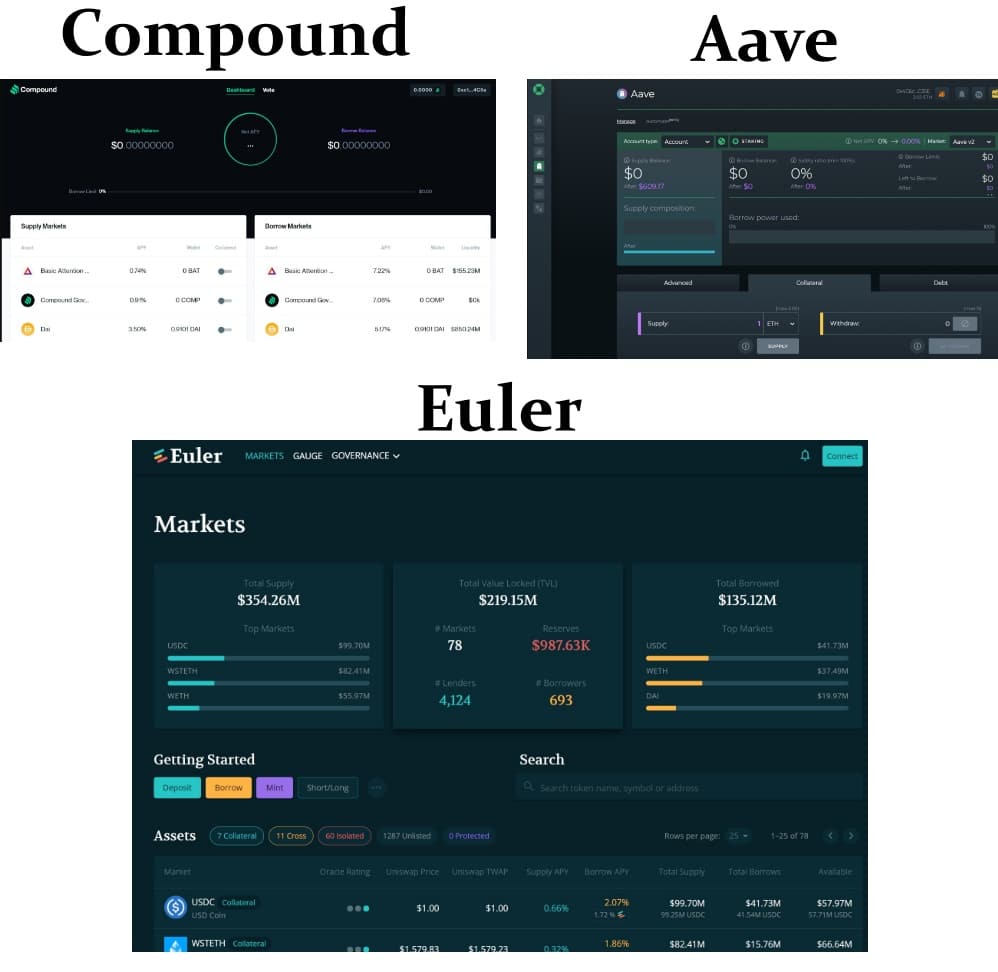

Protocols like Compound Finance and Aave were among the first generation of DeFi lending protocols. These platforms provide users with access to lending and borrowing functions for multiple crypto tokens. Now, being first-generation comes with some pros and cons. The power of “first-mover advantage” cannot be understated, but the flip side of the coin is that the first iteration of a software, technology, or idea is usually not the best, there are usually plenty of kinks and bugs to work out. This leaves plenty of opportunities for other teams to evolve and innovate upon the initial framework, which is exactly what the Euler Finance team has done.

I’m not saying there is anything wrong with Compound or Aave, in fact, I use Aave, and they are both fantastic platforms, but these protocols were not designed to handle the risks associated with lending and borrowing illiquid or volatile assets. I don’t know if this is because they could not figure out a way to effectively reduce the risk of the extreme amount of volatility that exists in our markets, or if they were not prepared for the sheer amount of trading volume or demand for trading pairs that they are not able to accommodate for, but the result is that they have to rely on a permissioned listing system to protect their users from the risks associated with such assets. This is one area Euler realized they could vastly improve upon.

A Look at Compound, Aave and Euler

A Look at Compound, Aave and Euler

The result of a permissioned listing system led to a significant unmet demand for lending and borrowing crypto assets. Lenders want to deposit tokens to earn yield and take leveraged long positions, while borrowers want to reduce exposure to volatility and take out leveraged short positions. This is where Euler Finance comes in and builds on the foundation laid by the first-generation lending platforms and aims to become a next-gen DeFi Protocol. They have achieved this by supporting permissionless listing and providing reactive interest rates all while reducing risk in never before seen innovative ways which we will explore in detail.

What is Euler Finance?

As we already touched on, Euler Finance is a Decentralized Financial lending platform on the Ethereum network that has built on and improved upon the lending platforms that preceded it.

The team named the company and protocol after Leonhard Euler, who was a Swiss mathematician, physicist, astronomer, geographer, logician and engineer who founded studies of graph theory and topology. He also made influential discoveries in many other branches such as analytic number theory, complex analysis, and infinitesimal calculus. Wow, brilliant guy! I find myself proud on a good day when I can manage to tie my shoes, floss, write an article, walk the dog, and cook up some Mac n' Cheese. This guy puts me to shame!

A Look at the Euler Finance Homepage. Image via euler.finance

A Look at the Euler Finance Homepage. Image via euler.finance

Anyway, Euler Finance was created in December 2021 after the company behind it won the Encode Club’s ‘Spark’ University Hackathon which helped the team secure $800k during a seed round with prominent backers such as Lemniscap, LAUNCHHub Ventures, Block0, Coinbase and more. On June 7 2022, Euler announced another funding round worth $32 million led by Haun Ventures, which will be used to diversify the Euler DAO treasury, leading to a fairly well-funded project.

Euler XYZ, the company behind Euler Finance, was founded by Dr Michael Bently, Jack Leon Prior, and Doug Hoyte, who will be covered later on in the team section. Euler finance provides a permissionless, non-custodial lending protocol that is custom-built with an array of new and ingenious features to help users swap, lend, and borrow more types of tokens than were traditionally available.

The protocol supports the borrowing and lending of nearly every ERC20 crypto asset, something not supported on other platforms, while offering the ability to earn interest on users’ crypto with less risk and volatility than was previously possible through their innovative technology stack that we will cover later on.

Image via euler.finance

Image via euler.finance

Euler Finance is free to use and can be accessed by anyone in the world with an internet connection. Like any DeFi protocol worth its weight in salt, it is completely non-custodial and managed by the community who are holders of the protocol’s native governance token EUL.

The platform can be accessed at https://app.euler.finance/, and something that is quite cool is that the original developers encourage new developers to create their own front-end access points to the protocol to help decentralize access and increase censorship resistance. The caring and sharing of open-source software and lack of authoritarian money-hungry developer communities that exist in the world of crypto always gives me a warm fuzzy feeling.

Pro Tip: Though I provided the URL to the platform above, it is always a good idea to ensure you double-check the web address and always access any DeFi protocol from the company website or whitepaper to ensure you are using the correct URL. Once you have the right platform, you should bookmark it to ensure you always navigate to the correct one to avoid the multiple scam sites out there that mirror the original platform.

Alright, let’s dive into the features and functions of Euler Finance.

Euler Finance Features:

This next part will highlight the important features and functions of Euler Finance. There is a lot to unpack here as the team has developed some pretty impressive protocol mechanics that deserve digging into, so take this time to go grab yourself a cup of your favourite drink before diving in ☕

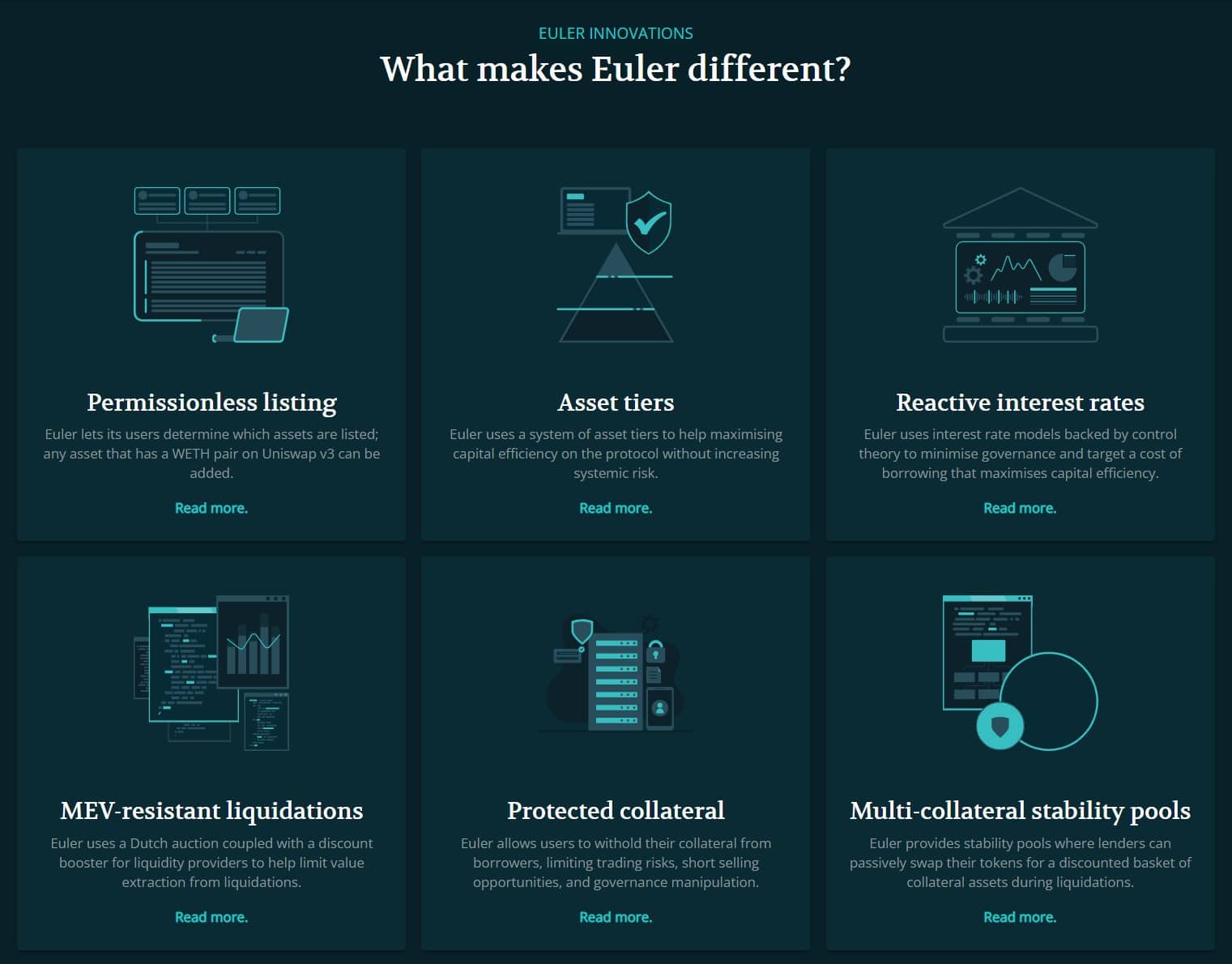

Euler Finance: Permissionless Listing

Euler’s non-custodial protocol allows its users to decide what crypto assets it will list. By using Uniswap v3 as a core dependency, any asset that has a WETH pair can be added as a lending market on Euler by anyone instantaneously.

Euler Asset Tiers

Now, for anyone with their DeFi smart kid hat on, permissionless listing may be ringing an alarm bell as you may or may not know that permissionless listing is far riskier on decentralized lending protocols vs other DeFi protocols like DEXs.

This is because of the potential for risk to spill over from one pool to another in quick succession. If a collateral asset suddenly decreases in price and liquidations fail to repay borrowers’ debts, the pools of multiple different types of assets can be left with bad debts, which is no bueno. (That’s Spanish for not good!)

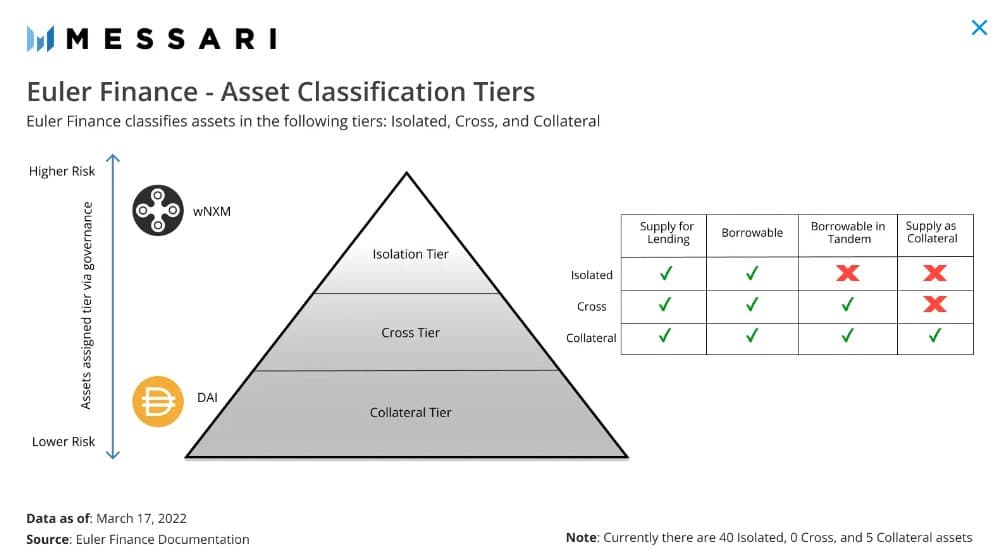

To overcome these risks, Euler uses risk-based asset tiers: Collateral, Cross, and Isolated, to protect the protocol and its users:

Image via Euler

Image via Euler

Isolation-Tier - Assets in this tier are available for ordinary lending and borrowing, but cannot be used as collateral to borrow other assets. They can only be borrowed in isolation, hence the term, “Isolation tier.”

This means that they cannot be borrowed along with other assets using the same pool of collateral.

Huh? Let’s look at an example:

I have USDC and DAI as collateral and I want to borrow isolation-tier asset 'ABC'. I can only borrow ABC and nothing else. If I want to borrow another token, 'XYZ', then I could only do that using a separate account on Euler.

Cross-Tier - Assets in this tier are available for ordinary lending and borrowing and cannot be used as collateral to borrow other assets but can be borrowed alongside other assets.

Need another example? I think so:

If I have USDC and DAI as collateral, and I want to borrow cross-tier assets 'ABC' and 'XYZ', I can do it from a single account as I can borrow more than one type of token that is in the cross-tier category.

Collateral-Tier - Assets in this tier are available for ordinary lending and borrowing, cross-borrowing, and can be used as collateral. These would be the most liquid assets with the most trading volume on the platform, and therefore, deemed the “safest.”

Let’s have an example:

I could deposit collateral assets DAI and USDC and use them to borrow collateral assets like UNI and LINK all from a single account.

By using this tiered method, different risk assets are siloed which helps reduce contagion effects, so one high-risk token with a small market cap in the isolation-tier cannot crash more well-established asset pools. Essentially, this method increases maximum capital efficiency while keeping systemic risk at the lowest possible level.

Image via Messari.io/euler-finance

Image via Messari.io/euler-finance

EUL holders can vote to promote assets from the Isolation-tier and move them to the Cross-tier or Collateral-tier through governance mechanisms. Promoting assets up the tiers increases capital efficiency on Euler as it allows lenders and borrowers to use capital more liberally, but may also expose protocol users to increased risk, so it is in everyone’s interests to balance the risks.

Euler Finance: Lending and Borrowing

When lenders deposit into a liquidity pool on Euler, they will receive interest-bearing ERC20 eTokens in return, which is standard practice across DeFi protocols. These tokens can be redeemed for their share of the underlying assets in a pool at any time as long as there are unborrowed tokens in the pool.

A Look at Accessing Lending and Borrowing on Euler

A Look at Accessing Lending and Borrowing on Euler

Borrowers take liquidity out of a pool and pay back borrowed funds with interest, resulting in the total assets in a pool growing over time. This is how lenders earn interest on assets as their eTokens can be redeemed for an increasing amount of the underlying asset over a period of time. Nothing new or ground-breaking here, this is the tried-and-true method behind DeFi lending and borrowing. This process is all handled through smart contracts, making it quite seamless and user-friendly.

Next, we will cover the different components involved with borrowing.

Tokenized Debts

Euler issues dTokens to tokenize debts similarly to Aave’s debt tokens. The dToken interface allows the construction of positions without needing to interact with underlying assets and can be used to create derivative products that include debt obligations.

Instead of providing non-standard methods to transfer debts, Euler uses the regular transfer/approve ERC20 methods but reverses the permissioning logic.

I know, sounds complicated but it isn’t, here is an example of how that works:

Rather than being able to send tokens to anyone, but requiring approval, as is the standard method, dTokens can be taken by anyone, but require approval to accept them. This prevents users from “burning” their dTokens. The zero address has no way of approving an in-bound transfer of dTokens.

As you would expect, borrowers pay interest on their loans. The interest accrued depends on the algorithmically determined interest rates for each asset. A portion of the interest accrued is held in reserves to cover the accumulation of bad debts on the protocol, adding another layer of security.

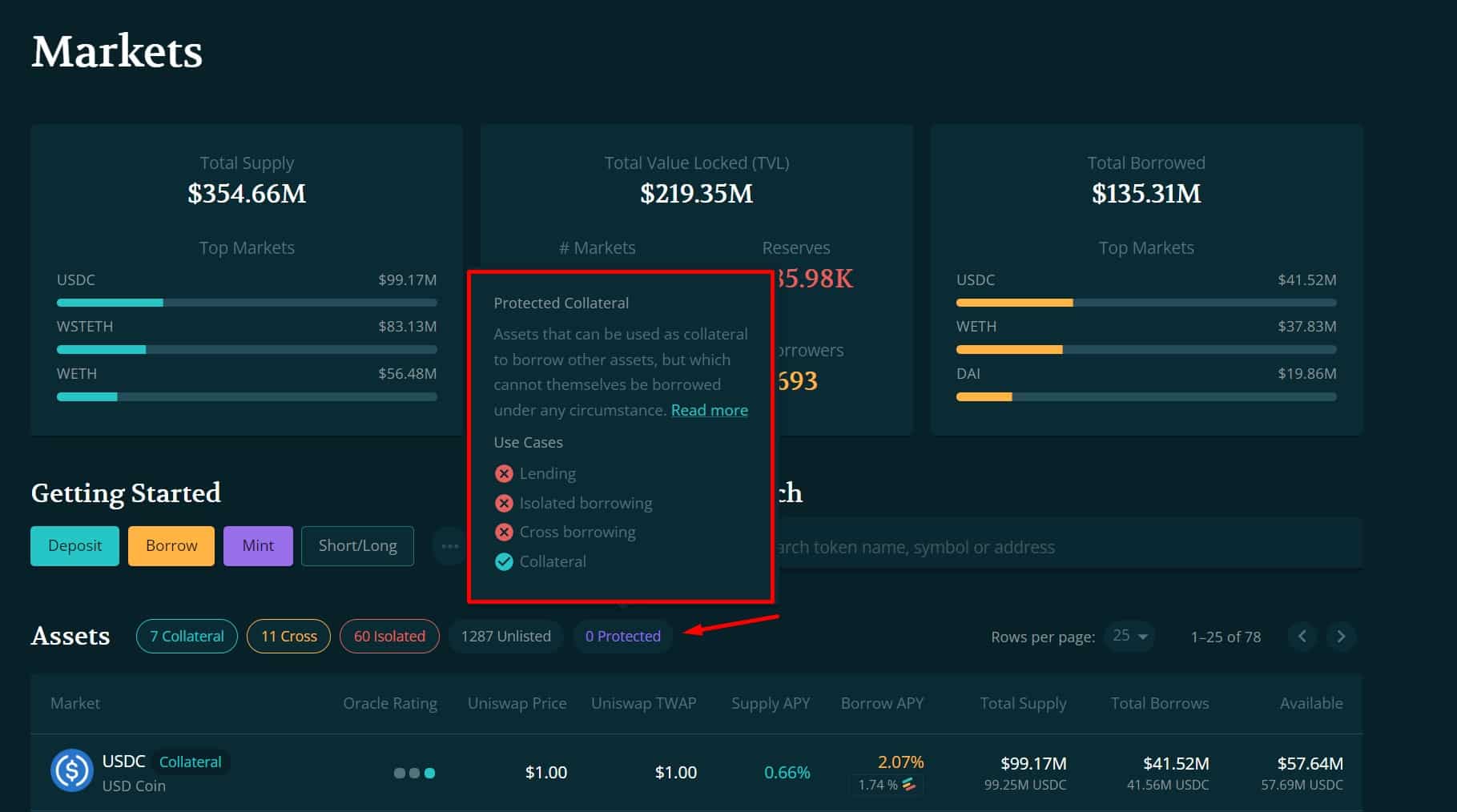

Protected Collateral

This is one of the features that is quite unique to Euler. On Compound and Aave, any collateral deposited on the protocol is always available for lending. Euler allows collateral to be deposited, but not necessarily made available for lending.

Image via Euler

Image via Euler

This is a convenient feature as depositors don’t need to withdraw funds from the platform if they choose to take a break from lending. Funds in protected status do not earn interest, but are free from the risks of borrowers defaulting and can be withdrawn at any time instantly. This also helps protect against borrowers using tokens to influence governance decisions or take short positions.

Why is this an important feature?

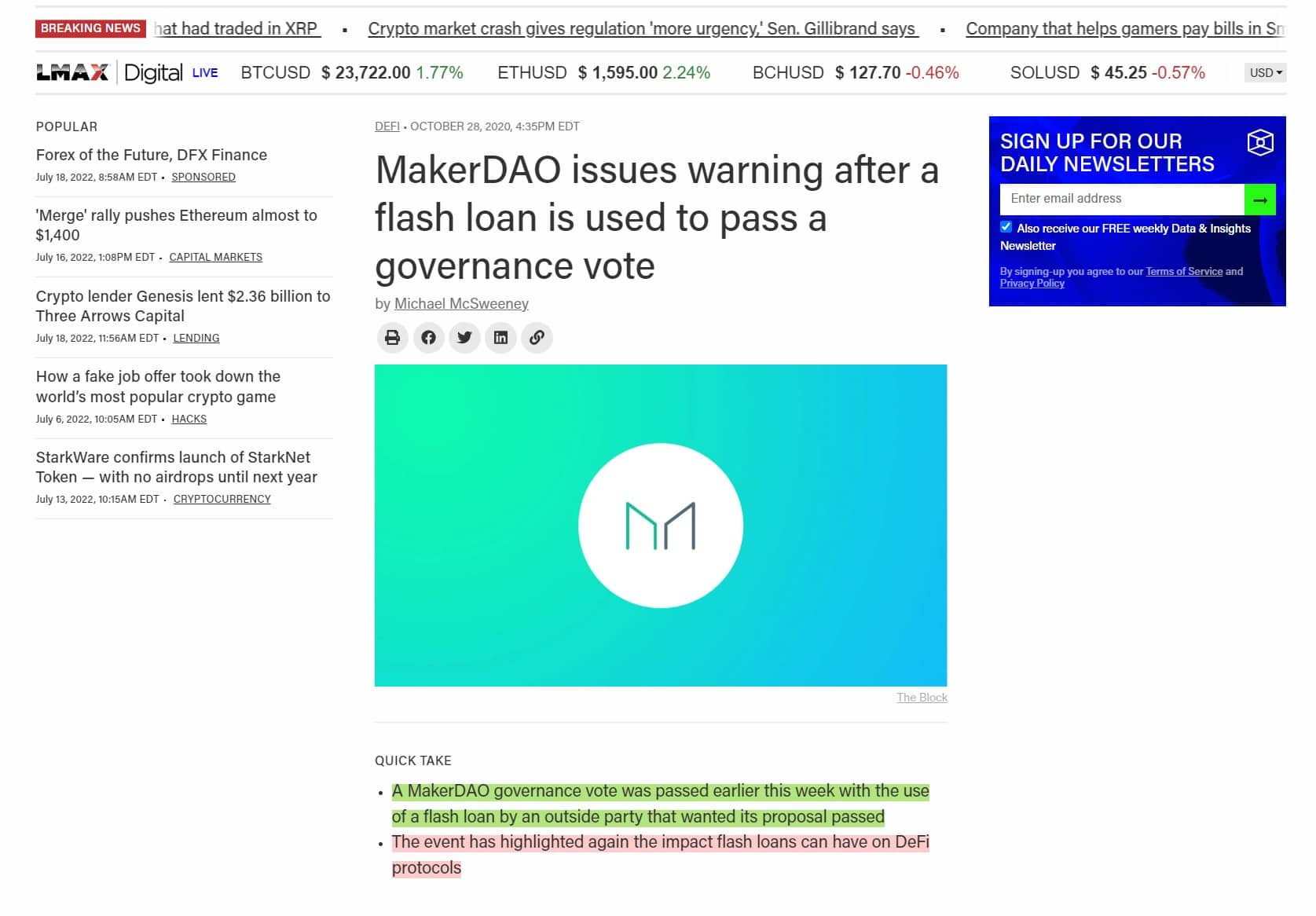

Well, aside from convenience, this also provides a valuable use case for those who truly care about the industry and DeFi community as a whole. In 2020, MakerDAO experienced a flash loan scenario that was used to unfairly pass a governance vote.

Image via theblock

Image via theblock

So, say there is a big governance vote coming up on a platform, Euler users could protect the assets needed to vote on the proposal, preventing whales from borrowing a boat load of those tokens then swaying a vote in their favour. This helps result in a fairer democratic governance process. This feature can also be used to help prevent intense selling pressure, pump and dumps, flash loan attacks, and death spirals.

Defer Liquidity Checks

This is another innovative feature on Euler that I have not come across before with other lending platforms. Normally, an account’s liquidity is checked immediately after performing an operation, leading to an action that could fail due to insufficient collateral.

For example, borrowing, withdrawing collateral, or exiting a market could cause a transaction to be reverted due to a collateral violation.

Again, that would be no bueno.

Euler has a feature that allows users to defer their liquidity checks which can allow many operations to be performed with the liquidity check being done only once at the very end.

Let’s look at how this is beneficial for the user:

Without deferring a liquidity check, I would first need to deposit collateral before issuing a borrow action. However, if done in the same transaction, deferring the liquidity check allows me to do this in whichever order I choose, allowing for more flexibility and a less rigid structure, while also potentially saving on wasted gas fees on failed transactions.

This allows users to be able to bundle a set of actions with the end result being a healthy position, but a particular action within that sequence may not have been feasible on its own. This allows for actions on Euler that are not possible on other platforms. Very cool stuff!

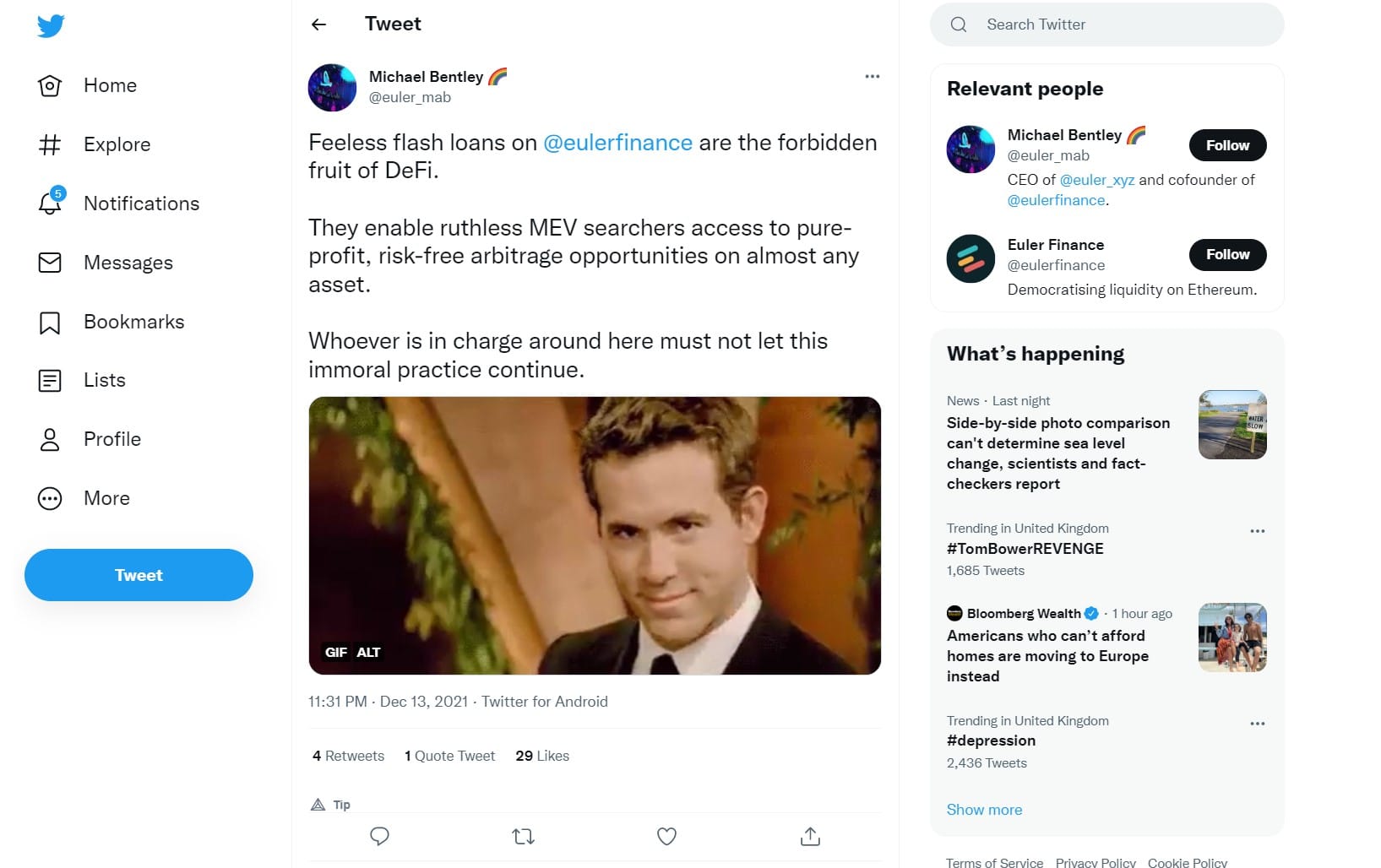

Being able to defer liquidity checks also leads to another great feature on Euler, and that is the Feeless Flash Loans.

Love the Ryan Reynolds Gif on Dr Bentley’s Tweet. Bonus Style Points for That. Image via twitter/euler

Love the Ryan Reynolds Gif on Dr Bentley’s Tweet. Bonus Style Points for That. Image via twitter/euler

Unlike Aave, Euler does not have the traditional concept of a flash loan. Instead, users can defer their liquidity check, make an uncollateralized borrow action, perform whatever operation they like, and then repay what was borrowed.

This action can be used to perform portfolio rebalancing, build up leveraged positions, take advantage of external arbitrage opportunities, and more.

Risk-Adjusted Borrowing Capacity

Similar to other lending protocols, Euler requires users to ensure that the value of their collateral remains higher than the value of their liabilities, except for during the period when liquidity checks are being deferred. Over-collateralisation is standard practice and controls how much can be borrowed in the first place.

To make this concept as simple as possible, it is essentially this:

I deposit $100 worth of X and can borrow $70 worth of Y. That way it doesn’t matter if I can’t pay back the $70, as the lender/platform keeps the $100. Nobody is left out of pocket but the borrower who failed to repay debts.

Compare this to what happened with the mess of what is happening with centralized lending platforms like Celsius and Voyager who are now bankrupt and what the folks at Three Arrows Capital did that caused their collapse:

They borrow $100 from you, then borrow $100 from me, then another $100 from Bob, without depositing any collateral, or perhaps less than they borrowed. Then when Three Arrows Capital cannot repay the $300 they borrowed, now you, me, and Bob are out of pocket, and poor Bob now doesn’t have the money he needs to feed his cats 😿

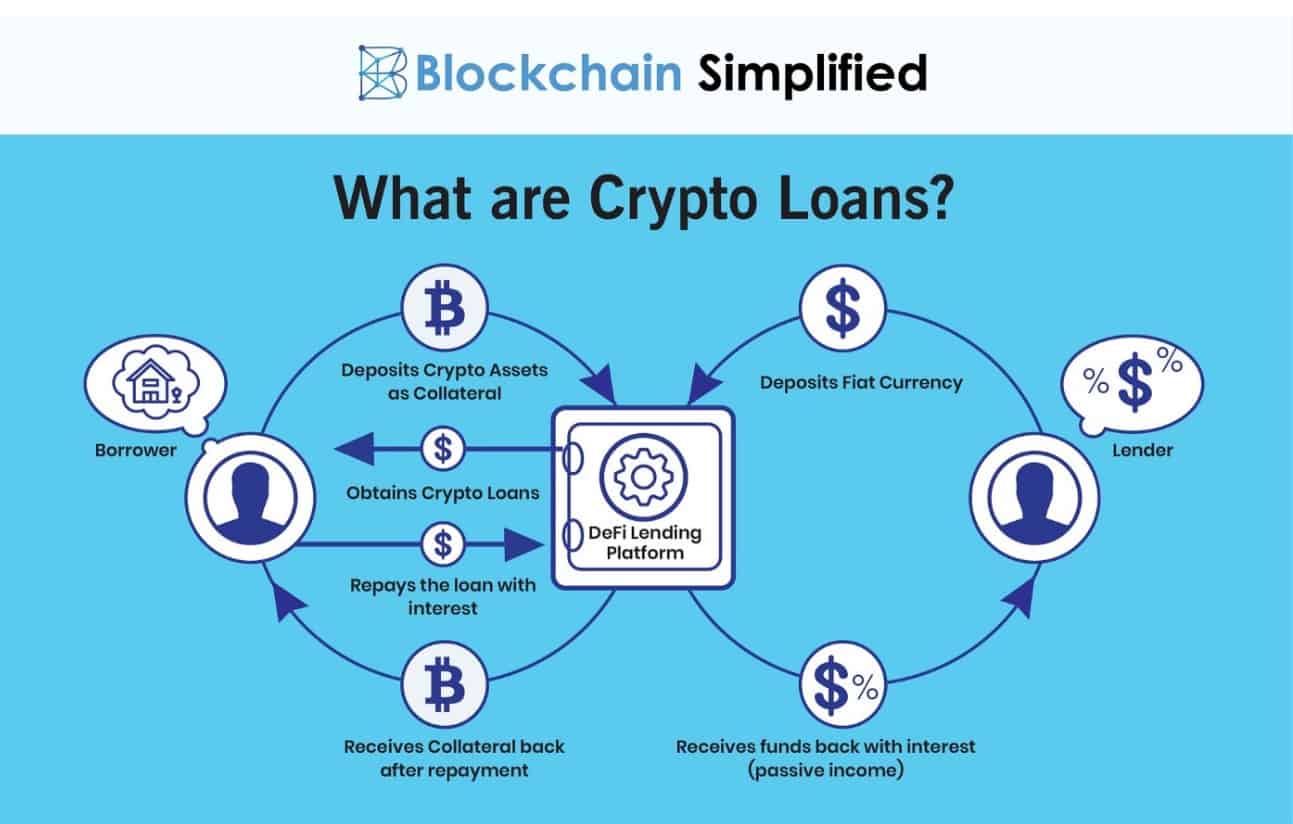

Blockchain Simplified have this fantastic and simple diagram showing how traditional crypto loans work:

Image via medium.com/blockchain_simplified

Image via medium.com/blockchain_simplified

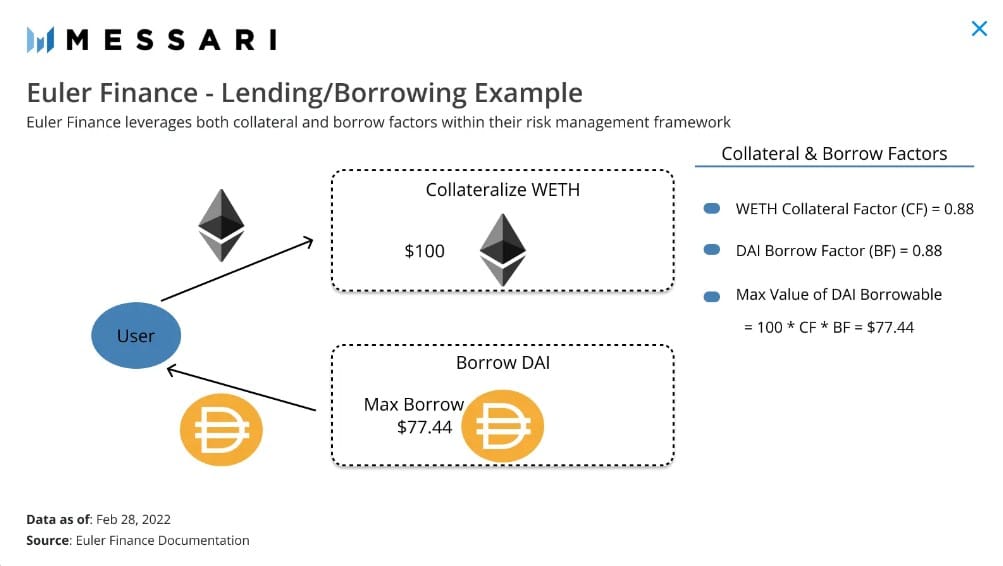

Euler achieves this differently from traditional DeFi lending platforms. They use a two-sided approach where they adjust up the market value of a borrower’s liabilities to arrive at a “risk-adjusted liability value.” This approach improves capital efficiency as it allows Euler to factor in the asset-specific risks of both downside and upside price movements, not just the downside risk as is done on platforms like Compound.

Image via Messari.io

Image via Messari.io

These risks are associated in asset-specific collateral factors similar to Compound, but also take into consideration of borrowing factors, which is unique to Euler. Ultimately, this approach means that the liquidation threshold of every borrower is tailored to the specific risk profiles associated with the assets they are borrowing and using as collateral.

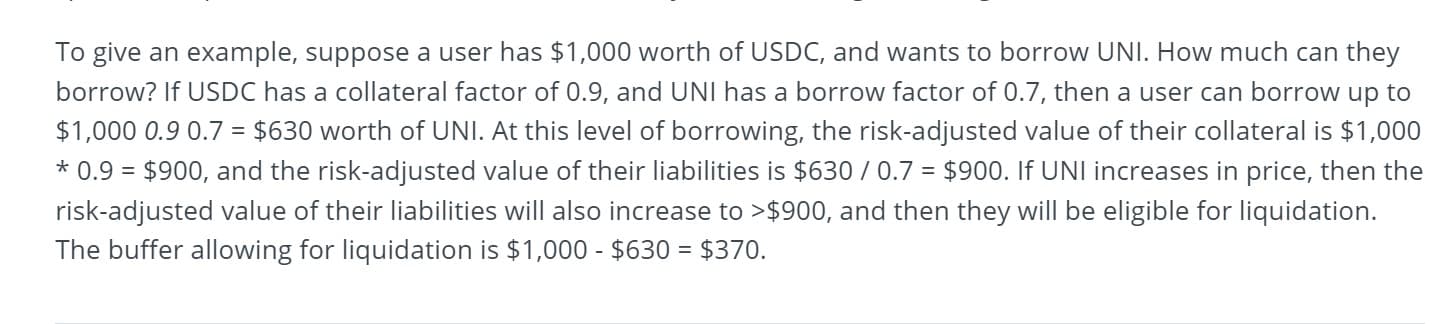

The Euler Whitepaper provides a great example of how this works, here’s a screenshot explaining it:

Image via Euler Whitepaper

Image via Euler Whitepaper

I think this is a very clever way of doing things as other DeFi platforms treat all borrowers the same regardless of the asset being borrowed, while Euler uses a method that is specific to each individual.

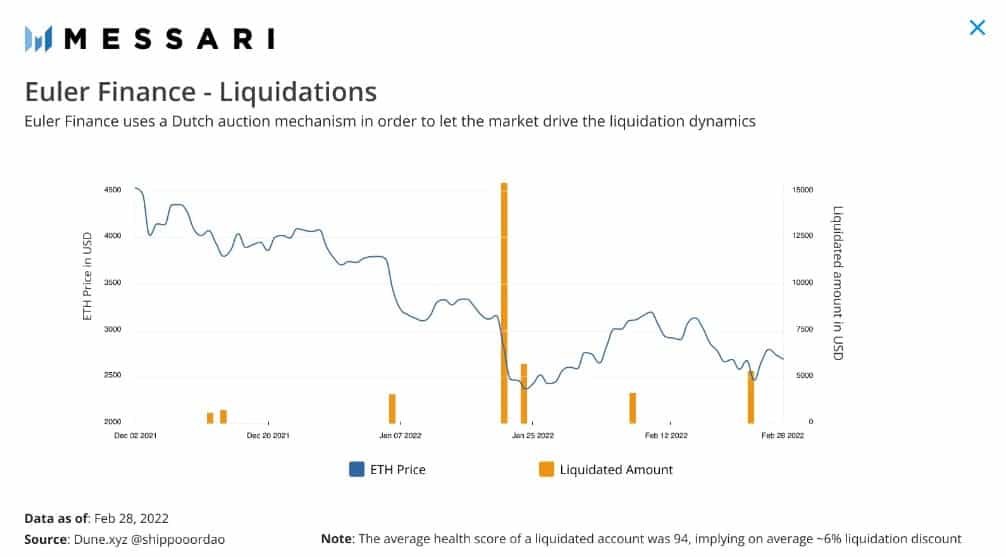

MEV-Resistant Liquidations

On most lending platforms, liquidations are incentivised by offering up a borrower’s collateral to liquidators at a fixed percentage discount (typically between 5-10%). The issue with this is that would-be liquidators often have no choice but engage in priority gas auctions (PGAs) for profitable liquidations, exposing the liquidation bonus as miner extractable value (MEV). Another issue with this method is that a fixed discount can be punitive for large liquidations, discouraging large borrowers, while being insufficient to cover costs and incentivising smaller liquidations.

How many “no-buenos” can I fit in one article? Euler is smashing it! Prior to research for this article, I had no idea there were so many shortfalls in traditional DeFi lending protocols that needed addressing.

Image via Messari.io

Image via Messari.io

To overcome this liquidation issue, rather than a fixed discount percentage, Euler allows the discount to rise as a function of how “in the negative” a position is. This turns the immediate liquidation trigger used traditionally into more of a Dutch Auction liquidation method. As the discount slowly increases, each liquidator must decide whether or not to bid for a liquidation at the current discount on offer.

As an example of how this may look, liquidator A might be profitable at 4%, but liquidator B might run operations more efficiently and be able to jump in sooner and liquidate at 3.5%. This Dutch Auction method is aided by the TWAP oracles that will be covered later on. This is beneficial as there is no one singular price point in which every liquidator becomes profitable at the same time.

Instead, the price can fluctuate over time leading to a continuum of opportunities to liquidate, which helps to limit the priority gas auctions and should help to drive the discount price towards the marginal operating cost of liquidating a borrower.

Though, this method alone does not prevent MEV as miners and front-runners can still steal a liquidator’s transaction. To limit this, Euler allows liquidity providers to make themselves eligible for a “discount booster”, which allows them to become profitable in the Dutch Auction before miners and front-runners who do not have the discount booster.

Soft Liquidations

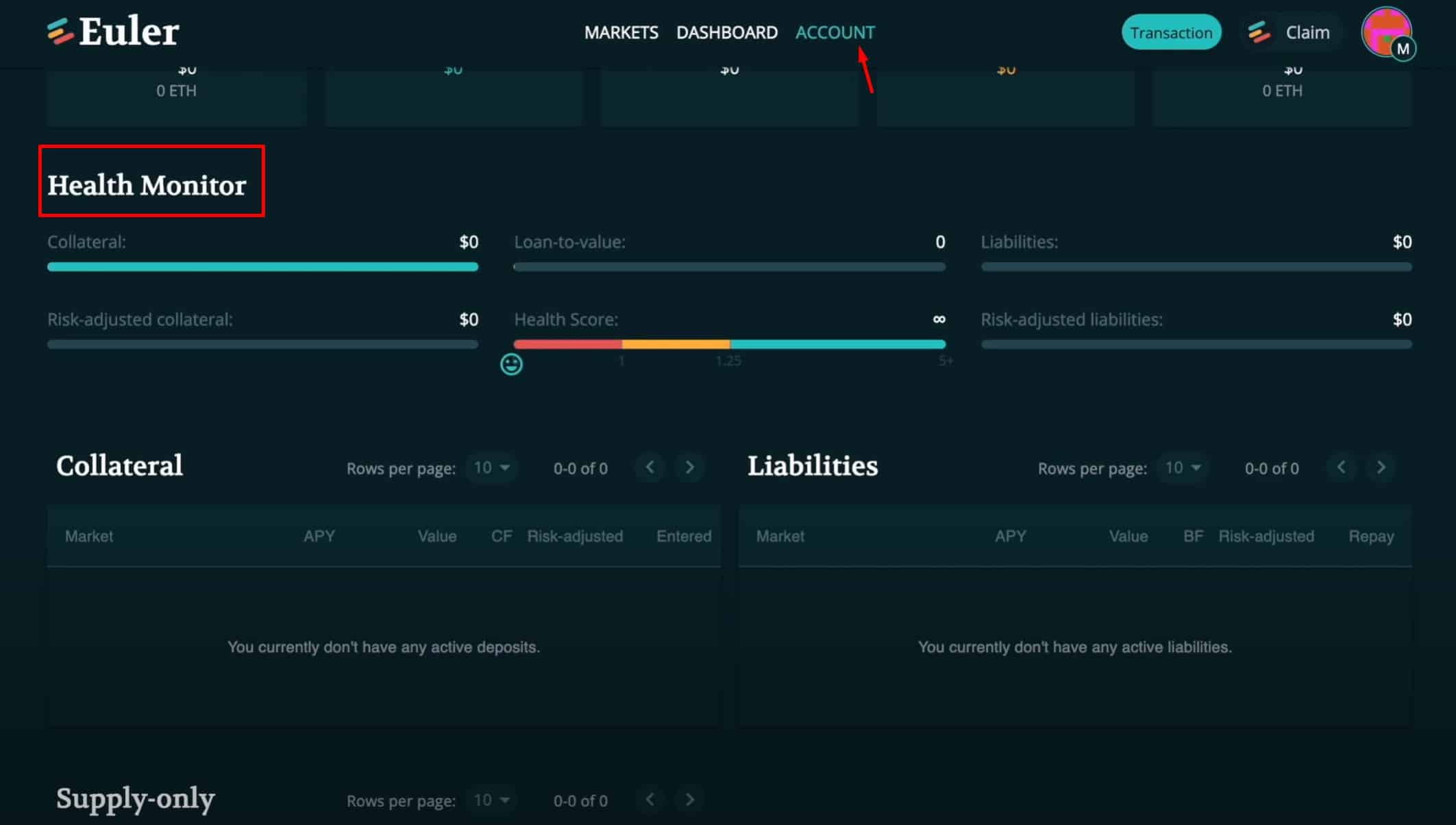

Soft liquidations are a very nice addition as it allows borrowers to have a fraction of their position liquidated if that means it can bring the loan-to-value ratio back into a healthy position, avoiding wiping out the entire loan.

Liquidations are Never Fun. Image via Shutterstock

Liquidations are Never Fun. Image via Shutterstock

This allows for liquidators to pay off a portion of a borrower’s debt without triggering a liquidation of the entire position. Euler uses a dynamic “close factor”, allowing liquidators to pay amounts to bring violators back to health, this helps enhance the stability and volatility of the assets held on the platforms and provides a better experience for the borrower as they experience less risk of complete liquidations.

When borrowing funds on any protocol, it is important to keep an eye on the health of the loan-to-value ratio on your loan:

Be sure to frequently check in on the “health monitor” of your loan which can be found in the “accounts” tab.

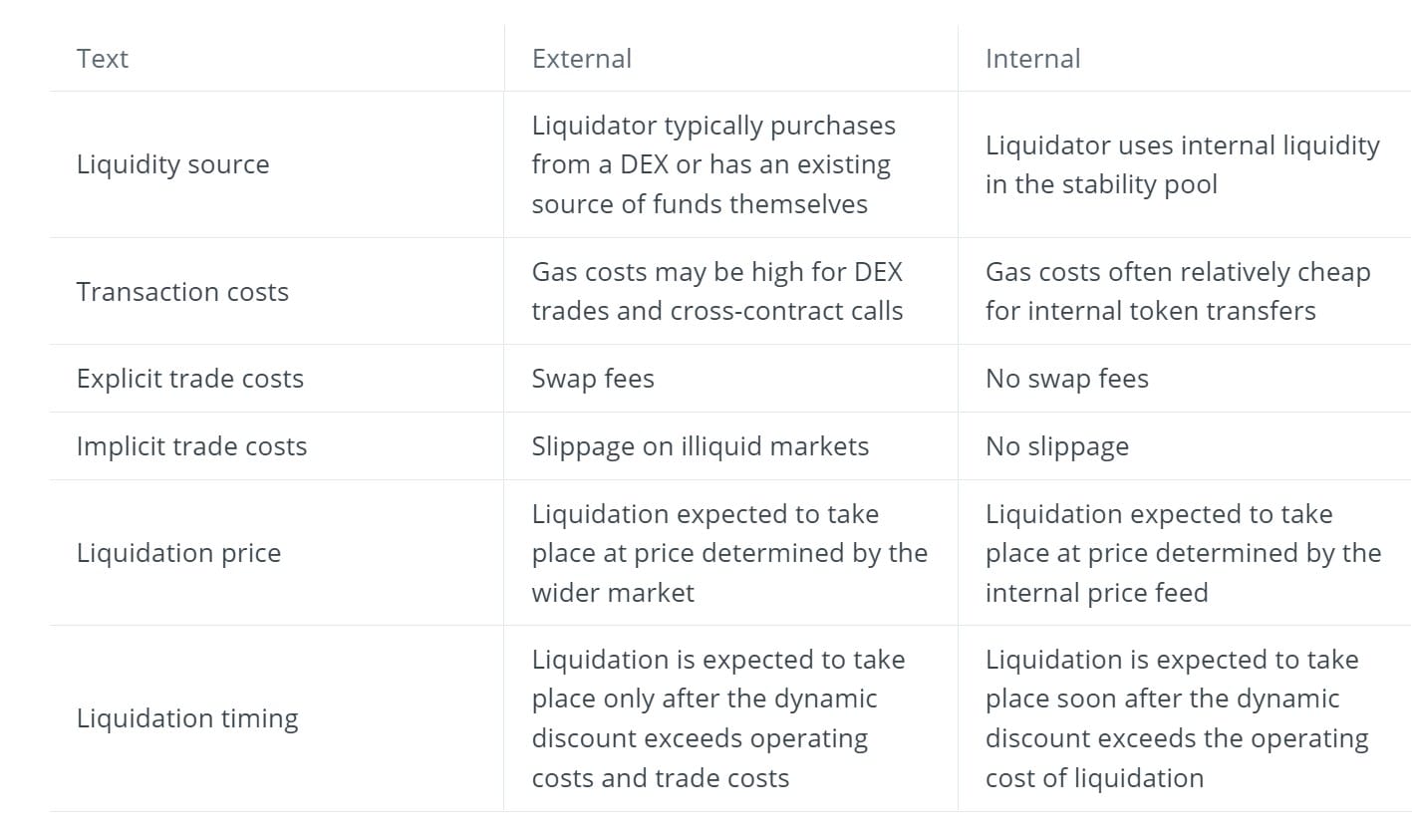

Stability Pools

Euler enables lenders to support liquidations by providing liquidity to a stability pool associated with each lending market. Liquidity providers in a stability pool deposit eTokens and earn interest while they wait for liquidations to be processed.

This is in contrast to the traditional liquidation methods on other platforms that rely on third-party exchanges to repay loans and third-party price feeds that may not align with the data feed of the lending protocol. This can cause issues such as things like slippage, swap fees, extreme volatility, and not using price-smoothing algorithms which may cause server mismatches in price.

Here is a comparison table showing the advantages of using an internal stability pool for liquidations vs external source of liquidity:

Image via Euler Whitepaper

Image via Euler Whitepaper

Euler’s approach can be thought of as an extended multi-collateral form of the stability pool idea that was pioneered by Liquidity Protocol. The main advantage of using a stability pool is that liquidations can be processed immediately using an internal source of liquidity at the point at which a borrower is deemed by the protocol to be in violation, without a liquidator needing to source the assets themselves from a third-party exchange.

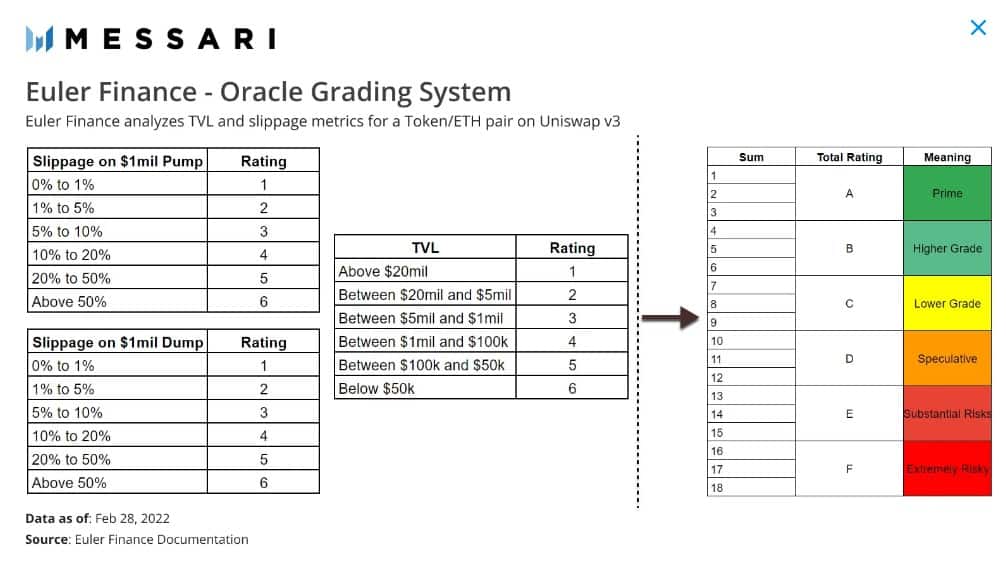

Decentralized Price Oracles

The price oracles used by Euler Finance are also a new innovation in the world of DeFi lending platforms. Platforms like Compound, Maker, and Aave use various systems to get prices from off-chain sources and put them on-chain so that they can be accessed by the relevant smart contracts.

Euler considers this an inefficient method and is unsuitable for them as it requires centralised intervention whenever a new lending market needs to be created. Euler relies on Uniswap v3’s decentralized time-weighted average price (TWAP) oracles to access the solvency of users in real-time. The reference asset used to normalize prices on Euler is Wrapped Ether (WETH) as it is the most common base pair on Uniswap.

Here is a look at Euler’s Oracle grading system:

Image via Messari.io

Image via Messari.io

This methodology is evolving and will eventually be replaced by a more comprehensive solution. Euler has already developed an open-source oracle tool that will simulate how costly it is to manipulate a given token pair on Uniswap.

Euler Finance: Interest Rates

Traditional platforms use static linear interest rate models to guide the cost of borrowing on their platforms. Simply speaking, as demand for borrowing from the pool increases or supply decreases, interest rates go up, and when supply increases or demand decreases, interest rates go lower. Simple supply and demand economics 101.

This model works fine if they are appropriately parameterised ahead of time but can cause issues if they are parametrised incorrectly. To avoid this, instead of static linear interest rates, Euler uses reactive interest rates.

To avoid the problem of having to choose the right parameters for every lending market, Euler uses control theory to help autonomously guide the cost of borrowing towards a level that maximises capital efficiency on the protocol. In fact, Euler was the first DeFi protocol to innovate in this way and has received praise for the innovation within the DeFi community.

Here is a great infographic showing how the interest rate calculation method on Euler differs from Aave and Compound:

Aave/Compound:

Euler Finance:

Graphics via Euler

Graphics via Euler

Euler uses a PID controller to amplify the rate of change in interest rates when utilization is above a target level of utilization. This allows for reactive interest rates that adapt to market conditions for the underlying asset in real-time without the need for ongoing governance intervention.

Euler Finance: Gas Optimization

You young whipper-snappers who are just getting into DeFi today with your fancy layer two Ethereum scaling solutions may never know the pain of Ethereum gas fees. Back in my day, it wasn’t unheard of to spend hundreds of dollars for a single Ethereum transaction.

Okay grandpa, settle down.

To avoid horrendous gas fees and "back in my day" stories, Euler relies on smart contracts that minimize the amount of storage used and implements a module system to reduce the amount of cross-contract calls needed to be performed and has had a number of other gas usage optimizations applied to the protocol.

This makes Euler more gas-fee friendly than many other lending protocols as those smart-contract transactions can really punch a hole in the old Ethereum bank account.

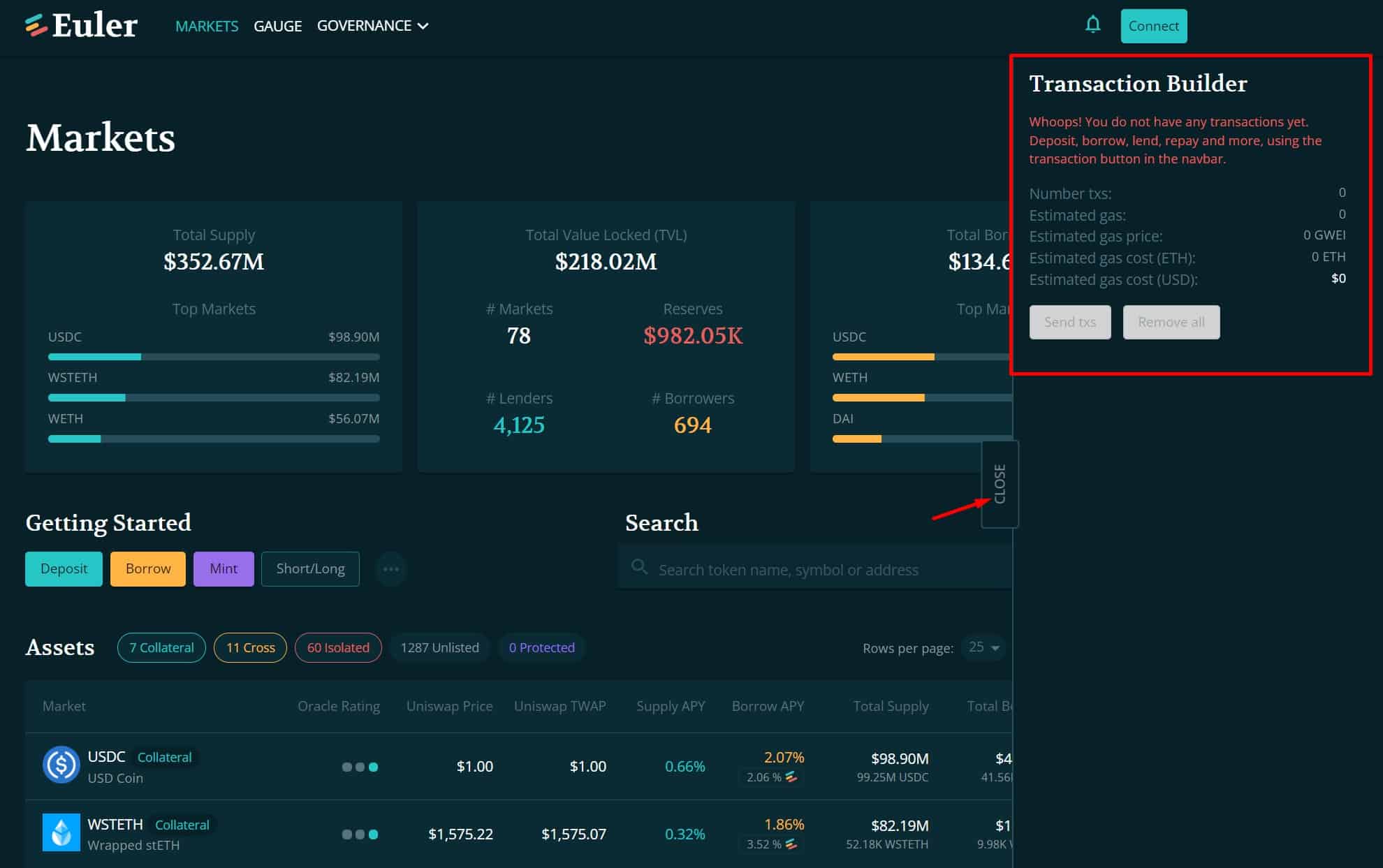

Through a feature known as Transaction Builder, users can batch multiple transactions and reduce their gas costs, while advanced users can use this feature in conjunction with the “defer liquidity checks” option to perform many functions for low-fee transactions.

Here is a look at the Transaction Builder interface:

Image via Euler

Image via Euler

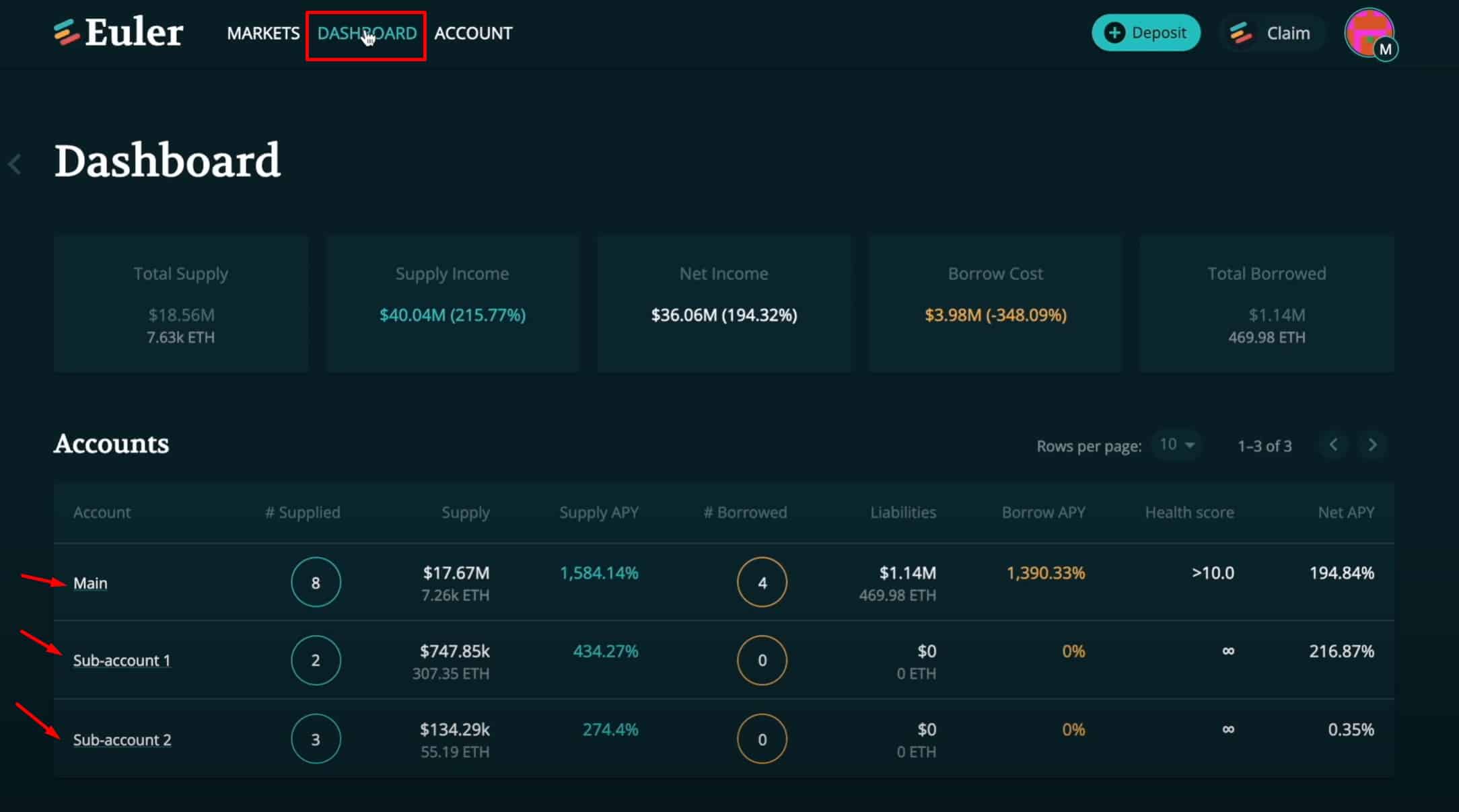

Another innovative addition is the use of Sub-accounts. If users of Euler had to send collateral to new Ethereum addresses for each new isolation-tier loan, it would cost a fortune in gas fees. To avoid this, Euler enables every Ethereum account using the protocol to access up to 256 sub-accounts which can be used to cost-effectively manage multiple positions at the same time. The user only needs to approve Euler’s access to a token once and can then deposit into any sub-account.

Pro Tip: If the image above made you think I have millions of dollars on the platform, I wish I was that ballin! If you switch your MetaMask wallet network from the Ethereum network to the Ropsten testnet, you can explore the platform using millions of dollars worth of demo funds to get a feel for how it works.

An additional benefit to sub-accounts is that no approvals are required to transfer assets and liabilities between them, allowing users to isolate and segregate their collateral and debts.

Euler Finance: Design and Usability

DeFi platforms aren’t always known for their beginner-friendliness and are often utilized by more advanced crypto users. Euler is no exception here as the concepts are still considered a bit advanced, though I do have to say that one thing I found they did very well was create a UI/UX that is easier to navigate and manage than most other DeFi platforms, so I have to tip my hat to that.

Here’s a look at a few of the different interfaces:

The platform provides all the functionality you would expect from a DeFi lending platform. The navigation is a breeze, and all the graphics, gauges, and menus lead to Euler being one of the better platforms I have used in terms of design, functionality, useability, and just general navigation and understanding of what is actually going on within the protocol.

For anyone who has ever used a DeFi platform, using Euler Finance will be straightforward as their design team did a fantastic job. Once you connect your MetaMask, Fortmatic, Keystone, Ledger, Torus, Trezor or Coinbase wallet, you’ll be off and flying in no time.

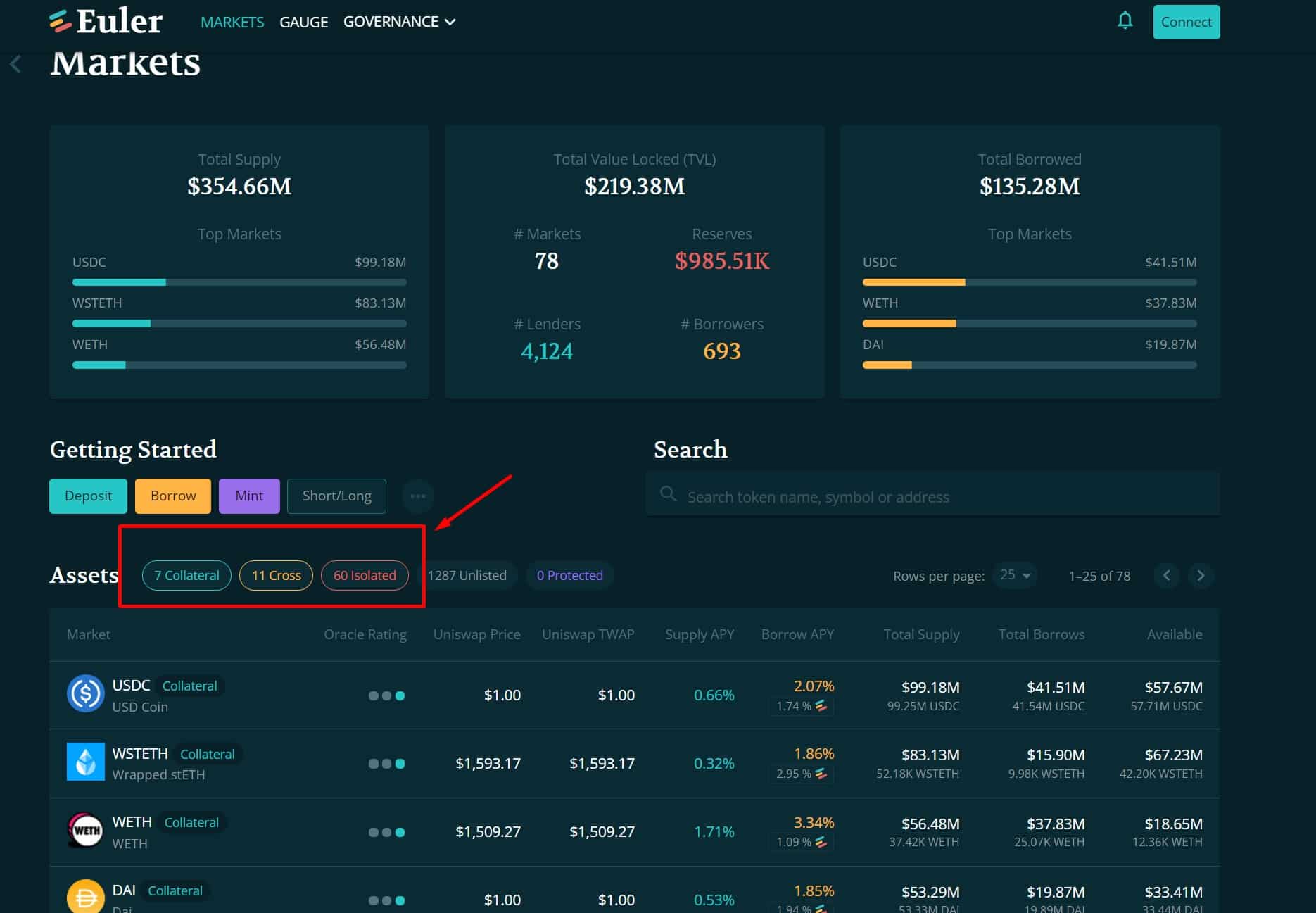

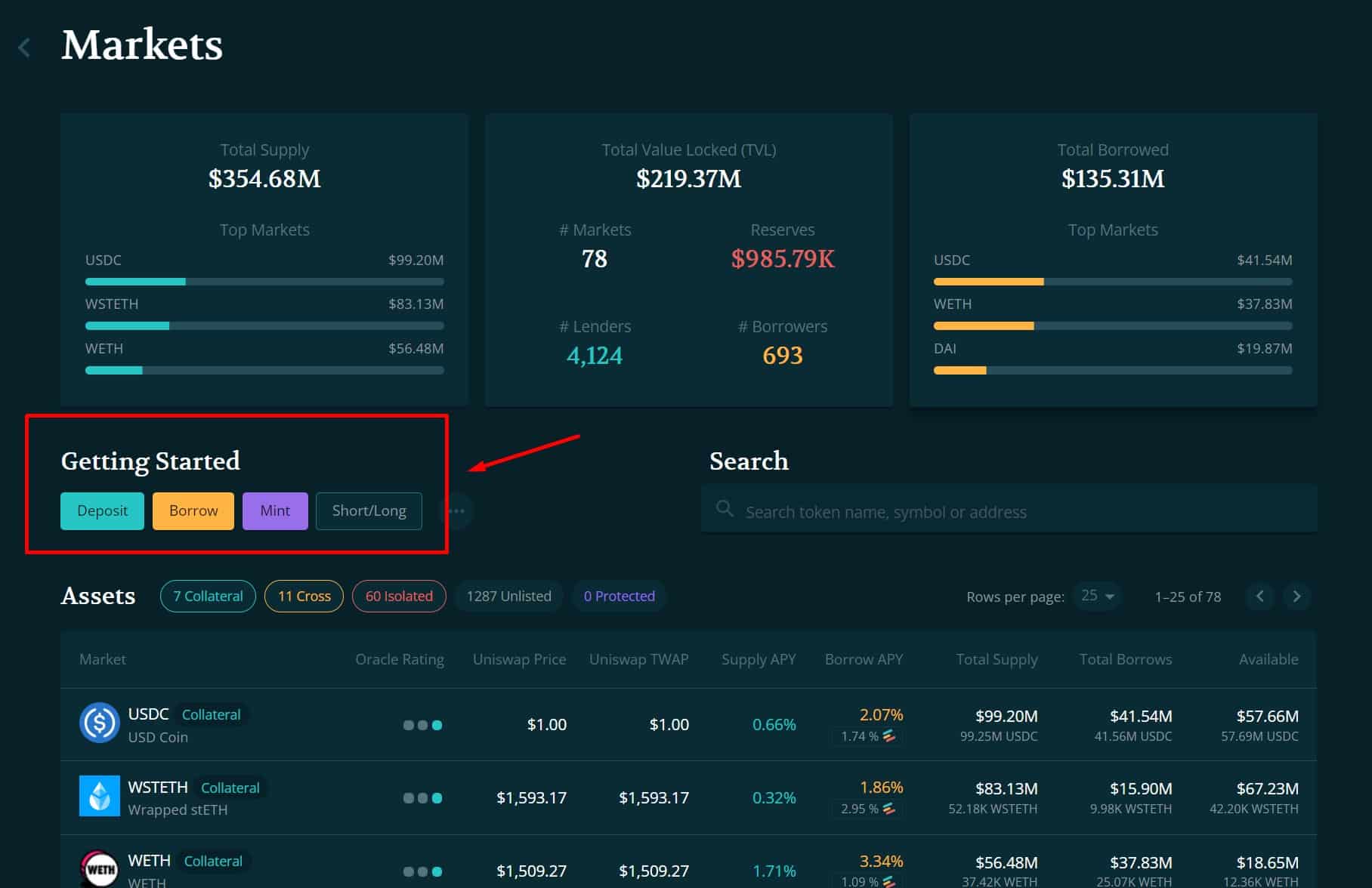

There are four main sections: Markets, Dashboard, Governance and Account which are worth describing briefly.

Markets- This is the area where you can see the markets, borrow, supply, TVL amounts and Oracle ratings.

Gauge/Dashboard- Shows all the accounts, sub-accounts and monetary information.

Accounts- Shows all the information about the user’s account, namely how much collateral you have, any active loans, the health score of the account, what is being lent etc.

Governance- This is where users can access the delegates section and the forum where proposals and governance issues are being discussed.

Euler Finance: Governance

The governance utilized by Euler is very similar to the governance model pioneered by Compound Finance years ago. I guess they figured,” why reinvent the wheel?”

The protocol will be managed by holders of the Euler Governance Token (EUL). Tokens will represent voting powers of the protocol software, and holders with enough tokens will be able to make proposals for changes to the protocol. Token holders will be able to vote on topics such as:

- The tier of an asset

- Collateral and borrow factors

- Price oracle parameters

- Reactive interest rate model parameters

- Reserve factors

- Governance mechanisms themselves

Euler Finance: Reserves

How a protocol manages its reserves is an important consideration for anyone wanting to become a lender on the platform. Mismanagement of reserves is how issues like bank runs happen and why platforms like Celsius and Voyager had to halt customer withdrawals and file for bankruptcy.

The way most lending protocols work is that they will take a portion of the interest paid by borrowers, and rather than hand it to lenders, they will keep it within the protocol.

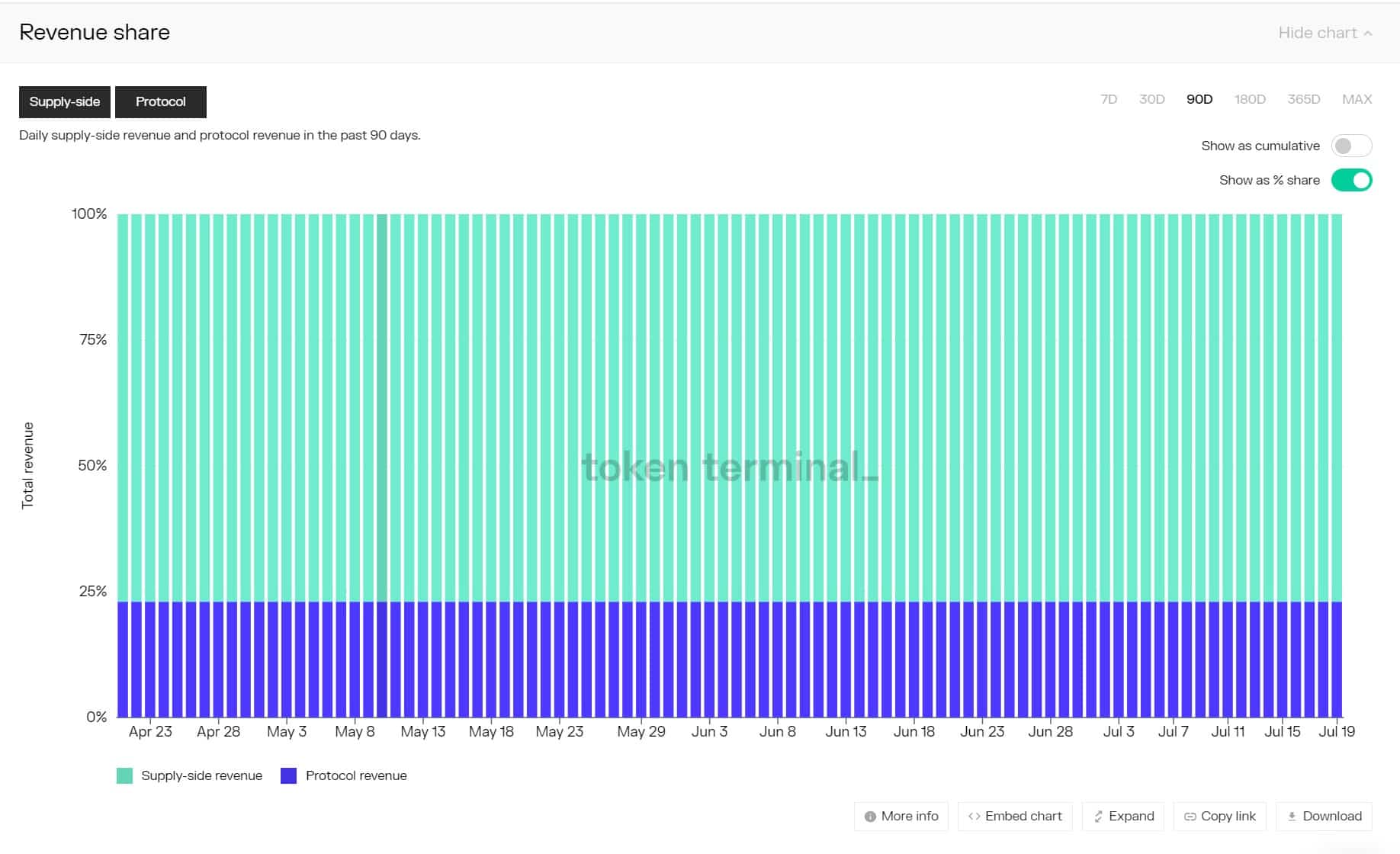

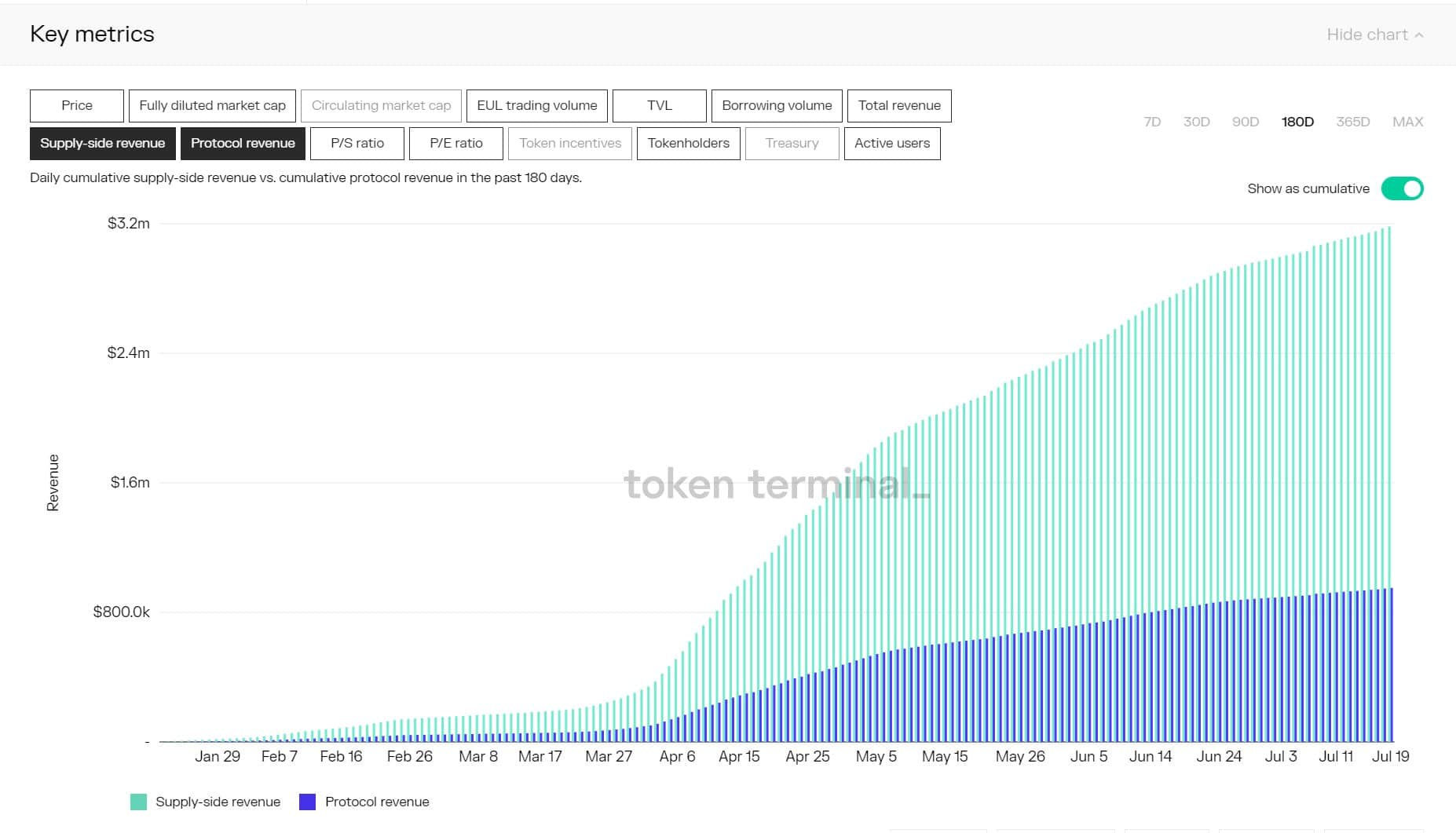

Let’s take a look at supply-side revenue and protocol revenue for Euler Finance over the past 90 days:

Image via Token Terminal

Image via Token Terminal

We can see that Euler sets aside a healthy portion of platform revenue. Reserves are important as they act as a backstop to lenders. There are scenarios in which borrowers will be unable to pay back their positions which leads to something called “bad debt”. If that bad debt spreads too widely and is not contained, then other lenders get nervous about being left holding the bag of bad debt which may lead to them withdrawing their funds, leading to a spiral, aka bank run.

Euler has positioned itself in a way that the reserves will grow faster than bad debt accumulates and has done so since the infancy of the protocol. This allows for the accommodation and confidence of more lenders on the protocol. We can see how this has played out on Euler over time:

Image via Token Terminal

Image via Token Terminal

Euler does a few things differently with regards to reserves than other lending protocols according to this interview with CEO and Co-founder Dr Michael Bentley.

To start, reserves on Euler are perpetually reinvested back into the protocol and earn compounding interest so they grow exponentially over time. Euler has also set a higher reserve factor in a way that leads to roughly a quarter of interest paid going to the protocol and not the lenders.

The trade-off here is lower returns for lenders, but safer and more sustainable interest payments that will hopefully lead to a long and prosperous lending platform and avoid the pitfalls that unsustainable lending platforms have experienced in the past by offering 20%+ returns then going bust. Remember guys and gals, if the returns seem too good to be true, they probably are and the higher the returns, the higher the risk. Euler aims to find that Goldilocks zone or “sweet spot” balancing risk and reward.

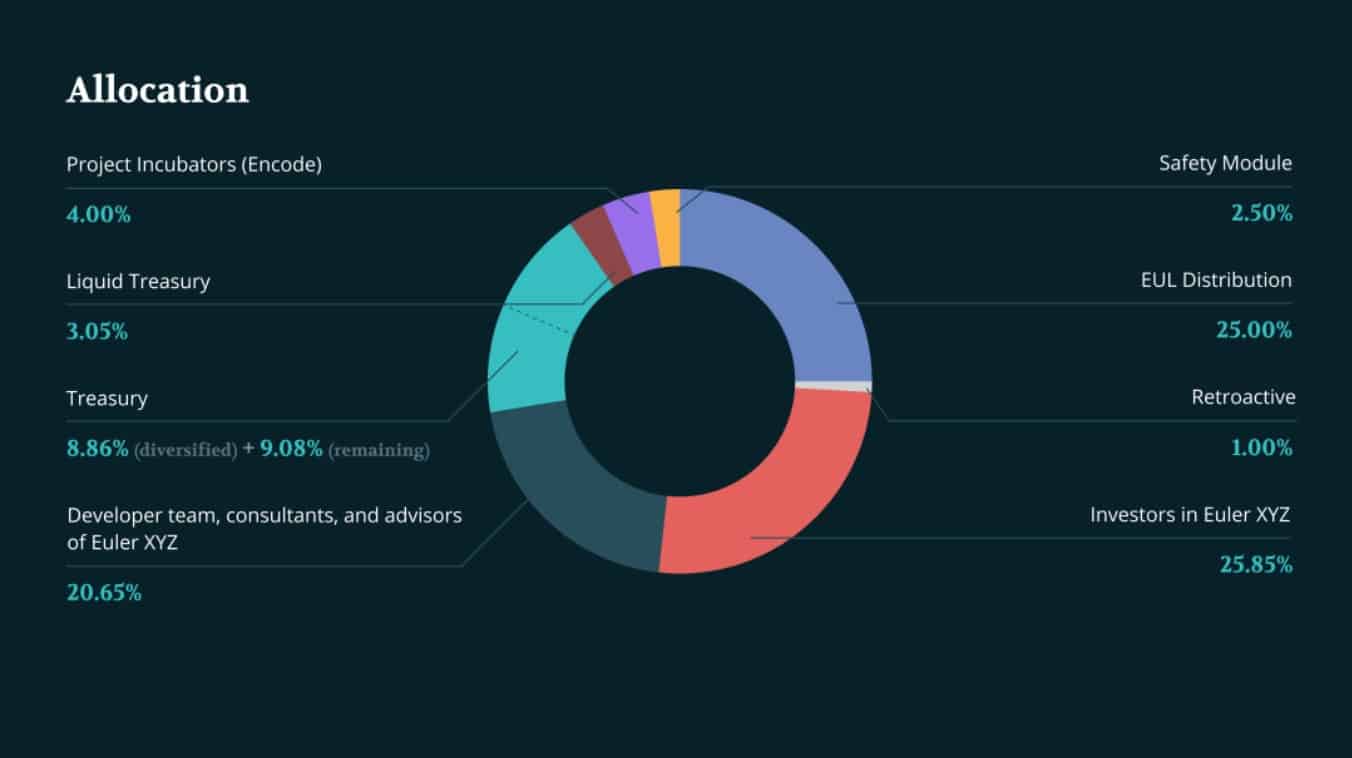

Euler Finance (EUL) Tokenomics

Euler (EUL) is the native token on the Euler Finance protocol. It is an ERC-20 token that acts as a governance token. The total supply of the token is 27,182,818 (a homage to Euler’s number).

As for the token allocation, here is what we are looking at:

Image via Euler Finance Whitepaper

Image via Euler Finance Whitepaper

The initial allocations may be subject to change as the ecosystem evolves. The total supply is fixed for the first 4 years, after which EUL token holders may enact a governance proposal to inflate the supply by a max of 2.718% per year.

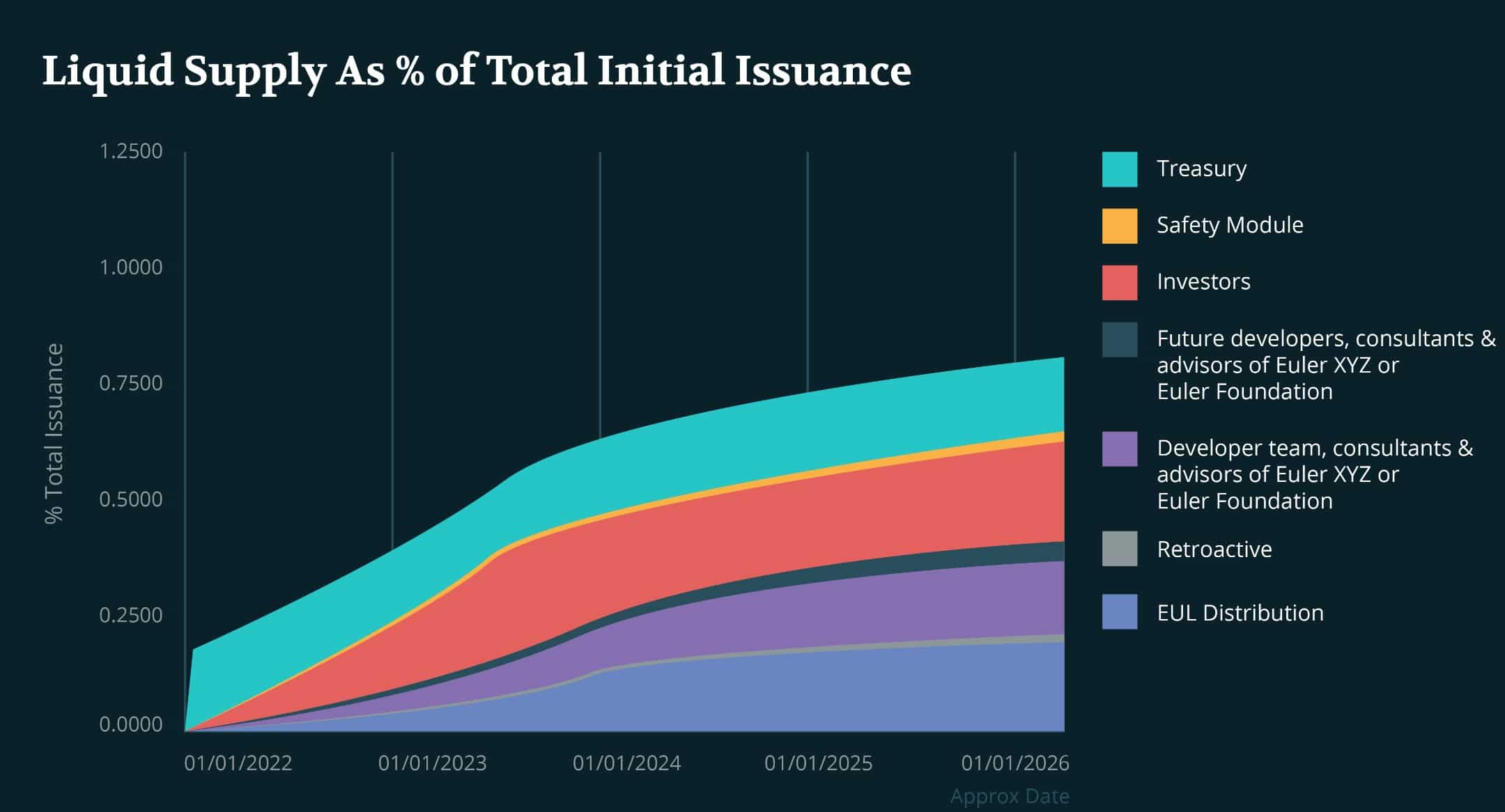

Here is a look at the supply schedule leading into 2026

Image via Euler Finance Whitepaper

Image via Euler Finance Whitepaper

Normally I dive into the token performance of a project but as the token has only been out since June 28th 2022, there isn’t much to look at. The token released to the public at a price of $3.73 according to CMC, bounced around like a pinball for 3 weeks shooting up to $4.40 then down to $3.20 before resting at $3.40 where it resides at the time of writing.

Token holders are users of the platform who are interested in governance and investors who are long-term bullish on the innovation and success of the platform. The EUL token is currently available on exchanges such as Huobi, Gate.io, MEXC and Uniswap.

Euler Finance: Security

Euler Finance has an impressive catalogue of security partnerships with some of the top security firms in the industry:

Image via Euler

Image via Euler

The platform has undertaken security audits by firms such as Halborn and offers a $1 million dollar bug bounty programme. The team posted the satisfactory security audit results on their Github.

Still, in March 2023, Euler Finance was the victim of a roughly $200 million flash loan attack via a code exploit. However, in a stunning turn of events, the hacker agreed to return the money in its entirety, marking one of the largest recoveries of stolen assets in blockchain history.

Euler Finance isn’t the first DeFi hack victim of 2023 — dForce and Platypus were similarly targeted in February, but Euler's hack was by far the largest.

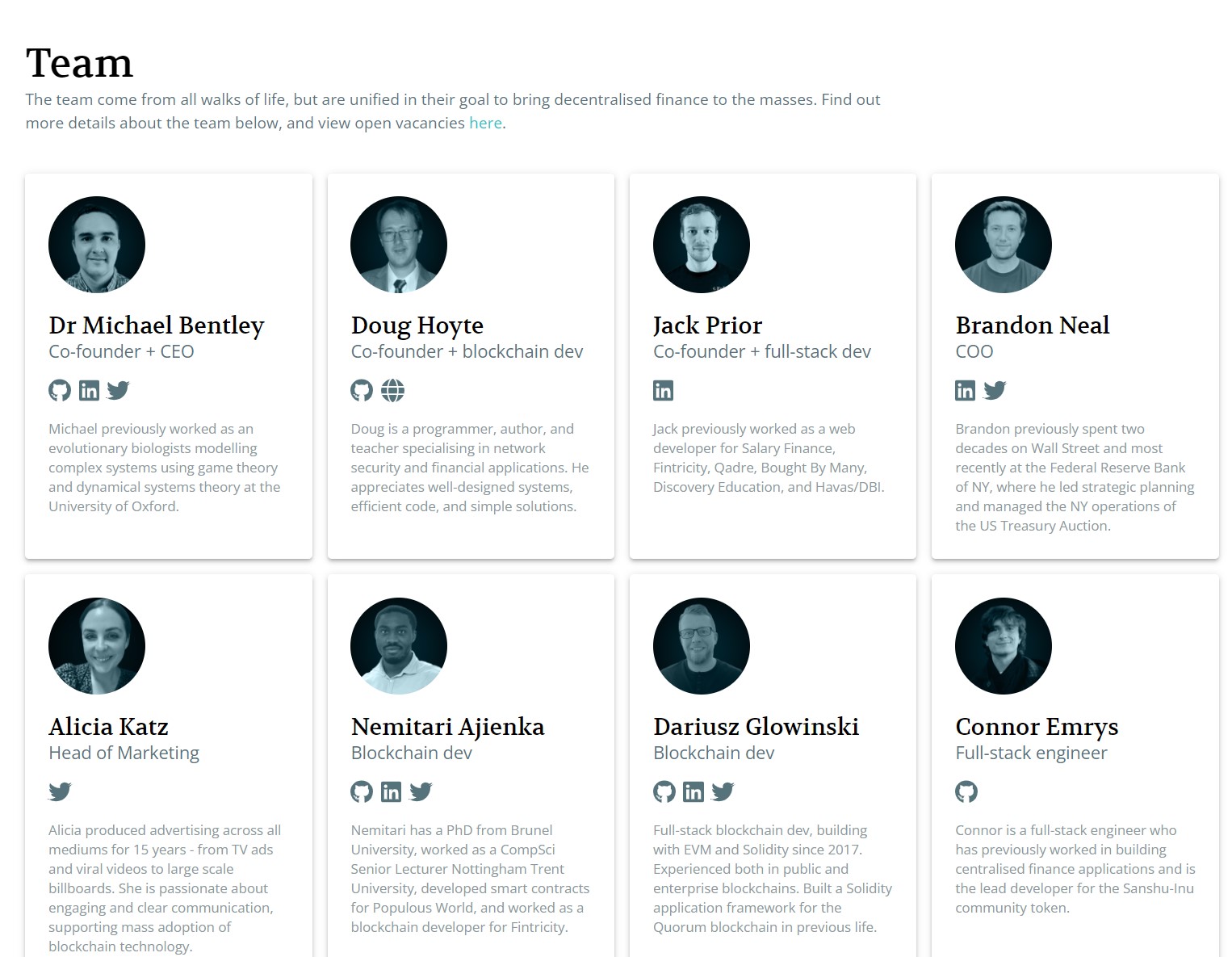

Euler Finance: Team and Investors

Euler is a team of software engineers and quantitative analysts that specialize in the research and development of web3 technology and financial applications. There is more to the team than just the Euler Finance platform.

The team is made up of members from various backgrounds that have extensive experience in both traditional and blockchain companies.

Dr Michael Bentley- Co-founder and CEO: In a previous life, Dr Bentley worked as an evolutionary biologist who used game theory and complex systems modelling to diagram evolutionary theories. He studied at the University of Oxford, worked as a Pricing Analyst for the Royal Bank of Scotland, and went on to become a Postdoctoral Research Associate at Oxford. An impressive and interesting background indeed.

Doug Hoyte- Co-founder and Blockchain Dev: Doug is a programmer, author and teacher who specializes in network security and financial applications.

Jack Prior- Co-founder and Full-Stack Developer: Jack worked as a web developer for Salary Finance, Fintricity, and Qadre, among others, and has over 11 years in the industry as a web developer. After studying web and multimedia management at the University of Sussex, he has held multiple developer roles for various companies before co-founding Euler.

Image via euler.xyz

Image via euler.xyz

Euler has an impressive team and more members than I can list here. Feel free to check out the Euler Team page if you want to learn more.

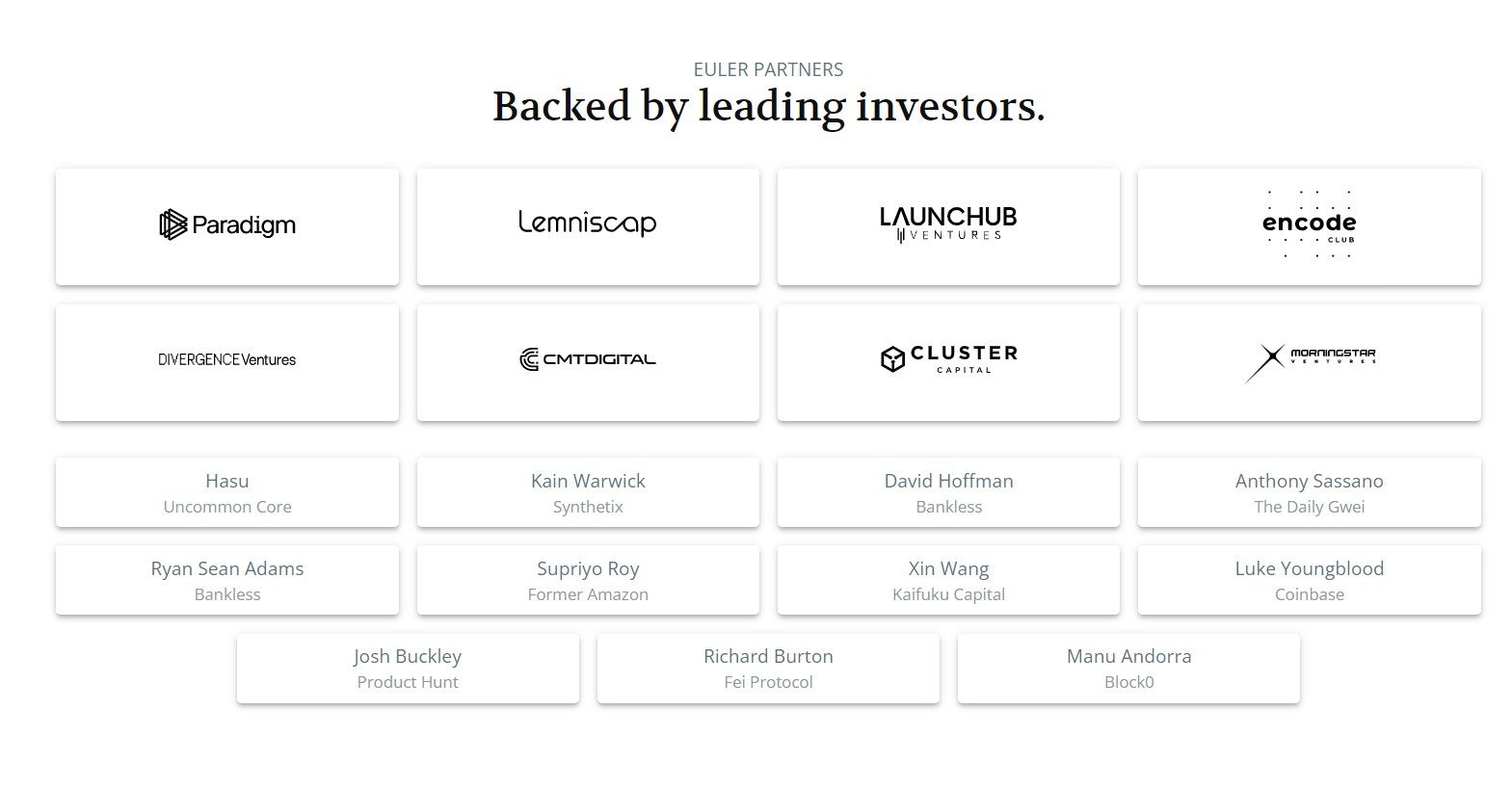

Euler is also backed by some industry-leading investors and VC firms as they have been attracting some folks with deep pockets. Here is a look at some of their investors:

Image via euler.xyz

Image via euler.xyz

Euler Finance: Concerns

I am going to be honest with you guys and admit something that not many people are willing to do. Crypto and DeFi is a multi-billion-dollar experiment and nobody knows what the state of decentralized finance will be in five years, or if it will be around at all.

In case events like the Terra collapse, the Celsius and Voyager bankruptcy, and the tens of thousands of failed crypto projects that no longer exist haven’t convinced you, nobody really has a clue in this industry of what will and won't work. It is a giant case of, “let’s throw some spaghetti at the wall and see what sticks.” As in, let’s try a bunch of different things and see what works.

If you don’t believe me, ask Mike Novogratz, CEO of Galaxy Digital who has put millions of dollars into his research teams and has top industry analysts and an entire firm analyzing and researching projects. Even with all that at his disposal, he was still so confident in Terra that he got himself a massive Terra tattoo before it collapsed and lost people billions in funds.

Image via twitter/novogratz

Image via twitter/novogratz

What I am getting at here, is that I have no idea if Euler Finance will prove to become a long-term and sustainable lending protocol. Maybe this is just me, and it may sound strange as I am a crypto investor, which is considered as the riskiest asset class, but I am quite risk-averse and I like trusting protocols, platforms, and tech that has been thoroughly battle-tested. It took me years of keeping an eye on Aave, half-expecting a collapse or rug pull before I was confident enough to use the protocol.

After testing out Euler Finance, verifying their security audits and scouring the platform with a fine-toothed comb, I could not find fault with the platform at all. It really does appear to be the next-generation lending protocol with many benefits over traditional lending platforms.

On paper and in theory, the revolutionary ideas and concepts sound brilliant, but my main concern is that it has not been battle-tested and withstood the test of time. Though in full transparency, this platform gives me a far higher degree of confidence than most newer DeFi platforms out there due to their focus on security, and what seems like incredibly clever innovations in the protocol mechanics.

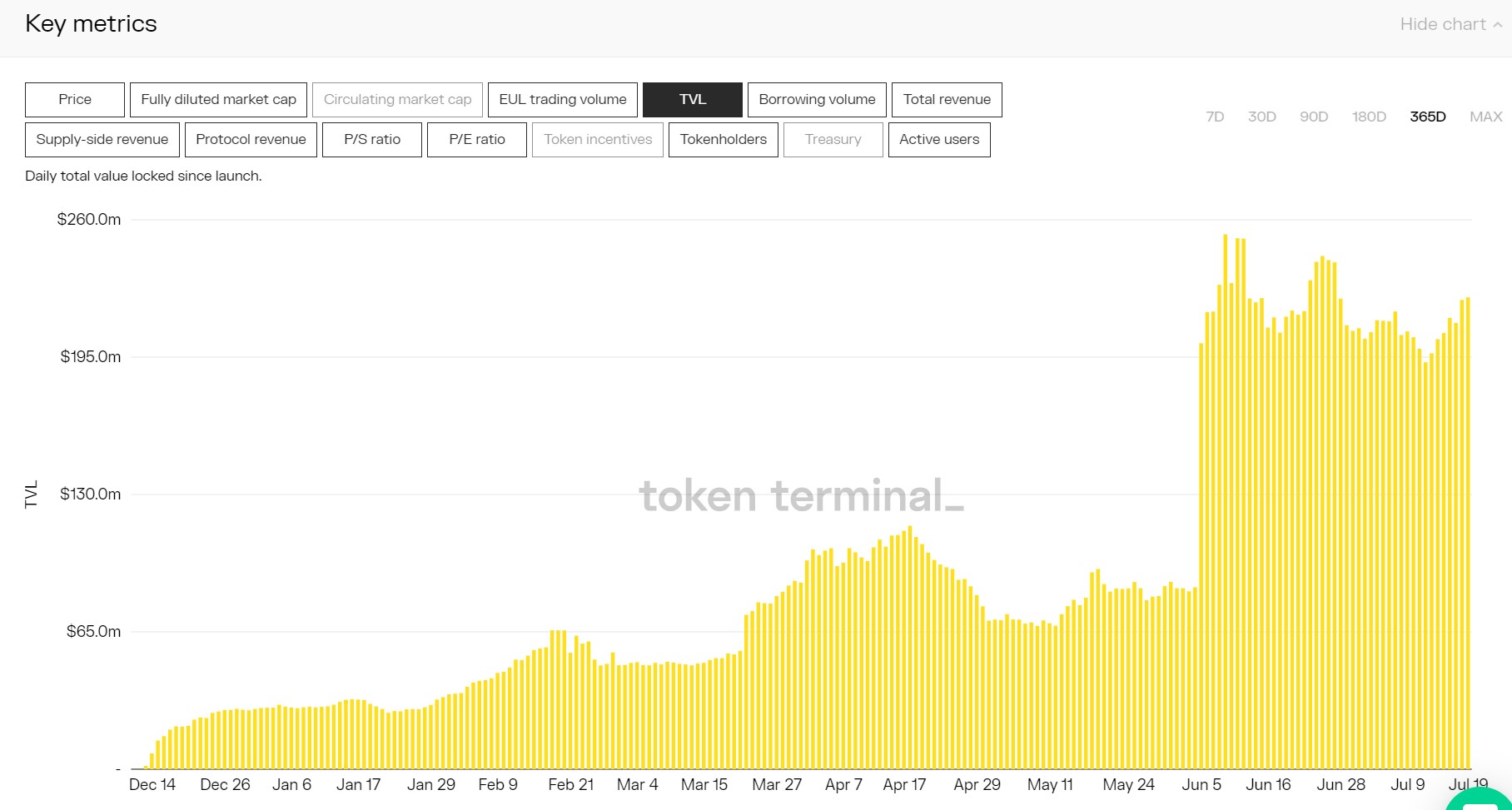

My only other concern comes in the form of low liquidity and total value locked as it is currently ranked 25th in TVL, making it not suitable for larger lenders and borrowers. Though with that being said, we are seeing a very healthy increase in value locked which is a good sign that the platform is quickly gaining traction:

Image via Token Terminal

Image via Token Terminal

Keep an eye on the platform’s liquidity before diving into the platform as a platform with no money locked into the protocol can't function, but of course, it is still a very new project and is picking up healthy traction and adoption. I expect it will climb the ranks as more users adopt the platform.

Euler Finance: Closing Thoughts

I am a big fan of innovation in the space. It is great to see platforms like Euler Finance build on the experience and ideas of previous platforms and advance the concepts, contributing to the evolution of the decentralized finance industry. If banks are like the horse and carriage, DeFi protocols like Compound, Maker, and Aave are the automobile, then platforms like Euler Finance aim to become the flying car, hoverboards, jetpacks, or those tube things people use to whiz around in the show Futurama.

The DeFi industry is awash with copycat protocols and countless unimaginative clone platforms that are just trying to capitalize on a growing trend. Euler is certainly an exception to that norm as it utilizes features never before seen in DeFi such as permissionless lending markets, reactive interest rates, protected collateral, MEV-resistant liquidations, and multi-collateral stability pools.

For the brave and the bold who are not afraid to jump into new things, Euler Finance offers many benefits over traditional lending protocols which is one of the reasons the platform has quickly enjoyed adoption and TVL increase as new users have flocked to the platform.

For me personally, as much as I appreciate the innovation, am thoroughly impressed, and love seeing the industry advance and evolve, like a hot tub, I am going to dip my toes in and use the platform with limited funds over the next while as I like what it has to offer, but only time will tell if their new experimental methods of building a lending platform will prove to be superior and sustainable.