Whether you like it or not, crypto hasn’t yet taken over the world. In most places, fiat currency is used for the majority of financial transactions. This means that not all of your funds can go into crypto since you’ll need some cash to pay for your expenses. Yes, you could sell your crypto whenever you need some fiat; however, let’s face it, that isn’t smart.

First of all, selling crypto includes transaction costs which means it will be extremely expensive to bounce between crypto and fiat. Second of all, you miss out on potential capital gains from not holding funds in cryptocurrency. If there only was a way to solve this... That’s where MELD comes in.

MELD Protocol aims to solve these problems by providing both crypto and fiat borrowing/lending as the go-to banking protocol. It’s true that multiple protocols are looking to do the same, and to be fair, I thought this too was going to be another similar one in a pile of protocols. However, I was wrong.

MELD has some interesting qualities that vastly differentiate it from its competitors. One major difference is that MELD is built on top of Cardano. According to MELD, this allows far cheaper transactions than for Ethereum-based competitors. Cardano is also viewed as a far more environmentally friendly Ethereum alternative that could help gather clients, at least institutional clients and investors.

What Is MELD?

In one sentence, MELD is a decentralized non-custodial banking protocol. MELD was started in April of 2021, and its development is done by MELD Labs, based in Singapore. The governance is done by MELD Foundation based in Switzerland. They oversee, for example, all of MELD’s fiat bank accounts. Partners include both native crypto projects like Polygon and traditional companies like the Agri-Fintech company Tingo. Lastly, MELD also has a handful of respected investors, including Silicon Valley Blockchain Society and Brotherhood.

A look at MELDImage via MELD

A look at MELDImage via MELD Being in an extremely early stage, they don't have many of their planned features up and running just yet, but according to their roadmap, which I'll be covering later, many things are coming during this year. Once fully operational, MELD will be found on IOS, Android, web browser and as a chrome extension

Currently, you can only access MELD's DApp in the browser; the mobile applications should be available sometime in Q2 or Q3. MELD is also not yet fully decentralized, but they have a roadmap for that too. Also, although decentralized, you still need to complete KYC/AML to get access to most of the features. This is naturally understandable since you'll be receiving funds to your own bank account etc.

According to the MELD whitepaper, they want to provide individuals with control of their own finances. Basically, anyone is the key customer for MELD, but they multiple times highlight the need for financial services for the unbanked. The whitepaper talks about $15 trillion being left out from the traditional financial system. However, while the thought is excellent and they're working on making it a reality with partnerships like the one with Tingo, I believe that crypto companies and individuals will at least, in the beginning, be key customers.

I'll be explaining how MELD works more in-depth in the next section, but the critical detail is that when you take a loan, you can choose to receive fiat money (USD, EUR) to your bank account. This means that companies and individuals can utilize their cryptocurrency holdings to pay for everyday use cases. Holding cash is a liability for companies but is still necessary to cover operational expenditures.

However, suppose a company now wanted to reduce their cash positions. In that case, they could buy Bitcoin and use it as collateral to get a line of credit or a loan. This way, they could still benefit from capital gains while minimizing their cash on hand. One good example is crypto mining companies who have increasingly been reluctant to sell their Bitcoin. However, they've had to cover their expenses. With MELD, they could opt not to sell but instead use that as collateral and receive fiat while still being exposed to the upside of Bitcoin.

Currently there aren't many things to use for, but all the features are coming. Image via MELD app

The last thing I want to highlight from MELD is the non-custodial part. We’ve all heard the saying “not your keys, not your coins” this is one reason why some don’t trust centralized lending platforms. Most, if not all, of these platforms require you to move your funds to them.

On the other hand, MELD allows you to keep your private keys meaning the ownership is yours. This, however, does not mean that the risk of using MELD is zero. There can always occur smart contract breaches or something else which puts your funds at risk. However, the risk of losing your funds should be lower. You can currently link the account with your Nami wallet, and soon, support will be added for Metamask.

How Does MELD Work?

As mentioned, MELD will have a lot of features, and most of them are still up and coming. Here I’ll go through the most basic features and how they work, and then we’ll look at the rest in the next section. Being a lending protocol, we’ll start with how that works.

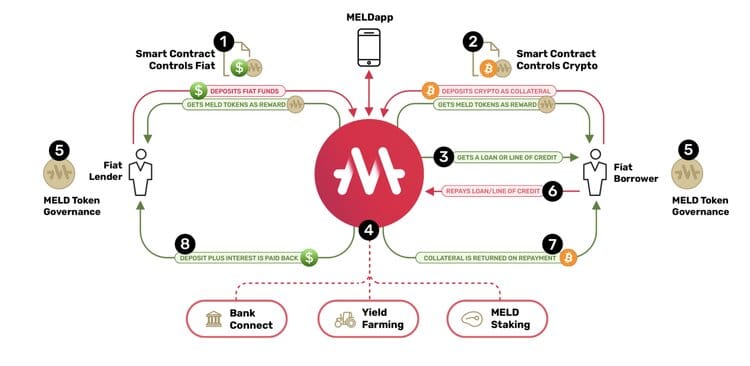

This is how lending and borrowing works on MELD. Image via MELD whitepaper.

This is how lending and borrowing works on MELD. Image via MELD whitepaper. From the picture above, you see how all the pieces fit together, but to make it simpler, we'll go through the procedure step by step (ignore the numbers in the picture). If you go to MELD to get a loan or a line of credit, the first thing you do is provide collateral. The accepted cryptocurrencies are ADA, ETH, BTC, and BNB. After providing collateral, you'll be able to borrow 50% of the value of your collateral and receive the funds to your account as a wire transfer.

The money you borrowed will come from the fiat liquidity smart contract supplied by fiat lenders. Now you have the loan, and as with any loan, you'll pay the interest and principal monthly until the loan is fully paid back, at which point your collateral will be released and returned to you. The interest rate you pay will depend on how much fiat liquidity is available and how many want to borrow, so basic supply and demand economics.

That's essentially how the protocol works if everything goes according to plan from the borrowers' side. As I mentioned, you can borrow in an LTV ratio of 50% (loan-to-value), but it doesn't mean you should and here's why. If the value of your collateral drops so that the LTV becomes 65% or stays over 50% for three days, then a margin call will happen, and you must provide additional collateral to bring back the LTV to 50%. If not provided or the LTV hits 85%, an automatic liquidation event happens.

The collateral is sold for USD/EUR and transferred back to the customer, minus a 5% fee. This is why you need to keep an eye on your LTV and maybe leave some room and not borrow the full 50%. The MELD app will inform you if your LTV changes; the data is sourced to various data oracles.

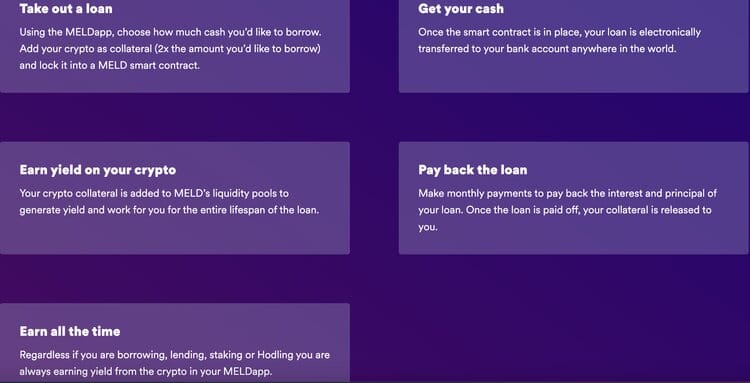

Here's another simple step-by-step guide on how MELD works. Image via MELD.

Here's another simple step-by-step guide on how MELD works. Image via MELD. From the lenders' side, everything is quite simple. You deposit your fiat money into a smart contract and receive yield. The yield is sourced from various features, including the interest paid by borrowers, trading fees, and protocol rewards. To boost your rewards, you can stake the native token of MELD called MELD; I'll cover that in another section. If necessary, you can also withdraw your funds at any point.

That was how the basic loan works and how a line of credit works. The only difference is that you only pay interest on the amount used in a line credit. On top of these two, there will also be another type of loan called Genius loan, so I'll explain that. The reason this loan is called Genius is that it pays itself down. I haven't yet explained what is done with your collateral when you take out a loan. Your collateral is being used in different token pools for yield farming. Normally the rewards earned go partly to the MELD protocol and partly to MELD token stakers.

In the Genius Loan, however, part of the earnings from yield farming is used to pay down the principal. Meaning not only are you are exposed to the capital gain from your collateral, but on top of that, your collateral is earning yield. The only downside to this loan is that you'll need to pay a slightly higher interest. The exact numbers are not yet available but at least thinking about this with basic logic makes the Genius loan sound extremely intriguing.

Also, if you want, you are allowed to pay down the principal, too, meaning you don't have to sit and wait for the principal to be paid if you don't want to. According to MELD's own calculations, it will take 3 and 6 years to pay down a $100k loan, depending on the market conditions.

Additional Features of MELD

Because the whole defi industry is relatively new on Cardano, there isn't yet a lot of infrastructure in place. This applies to, for example, wrapped assets. As you can probably guess, MELD will solve this. MELD will support defi infrastructure to wrap assets. These wrapped assets will be called MELDed assets. The initial stage will only include BTC, ETH and BNB, but the plan is to support other ERC-20 and BEP20 tokens later on. This will be managed through MELD DAO, and a 0.2% fee will be collected on every transaction. The wrapping of BTC and ETH will be done using Polygon, and for BNB, they'll work with the Binance Smart Chain network.

Next up on the list is the MELD debit card. The details around the card are quite thin, while the competition in this space is fierce. The idea is to allow people to spend their money without cashing out of crypto. I don't know the benefit of using their card, but I can imagine that some cashback can be earned. If the card is seamlessly integrated into MELD, I could imagine it could be a nice addition if you're a user of their other services. Also, the card looks quite nice in a picture in their whitepaper.

Hopefully you like the color red. Image via MELD whitepaper.

Hopefully you like the color red. Image via MELD whitepaper.The last additional feature I'll be covering is NFTs. The MELD token was initially distributed to the public through an ISPO (I'll explain in the next section). All of those who participated will be eligible to mint a Banker NFT. This NFT was initially planned to boost your MELD staking APY. However, that has now been trashed, and the utility for these NFTs is still unknown.

Nevertheless, the idea is a fun and engaging feature, in my opinion. The NFTs can be evolved if you're active, and by evolving the NFT, you'll earn additional rewards, so it's not just the NFTs look that changes. Basically, the NFTs would serve as an entrance to a membership club with different tiers.

MELD Tokenomics

As mentioned, MELD has a native token called MELD. This token was first distributed via a private sale. Later, the public could enter through an Initial Stake Pool Offering (ISPO). An ISPO works with people delegating their ADA to a specific staking pool. In this case, MELD had two staking pools where one would give you rewards in MELD and ADA while the other only distributed MELD tokens.

In the first staking pool, MELD acquired 50 % of the ADA block rewards, and in the second, they got 99%. Once the ISPO was finished in December of 2021, all the participants were airdropped their MELD tokens. This solution was done because the MELD team felt this was the fairest way. Currently, MELD is only available on Bitrue and FMFW.io, according to CoinMarketCap, but the team is working on making the token more accessible.

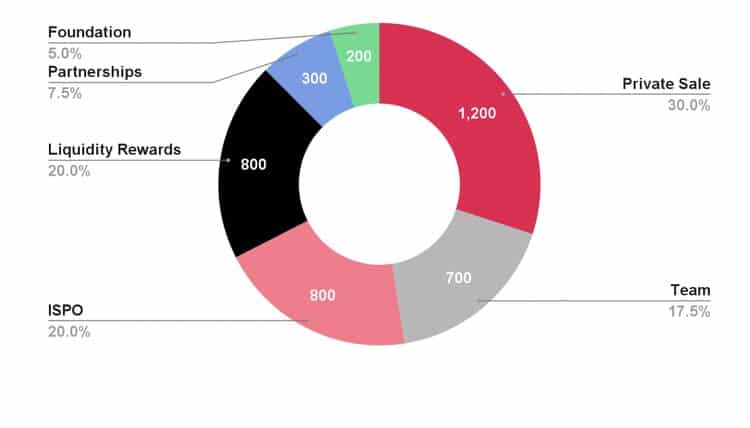

Here's a look at the distribution. Image via MELD whitepaper.

Here's a look at the distribution. Image via MELD whitepaper. From the image above, you see the token distributions in percentages. While the ISPO itself might have been quite fair, the allocation to the public is relatively small. When it comes to vesting schedules, I’ll leave a picture down below, but essentially all participants will have their tokens released gradually. The team and advisors will have to keep their tokens locked up for 9 months after the token launch, and then they’ll be released 4% a month. The private sale investors will be able to unlock their tokens from the beginning with a 4% a month rate, meaning they don’t have the 9 months lock-up.

As you can see, the inflation in added liquid supply will be quite aggressive initially, after which it’s flat. The total supply is 4 billion tokens, and it should stay at that. However, there is a chance that the token could become deflationary since 20% of the collected fees will be allocated to buyback and LP funds.

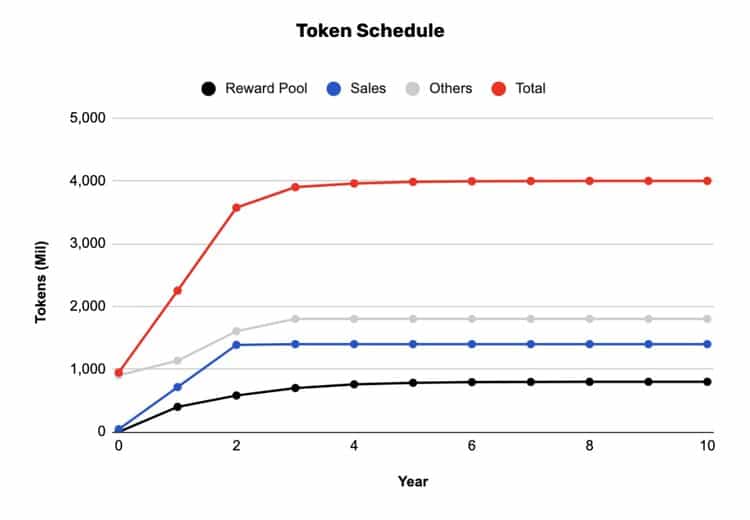

And here's a look at the MELD vesting schedule. Image via MELD whitepaper.

And here's a look at the MELD vesting schedule. Image via MELD whitepaper. The rest of the collected fees will go to staking pools and the Foundation. The staking pool is obvious, but the Foundation will require some explanation. As mentioned, the Foundation will have a role in running the protocol. Therefore, they will get a part of the fees and distribute that to research, development, grants, foundation reserves, and maintenance. The fees that MELD takes is the already mentioned 0.2% fee from wrapped assets. On top of that, there's a 3% fee on margin loans and a 0.3% for swaps. The fee structure is quite conservative, and in the next section, you'll see that the fees could be higher compared to others.

As I believe I've mentioned here somewhere, the MELD token can be used to boost your rewards as well as for governance. Already you can stake your MELD tokens for a 12.5 % APY. Currently, there's only a 6-month staking pool meaning your funds will be locked up, but a flexible pool is coming soon. The governance part is also yet to be significant since MELD is not yet fully decentralized. Once MELD enters stage 3 of decentralization, you'll be able to use your MELD tokens to vote for improvement proposals, but this might take a while since currently, we're in stage 1.

MELD Compared to Others

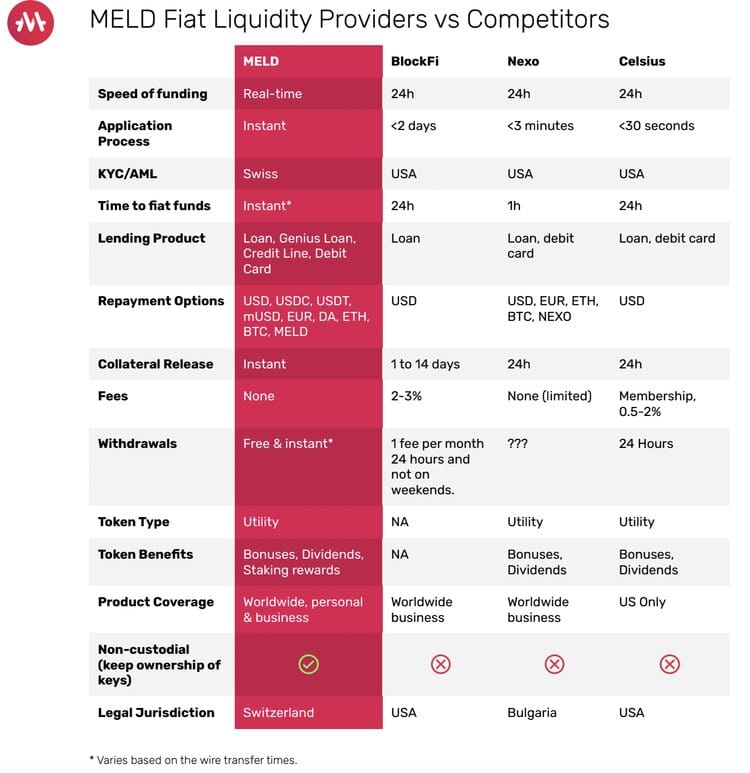

You'll see how MELD compares to some well-known cefi platforms from the picture below. While it seems that using MELD is a no brainer, we do need to be a little critical. First, MELD does not really offer the same things compared to the others. The other platforms are fully functional and add to and improve their services as we speak.

The offering of these platforms has improved and become substantially wider from the time this whitepaper was written. MELD, on the other hand, doesn't have any of their core functions functionality just yet, meaning theoretically they sound better than others, but in the real world, they're far behind. Now that doesn't mean they can't become the best; it just means that all of what they're saying is only theoretical at this point.

This is how MELD compares themselves to others. Image via MELD whitepaper.

This is how MELD compares themselves to others. Image via MELD whitepaper. However, if we look at these things without accounting that MELD isn’t fully operational, they have some exciting benefits. First of all, as I already mentioned, the Genius loan itself sounds extremely intriguing, and I think it can be a good demand driver for MELD if the interest rate isn’t too high. Another thing I also mentioned as a substantial benefit is the non-custodial part which I believe will also be a good demand driver.

Some other things I believe users will appreciate are the quickness of both taking a loan and having your collateral released. The point is to avoid the banks and their long lines and waiting times. With MELD, everything moves quickly, and before you know it, you’ll have your funds and be able to do anything you want. And lastly, the part that you don’t have to pay anything for withdrawals makes it much simpler to decide to use the protocol.

I also need to mention before moving on that there are only a few competitors from a wide selection in this list. From this article, you’ll find a comparison between top cefi platforms. Also, because the whitepaper is made by MELD, you’ll only see the things MELD can compete with. For example, many prefer these cefi solutions because they work like traditional companies. Many of these have good customer service that will help you.

They also have significant insurance funds if something goes wrong. Another benefit of these platforms is that they provide reasonable rates for borrowing crypto. This isn’t available on MELD, and if you’re looking for a complete package, something else might be better for you. I genuinely suggest you look at the article I linked to and see which service sounds the best for you. But of course, nothing stops you from using multiple services for different purposes.

MELD Roadmap

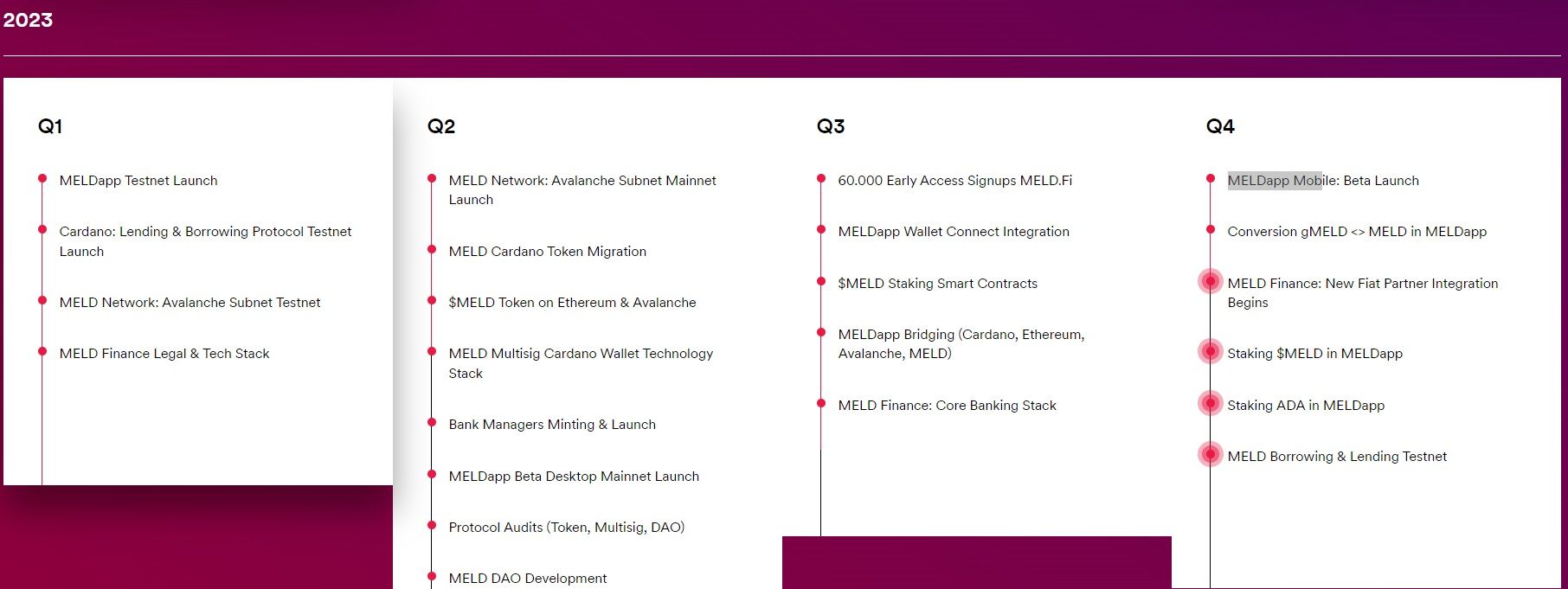

The MELD roadmap is quite extensive since, as I’ve made clear multiple times in this article, there aren’t a lot of features available just yet. Now, most of you probably want to know when we’ll see the most basic functions like borrowing and lending, and I’m sad to tell you that you’ll have to wait.

The borrowing and lending testnet is set to live in the fourth quarter of 2023. Also slated for the same quarter is the ability to stake the MELD and ADA tokens on the MELDapp. The app's mobile beta is also expected to be released in the fourth quarter.

The MELD Roadmap. Image via MELD

The MELD Roadmap. Image via MELDMELD Protocol Review: Closing Thoughts

On paper, I have to hand it to the MELD team that they’ve done an excellent job, and I believe they’ve got a chance to become a top tier defi protocol. The competition is fierce, and it might be hard to distinguish from them, but the team seems to know where to take the project to do that. Still, everything has to be proven, and before I see a working product, it’s hard to give them all too much credit.

One concern is that if their launch dates are pushed much further back, they might be too late in the game. As mentioned, their competitors are consistently improving their own products. I believe that changing services is a far higher barrier for many than to start with one, especially if you’ve already locked up a substantial amount of funds on some other platform or maybe even have a loan from some other place.

With MELD, we will just have to wait and see what happens. Hopefully, they can gather a good client base, including some institutions and also some from the unbanked. There’s no denying that a service like this is both equally wanted and needed.