When it comes to my emergency cash needed on hand, I’m happy for it to be chillin’ in the bank and not earning anything in the way of interest. My crypto assets, however, need to get themselves working for a decent salary. While shopping around for a rock-solid crypto platform to park my assets in, I came across YouHodler through an ad from the Brave browser (where I can earn some BAT tokens by ignoring most of the ads they flash at me). The name of the platform struck me as slightly cheesy but hey, don’t judge a book by its cover, right?

⚠️Safety Notice⚠️- In light of the liquidity issues faced by the lending platforms Celsius, BlockFi, Voyager, and others, which resulted in lost customer funds, we recommend users do extra due diligence on centralized crypto platforms they are considering and practice safe financial habits such as diversification and self-custody when possible.

What is YouHodler?

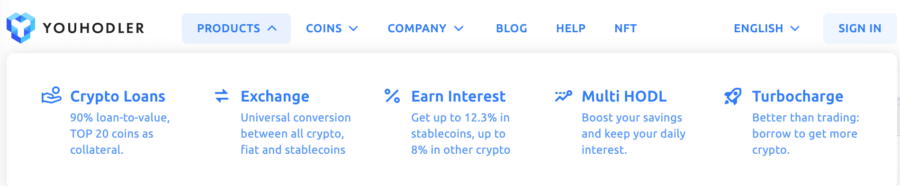

YouHolder is a centralised crypto-lending and borrowing platform offering services that caters to lenders and borrowers to earn interest and obtain loans. It also offers an exchange service to swap between fiat and crypto or two kinds of crypto. What makes it different from other platforms of similar functions are the MultiHODL and Turbocharge products that help users maximise their returns in a risky manner.

Products and services offered on YouHodler Image via YouHodler

Products and services offered on YouHodler Image via YouHodlerExchanging Between Fiat and Crypto

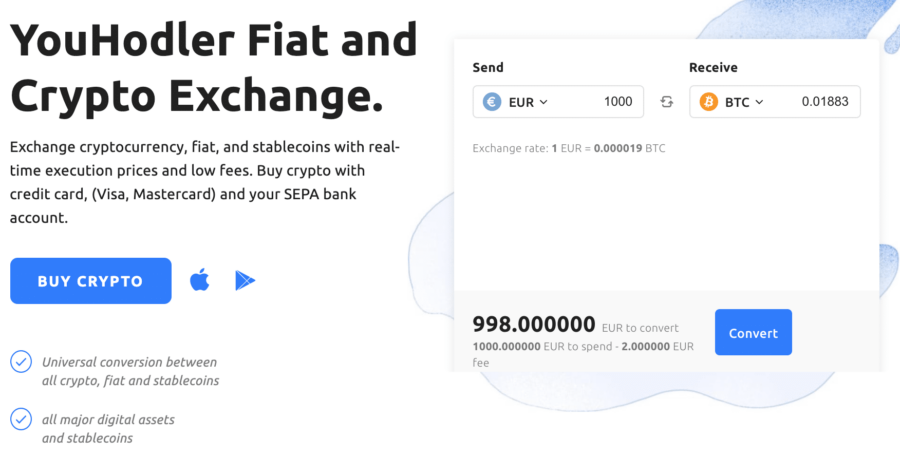

For those new to the crypto space, YouHodler offers an exchange service for swaps between fiat and crypto. You can deposit your cash in this platform and exchange them for crypto. It is also handy for those who want to swap the other way around.

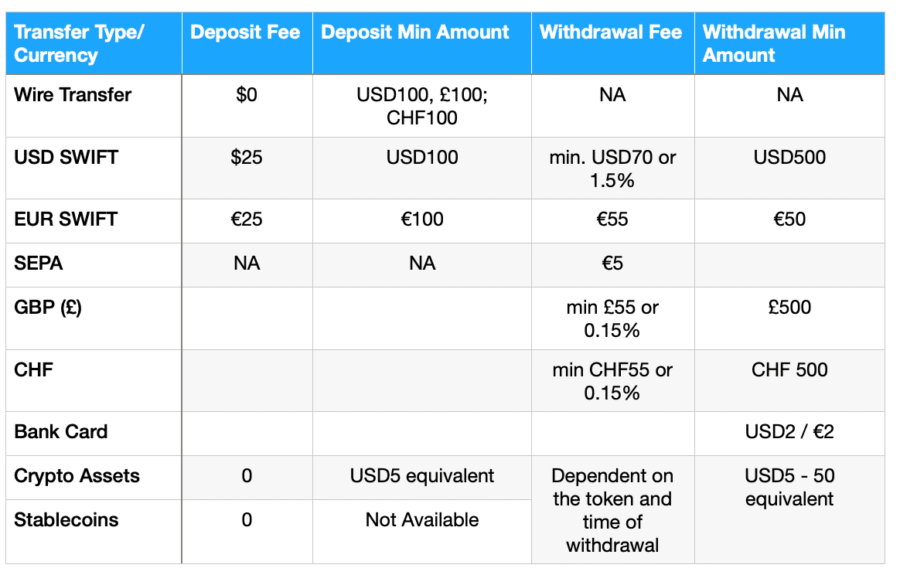

A straightforward way to exchange fiat and crypto

A straightforward way to exchange fiat and crypto The rates may differ based on the cryptocurrency swapped but here's a chart for deposit and withdrawal fees for your reference:

Check carefully before making any deposits or withdrawals

Check carefully before making any deposits or withdrawalsThe minimum deposit required to get started is $5. Opening an account with YouHodler requires going through the Know-Your-Customer ( KYC) process. This is where you are required to upload personal information, tying up your identity with the account. This step is a necessary element of the Anti-Money-Laundering (AML) policies enacted to prevent criminal activity.

After that, the next thing to consider is the security of the funds held on the platform. There are two main elements that are of key importance: insurance and the people running the company.

Insurance by Ledger Vault

The platform’s homepage advertises that it uses Ledger Vault to provide up to $150 million of pooled crime insurance. What does that mean really? To answer that question, I decided to take a quick peek at Ledger Vault and here’s what I found out:

- It is an enterprise-level product by the Ledger company (the same ones that make my Ledger cold wallet).

- It is a program for managing private keys that has access to the storage area where tokens are kept.

- Ledger Vault is relied on by one other lending platform, unlike some of its competitors which offers safety to a few. This is good because in the event of a major event, the number of companies seeking insurance at the same time is less.

In other words, access to the tokens are as well-guarded as those hi-tech bank vaults shown in action movies. The weakest link therefore, are the people who have access. Let’s direct our spotlight on the team.

YouHodler Background

YouHodler was set up in 2017 and there are two companies running it: Naumard Ltd based in Cyprus and YouHodler SA in Switzerland. I'm slightly raising one eyebrow here about the Cyprus location because of its 'golden passport' scheme that raised a bit of a kerfuffle.

Three key personnel are listed on the website: Ilya Volkov the CEO, Renat Gafarov the CTO, and Alex Vinny, Head of Product.

Ilya Volkov, CEO and Founder

Ilya graduated with a degree in Philosophy in Moscow before venturing into the FinTech world. He’d spent 10 years in Commercial Finance followed by another 10 years in online trading. In a recent interview, he shared his journey on starting YouHodler inspired by the LUMIAMI approach and Design Thinking. He sees YouHodler as an integral piece that connects banking, trading and cryptocurrency. This is certainly reflected in the offerings on YouHodler.

Renat Gafarov, CTO

Renat started his career as a frontend developer, quickly moving up the ranks while also going through multiple companies. His current stint at YouHodler is the longest he’s been in a company (4 years).

Alex Vinny, Head of Product

From what I can tell, I think Alex went to the same university as Renat, Altai State University in Russia. He is also connected to Ilya via The Forex Club where he worked, first as a UI/UX Designer, then a Product Designer before joining YouHodler as a UI/UX Designer.

The management team looks like they come from rank-and-file backgrounds, which is something I like because it means they know what they’re doing in their area of expertise. The risk is that there is not a lot of management experience, which hopefully, will be addressed as the company scales up.

In terms of how likely they will run away with everything in the middle of the night, aka do a rug pull, in that interview with the founder, his intention to build something better is convincing enough. Unless I can dig up more dirt about them, which isn’t easy because they seem fairly low-key, I am cautiously positive.

At this point, knowing what you know about the company, you can decide if you'd like to continue exploring the platform and the other services it offers. For myself, I am curious to see what else is available, so am proceeding with caution.

How Does it Work for Lenders?

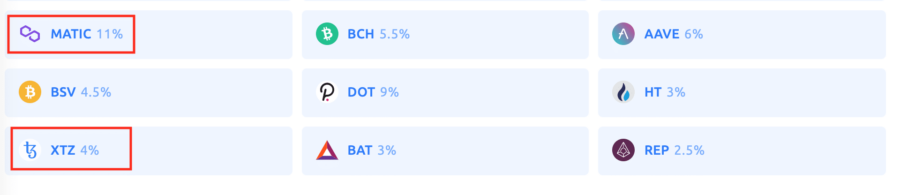

The selling point on the website is that you can get up to 12.3% interest annually for both crypto assets and fiat. Usually, with these kinds of claims, there’s a bit of truth-stretching involved. Nice of them to provide a earnings calculator for me to check what I’m most likely getting for my crypto tokens. Here’s what I found out (in order):

- MKR, COMP, REP 2.5%

- HT, BNB, BAT, BNT, DOGE, OMG 3.0%

- XLM, XRP, YFI. ZRX 4.5%

- BTC 4.8%

- EOS 5.0%

- LTC, BCH, DASH, ETH 5.5%

- SNX, ADA, AAVE 6.0%

- LINK 6.2%

- UNI, SUSHI, TRX 7.0%

- PAXG 8.2%

- DOT 9.0%

- BUSD 10%

- EURS, USDP 12%

- USDT 12.3%

Comparing my findings with their published list below, I noticed it has two tokens which were not from the dropdown menu of the calculator (marked in red). I wonder why.

Accidental oversight?

Accidental oversight? In general, I like the idea of getting weekly interest payments, especially if it can also be compounded. The interest paid is also in the currency/token deposited. There’s no requirement to accept a platform’s native token in order to earn a better rate. I suppose there are two ways to look at this:

- There is security in having interest paid in the original form. For example, I’d take interest in BTC any day over any native token.

- If there is a native token, then what you’re banking on is that the amount of interest in the original form is less than what you could potentially get with the native token, especially if the native token is doing well and fetches a higher price in the market. This would require an additional layer of monitoring. How much work are you willing to put in when it comes to keeping an eye on your assets?

There’s also the flexibility of withdrawing my crypto anytime. It’s worth noting that I won’t get any interest for the week that I make the withdrawal.

Putting my crypto to work here would require me to deposit a minimum of $100 worth of each type of asset I want to earn interest on. Eg: If I want to earn interest for BTC, USDT, ETH, and UNI, I would need to lock in a total of min $400 worth of tokens in my account. No wonder they have a maximum deposit amount of $100k across all currencies. Compared to other platforms that have no minimum, this is a bit of an entry barrier.

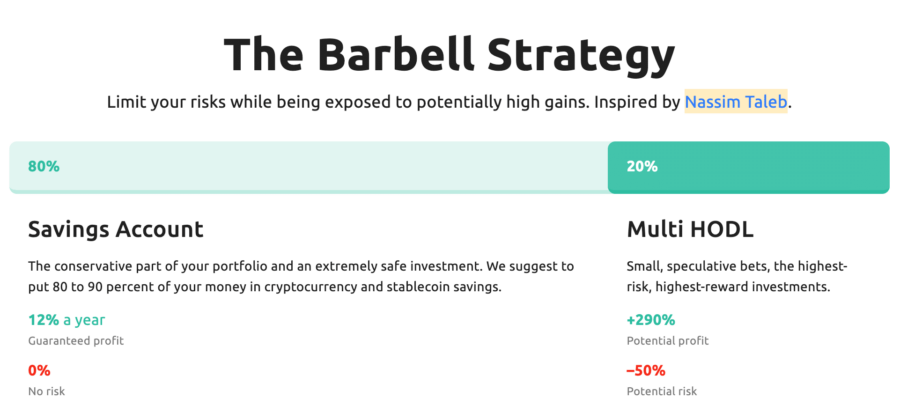

MultiHODL

One thing that makes YouHodler unique from other platforms for lenders is the MultiHODL product. The key idea for this product is based on something called The Barbell Strategy by Nassim Taleb, a mathematician and risk analyst, famous for his book “The Black Swan”.

How it works

Let’s say:

- I put in $1,000 in USDT. 90% of it is in a deposit, and I decide, with 10% of my deposit, i.e. $100 on a crypto token like AAVE, that its price will go up.

- I open a position, i.e. I place my bet. Then I watch and wait to see what happens.

- If I’m wrong, I lose the hundred dollars.

- If I’m right, I could stand to gain more than 12.3%, depending on where I set the level of profit-taking. The profit goes directly into my account.

- I get to decide how long to keep the position open or when to close it. There is a fee associated with the duration of the open position.

Also, the position will automatically close after 10 days (in case I forget about it), or if the price falls below the level of loss. Other than stable coins, I could also use other crypto tokens as capital too.

Learning about risk with training wheels on.

Learning about risk with training wheels on. The mechanics of how the bet placement works is similar to margin trading, where one sells another’s shares, then buys back the shares at a later price, either lower or higher than predicted. It’s usually paired with leverage, i.e. I put in $100 and buy $200 worth (that’s a 2x leverage). If things go wrong, I could stand to lose $200.

Margin trading has always been something I’d shy away from because I’m not comfortable losing more than what I’ve put in. With the MultiHODL product, leverage is an option. They call it “multiplier”. There’s a slider to choose how far you want to go. Of course, the more you multiply, the higher the risk/reward.

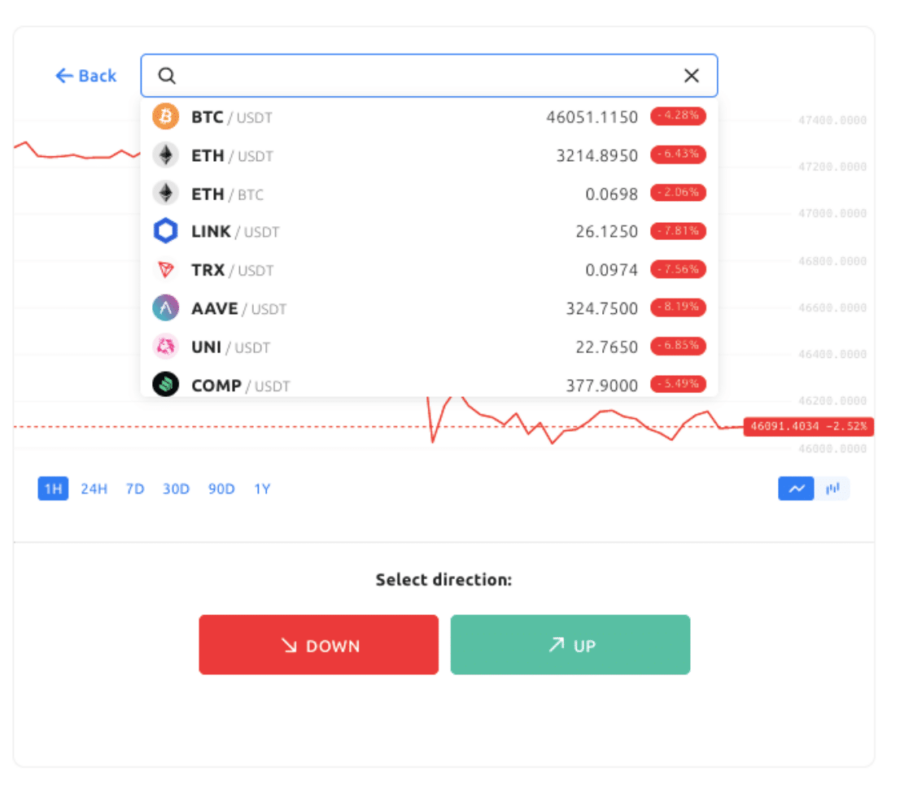

Give your chart-reading skills a test

Give your chart-reading skills a test If you’re getting started in crypto trading and got a bit of knowledge in reading charts or doing technical analysis (TA), you could consider testing out your hypotheses here, whether the price will go up or down. If not, and you’re feeling lucky, just close your eyes and pick something. You have a 50-50 chance of being right anyway.

That being said, it’s worth giving it a go with a small amount, like nothing more than 10%. If you’re not sure of your risk level, try asking yourself: if I wake up the next morning and I found out that I’d lost the amount I’d put in, how awful would I feel on a scale of 1 to 5?

Unlike the deposit-and-earn scenario, which is pretty much set-and-forget, doing the MultiHODL way requires a bit of effort to monitor your bets. If monitoring can be a stressful thing, I suggest skipping this product.

As for me, I’m just about ready to throw my pitiful BAT stash into this platform and allocate maybe 20% of my BAT holdings to this product. But wait, there are fees to consider:

- one-time origination fee

- rollover fee - the hourly fees during the duration of the bet

- one-time 10% profit share fee

Example of Rollover fee calculation

Example of Rollover fee calculation How Does It Work for a Borrower?

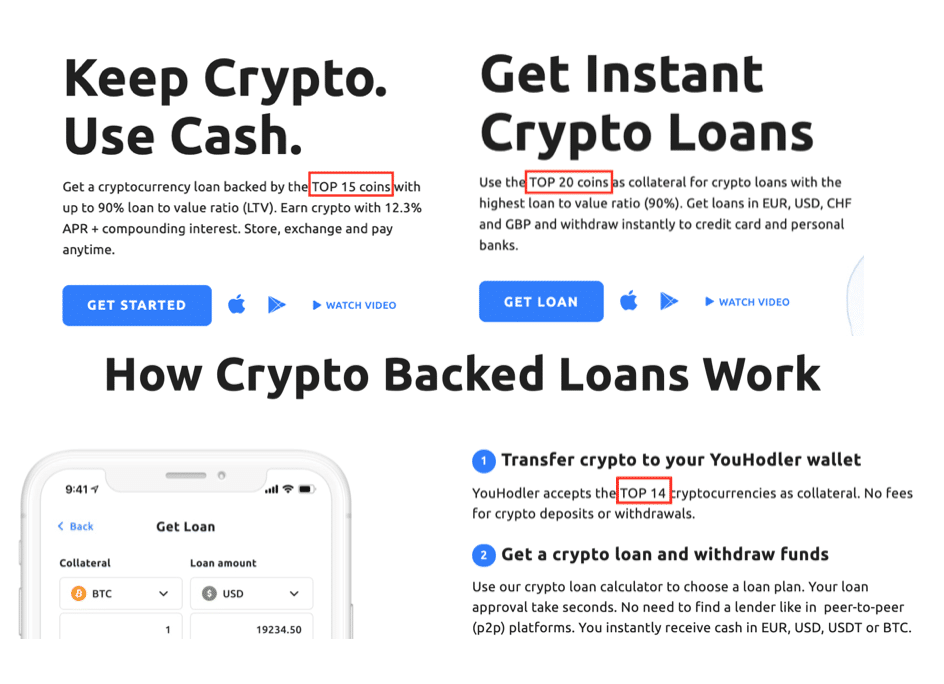

According to their loan page, the top 20 coins used as collateral can be used to secure up to a loan of up to 90% of the collateral value. This is commonly known as Loan-To-Value ratio, aka LTV. In this case, a 90% LTV means I can get $900 from collateral that’s worth $1,000. Whoa!

Further down the page, I noticed that it said top 14 coins as collateral. However, on the homepage, the advertising said top 15 coins. This kind of confusing messaging doesn’t sit well with me. If it's a genuine error, they need to pay more attention to their copywriting; if it's not, could something else be afoot? It didn’t help that the top coins were not listed.

It's things like this that triggers my alarm bell.

It's things like this that triggers my alarm bell. Getting a Loan and Risks

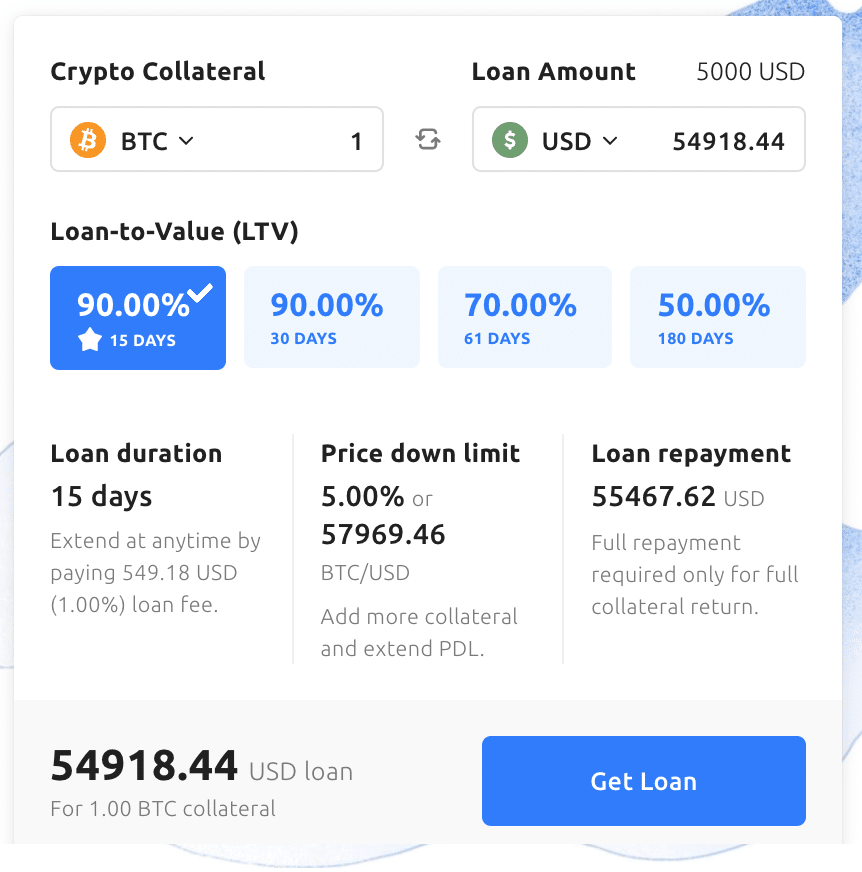

The shorter the loan period, the higher the loan amount is available.

The shorter the loan period, the higher the loan amount is available.As with all crypto platforms that uses smart contracts, as long as you have the required collateral, you’re practically guaranteed to get the loan. The downside is the risk of instant liquidation if the collateral amount is worth less than the loan amount, especially with the volatility in the market. This is where Price Down Limit (PDL) comes in. It’s like the minimum number of items in the warehouse waiting to be sold. Once that minimum number is reached, it’s time to order more stock before you run out of items to sell. In this case, once 2/3 of the Price Down Limit is reached, the YouHodler team will reach out to you to ask for more collateral. If you would like to add more collateral to the loan, you activate the Extend PDL function.

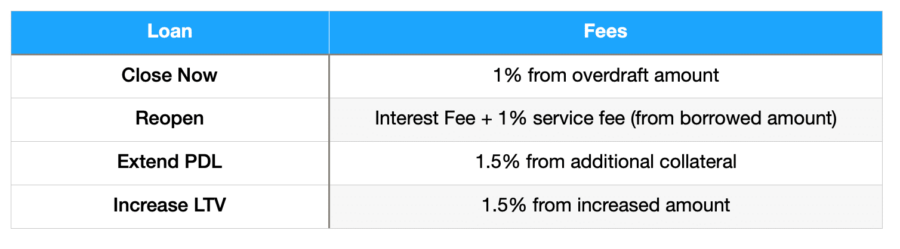

In addition, you can also do one of the following for your loan:

- Close the loan using the Close Now function - this allows you to not repay the loan by having your collateral liquidated.

- Set Close Price feature aka Take Profit - Set the price where you want to take profit. Once it reaches that price, part of the collateral is sold to repay the loan and the rest is deposited into the account. This can be defined upon applying for the loan or for the duration of the loan.

- Reopen feature - extend the loan without repaying it by activating this function. Fees apply every time the loan is extended.

Last but not least, let's check out the loan parameters and fees.

- Loan minimum: $100 or its equivalent.

- Loan maximum: varies according to market conditions and collateral used.

- Loan currency: USD, EUR, CHF, GBP, BTC and Stablecoins

- Loan repayment methods: crypto (by converting it to fiat), wire transfer, debit/credit card, from account, Close Now feature

Fees associated with the loan function

Fees associated with the loan function Turbocharge

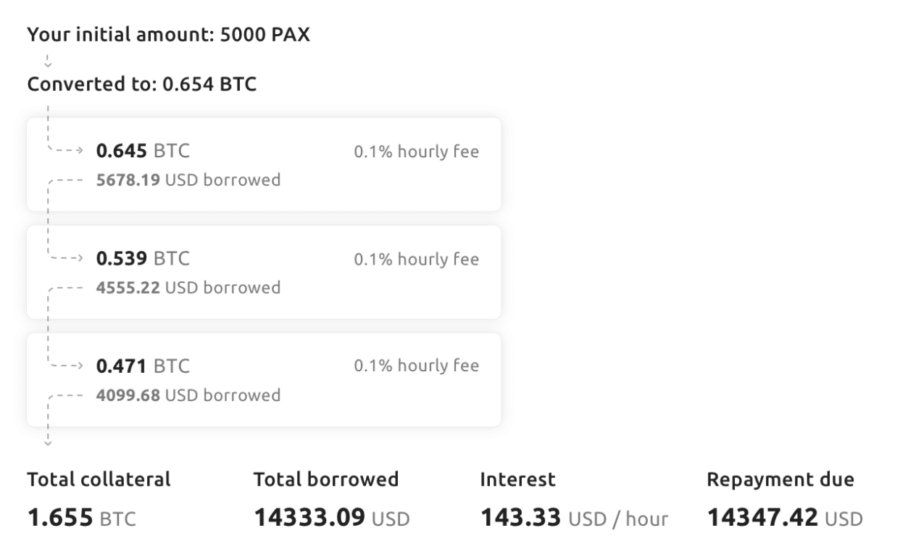

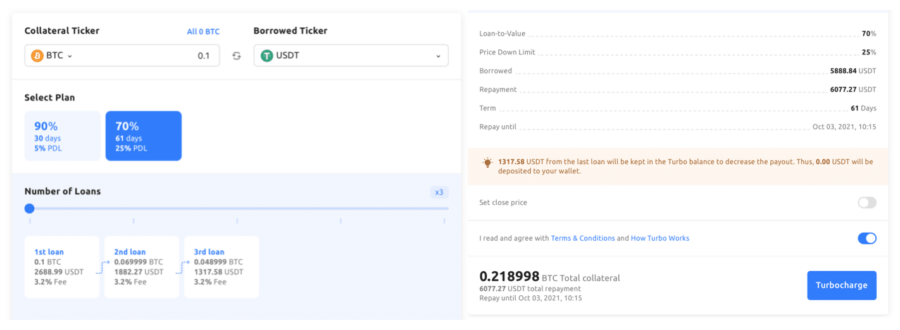

The classic-loan scenario above is for those who want to use their crypto as collateral to get cash. But what if you want to make money from your crypto? Now you're talking about leverage. It's like using the still-mortgaged first property to act as collateral to take out a mortgage for your second property. Imagine that we're talking about loans in this same fashion. Let's say you deposit collateral that gets you $1,000. Then, you use that amount to get a second loan, which gets you $800. It then becomes the "capital" for the third loan and so forth.

That's essentially what Turbocharge is, another unique product only offered on YouHodler. This product is designed based on the "cascade of loans" principle which sounds, to me, like a most dangerous phrase. It's nothing more than the domino effect in action but in, hopefully, a positive way, i.e. everything going up instead of down. While it may feel like you only need to be out of wallet once for the first loan, and you're using "free money" to take out the next loan and the one after, you are still responsible for the whole lot. All it takes is one loan to default and the entire thing will come tumbling down like a house of cards. I want my crypto assets to be working hard, but I don't need them to be doing hard labour in a chain-gang!

This is what happens in a Turbocharge loan

This is what happens in a Turbocharge loan If you really want to have the experience, then do something really small, like the minimum of $100 and take out not more than 3 loans to get a taste, not max it out at 15 times. Exercise extreme caution here!

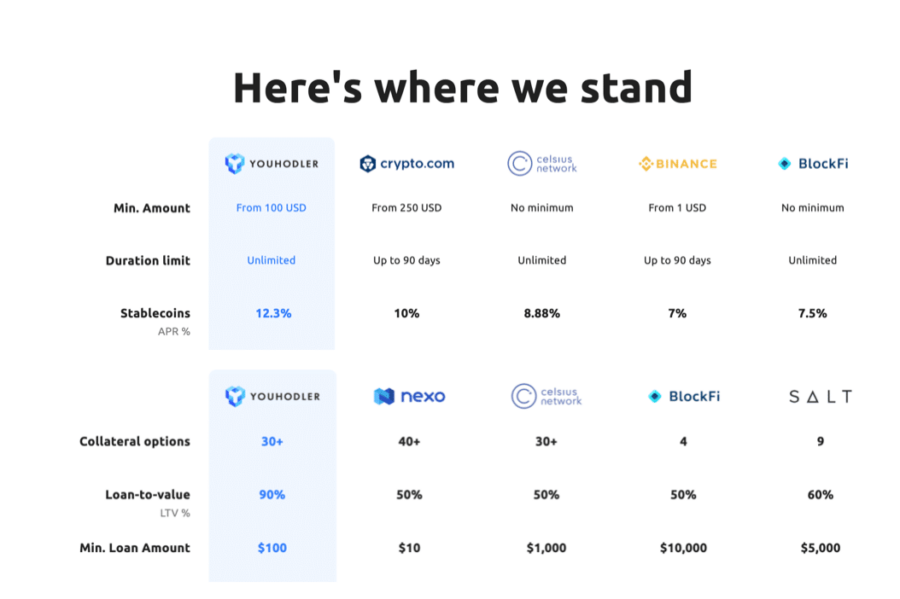

Competition

There is no shortage of competition for the space that YouHodler operates in, as the image below shows:

When in doubt, shop around

When in doubt, shop around Since this chart was compiled by YouHodler, it is reasonable to find that it paints the platform in a fairly flattering light. Despite that, it also knows it's not the best in everything and probably doesn't try to be. With the two unique products it offers, it has confidence enough to capture the number of users it needs to remain healthy and competitive.

If you are interested in YouHodler alternatives, be sure to check out our Top CeFi Platforms article.

General Safety and Risks

Ever since the data leak issue from 2019 occurred, YouHodler has beefed up their security including 2FA password protection ("what you have and what you know") for all their users. They also included a 3FA security measure for those with more than $10k in their account that allows the users to disable all withdrawals. If a withdrawal is necessary, there will be additional verification steps taken to make this happen. Traditionally, 3FA requires some kind of pre-authorisation of the machine where you perform the task. A dedicated digital certificate on the machine is a common way to do this. Whether YouHodler takes this route in their definition of 3FA, I don't know. It's worth taking note of.

When it comes to regulatory concerns, i.e. the platform getting shut down by some government, it's unlikely to happen, given where they have their headquarters in.

One key point of concern is how the platform actually makes money. While it is possible to believe that the fees they collect from the users' transactions would be enough to cover all costs related to the operations of the company, there isn't anything in the website that gives a clear indication of their business model. Some of their competitors openly mention loaning amounts to institutional investors via rehypothecation. This means that the deposited collateral is used as a pledge for another loan made by the company on its own behalf. YouHodler does not mention this but it does not mean they are not doing it. More transparency in this matter would be helpful to know.

Conclusion

As platforms of this nature goes, YouHodler is no worse than what's out there. The two unique products they have currently gives them an edge, but only until the next best thing comes along. I would not be parking all my assets onto one platform because diversification is important. Here's what I would do:

- Put in a small amount, maybe slightly above the minimum amount of $100 to get started on earning interest.

- Once the interest accumulated has reached a sizeable level for me, I'll allocate half of the extra interest into the MultiHODL product to make educated guesses of the market trends.

- With the other half (min $100 in value), I will put it in a Turbocharge loan 3 times over to observe what happens.

- Last but not least, I'll withdraw the extra profit earned and buy myself some ice-cream. (After fees are deducted, probably the only thing I can afford!)

After weighing all the risks and benefits, I think it's worth going through the KYC process to give this platform a try. The amount of money I'm risking is not an amount I will lose sleep over. If everything turns out peachy, it will be a nice surprise.