Editor's Note (March 21, 2026): We fully updated this review in March 2026 to reflect the current state of Pendle Finance and make the platform easier to understand for everyday DeFi users. The refresh adds clearer explanations of PTs, YTs, standardized yield, fixed-yield strategies, and Pendle’s role in tokenized yield markets, while also sharpening the risk section and overall structure of the review.

Pendle Finance Review 2026: Quick Verdict

Pendle Finance is one of the most innovative DeFi protocols for yield tokenization, giving users a way to separate fixed yield and variable yield exposure through PT and YT. It stands out for maturity-based positioning, a specialized AMM, and stronger risk-management flexibility than most DeFi earn platforms, but it is still much better suited to experienced users than complete beginners.

Best For

- Experienced DeFi users who understand yield-bearing assets and maturity-based positions

- Investors seeking fixed yield exposure through PT rather than relying on fully variable returns

- Traders who want to speculate on future yield through YT and implied yield shifts

- Users who actively manage positions across expiry dates, yield changes, and market conditions

Not Ideal For

- Beginners who want simple passive yield without tracking maturity or pricing complexity

- Users who do not want to manage PT, YT, or variable-yield exposure actively

- Investors uncomfortable with DeFi smart contract risk and third-party asset dependencies

- Anyone looking for a basic lending-market experience rather than a structured yield protocol

Caution: Pendle’s structure is powerful, but its mix of DeFi smart contract risk, underlying asset risk, maturity mechanics, and AMM pricing complexity means it rewards understanding and punishes casual clicking.

Scored Summary

| Innovation | 5/5 Pendle Finance remains one of the most original DeFi protocols thanks to yield tokenization, PT and YT markets, and maturity-aware trading design. |

|---|---|

| Ease of Use | 3/5 The app is usable, but the mechanics behind fixed yield, variable yield, maturity, and pricing are not beginner-simple. |

| Risk Management Utility | 4.5/5 PT offers a cleaner route to fixed-yield style exposure, while YT gives advanced users a direct way to position around future yield expectations. |

| Yield Opportunities | 4.5/5 Pendle offers strong flexibility for users who want to trade, hedge, or restructure yield rather than passively accept whatever the market delivers. |

| Accessibility for Beginners | 2/5 Pendle is less suitable for users who just want straightforward passive income without managing maturity, PT, YT, and structured DeFi risk. |

| Overall Verdict | 4.5/5 Pendle is a standout DeFi protocol for advanced users who want more control over fixed yield, variable yield, and maturity-based positioning, but it is not the easiest entry point for newcomers. |

Key Takeaways

- Pendle turns yield-bearing assets into separate principal and future-yield claims instead of leaving them bundled together.

- The protocol is most useful when you have a clear view on predictability, yield direction, or how much time remains until maturity.

- Its AMM is designed specifically for time-sensitive assets, which is a major reason the PT and YT model works in practice.

- vePENDLE still matters for understanding Pendle’s tokenomics history, even as the protocol transitions toward newer staking mechanics.

- Pendle is impressive because it gives DeFi users more control, but that control comes with a steeper learning curve.

Disclosure and Methodology

Some links in this article may be affiliate links. If you choose to use a service through these links, we may earn a commission at no additional cost to you.

For this review, we evaluated Pendle Finance’s protocol design, yield tokenization model, PT and YT mechanics, AMM structure, token incentives, supported ecosystems, and publicly available documentation on functionality, security, and risk.

What Is Pendle Finance?

Pendle Finance is a DeFi protocol built for yield tokenization. In simple terms, it lets users split a yield-bearing asset into two tradable pieces: the principal and the future yield.

That design is what makes Pendle different from a standard earn platform. Instead of depositing an asset and passively accepting whatever variable yield shows up, users can separate the fixed-value side of the position from the yield side and trade them independently through Pendle V2.

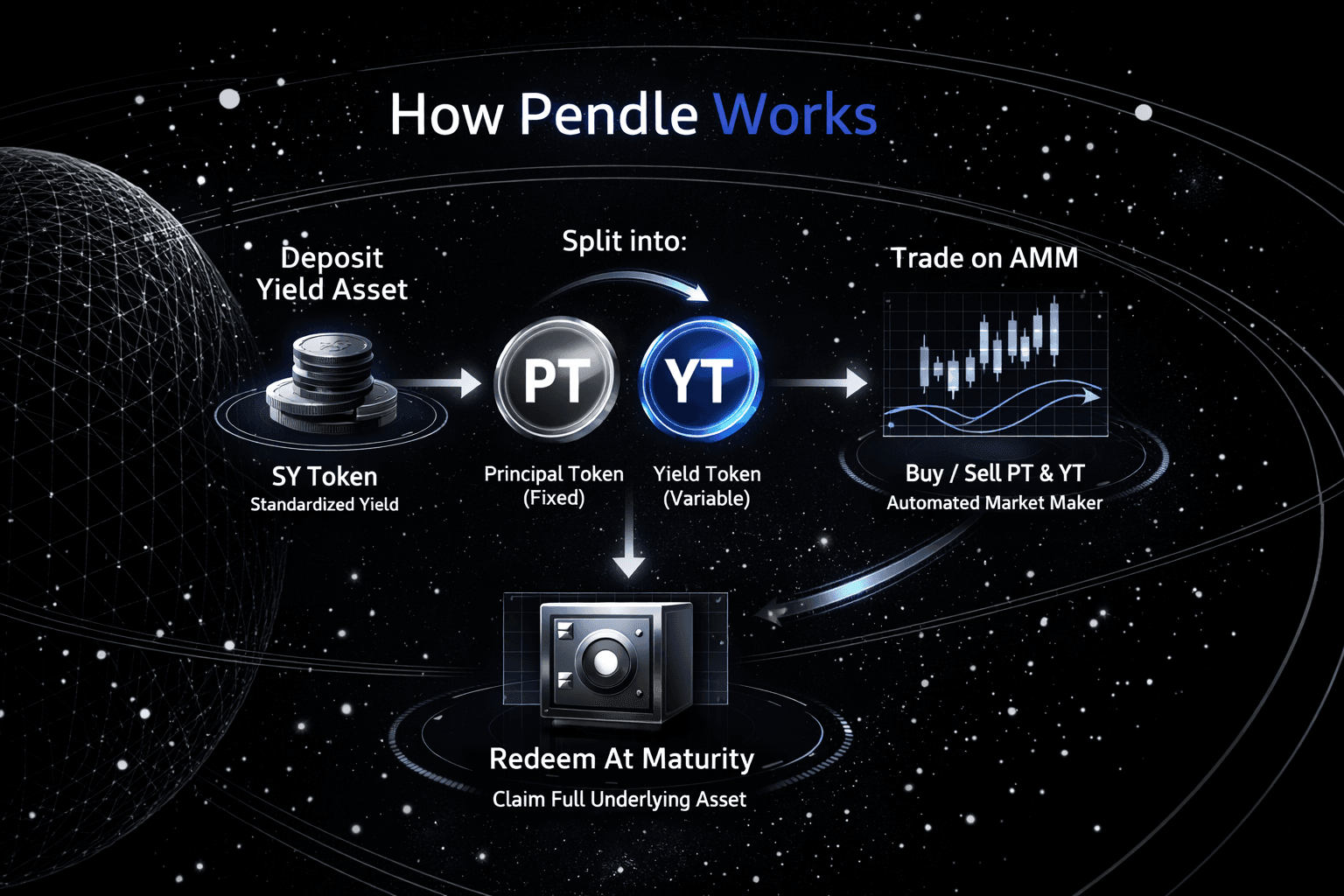

At the center of the system are Principal Token, or PT, and Yield Token, or YT. Pendle first wraps yield-bearing assets into Standardized Yield, or SY, which gives different assets a common format inside the protocol. That SY position can then be split into PT and YT. PT represents the principal claim, while YT represents the right to receive future yield and rewards until maturity.

Why does that matter in DeFi? Because most yield products lump everything together. You deposit into a vault, staking protocol, or stablecoin strategy, and your exposure to principal and yield stays bundled in one moving piece. Pendle changes that by turning yield itself into something tradable. That opens the door to fixed yield strategies through PT, yield trading through YT, and more deliberate positioning around implied yield, maturity, and market expectations.

Pendle V2 also matters here because it made the product cleaner at the protocol level. With SY as the standardized base layer, Pendle can support a wider range of yield-bearing assets without forcing users to think through every technical wrapper behind the scenes. The result is a DeFi protocol that feels less like a passive yield farm and more like a yield marketplace.

That definition sets up the next part naturally. Once you understand that Pendle turns one yield-bearing asset into separate principal and yield claims, the real question becomes how those pieces work in practice, and why maturity changes everything.

How Pendle Works

Mechanism Behind Tokenized Yield And Interest Rate Trading

Mechanism Behind Tokenized Yield And Interest Rate TradingNow that the basic definition is in place, the mechanism makes more sense. Pendle does not create yield from thin air. It takes an existing yield-bearing asset, restructures its cash flows, and gives users different ways to trade or hold those flows depending on what they want from the position.

That restructuring is what turns Pendle from a simple yield app into a proper yield market. To see how it works, you have to start with the three building blocks that sit underneath every Pendle V2 position.

The Core Building Blocks: SY, PT, and YT

Pendle V2 begins with SY, short for Standardized Yield. SY is the wrapped form of a yield-bearing asset inside the protocol, and it gives Pendle a consistent base layer for handling different sources of yield across DeFi. Instead of treating every asset as a special case, Pendle standardizes them first and then builds the rest of the system on top.

From there, SY can be split into two separate claims. The first is PT, or Principal Token, which represents the asset's principal and is redeemable on the maturity date. The second is YT, or Yield Token, which represents the future yield generated by that asset until maturity. Once the split occurs, users are no longer dealing with a single bundled position. They are dealing with two different exposures, each with its own pricing logic and strategy.

Maturity is central to everything here. PT and YT do not float in an endless timeline. They exist with a defined maturity date, and that endpoint shapes pricing, implied yield, and trader behavior across the market. The closer a market moves toward maturity, the more the relationship among principal, future yield, and time tightens.

What Happens When You Buy PT

Once Pendle splits an SY position, PT usually trades below the underlying asset's value before maturity. That discount to maturity is why PT is often treated as a fixed-yield instrument in DeFi. If a user buys PT at a discount and holds it until maturity, the token can typically be redeemed for the underlying asset, assuming the underlying structure performs as expected.

That price gap is where the fixed-yield style exposure comes from. The return is not presented the way a traditional bond desk would, but the logic is familiar. You buy below redemption value, hold through maturity, and the gap between entry price and redemption value translates into an implied yield or fixed APY-style outcome.

This makes PT attractive for users who care more about predictability than upside. Instead of staying exposed to variable yields, they can use PT to lock in a more defined return profile. In a market where yields can move quickly, that kind of structure is one of Pendle’s strongest draws.

What Happens When You Buy YT

If PT strips out the principal side, YT takes the other half of the trade. Buying YT gives a user exposure to future yield until maturity, along with any associated rewards that flow through that position. In other words, the buyer is making a directional bet on how much yield the underlying asset will generate over the remaining life of the market.

That setup creates higher upside when realized yield beats market expectations. If the asset produces more than the market had priced in through the implied yield, YT can become very attractive. For traders who want variable yield exposure rather than stability, this is where Pendle becomes more than a fixed-return protocol.

The trade-off is that YT carries much more sensitivity. If yields compress, if realized yield disappoints, or if the underlying asset loses traction, YT can underperform quickly. Time decay also matters here. As maturity approaches, the remaining yield window shrinks, making YT harder to justify unless the yield outlook remains unusually strong.

Why Pendle Needs a Specialized AMM

At this point, the obvious question is why Pendle cannot just use a standard AMM design and call it a day. The answer is that PT and YT are not ordinary tokens. They are tied to time-decaying assets, and their value changes as maturity approaches. That makes pricing more complicated than a normal spot market.

Pendle’s AMM is built for that exact problem. It is designed to handle assets whose relationship to time matters, so liquidity and pricing remain more efficient as the maturity date approaches. In simpler terms, the AMM is designed to make trading PT and YT workable without forcing users into a market structure built for static assets.

That matters for practical reasons, not just design elegance. Better pricing efficiency can reduce slippage, improve liquidity conditions, and help the market's implied APY reflect real expectations more closely. For a review, the key point is that Pendle’s AMM exists because ordinary DeFi market designs are not designed for yield claims that decay toward maturity.

With the mechanism laid out, the next question becomes more strategic. If Pendle can split yield and price maturity and create separate principal and yield markets, what problem is it actually solving for users in DeFi?

What Problem Does Pendle Solve?

Separating Yield From Principal To Unlock New Trading Opportunities

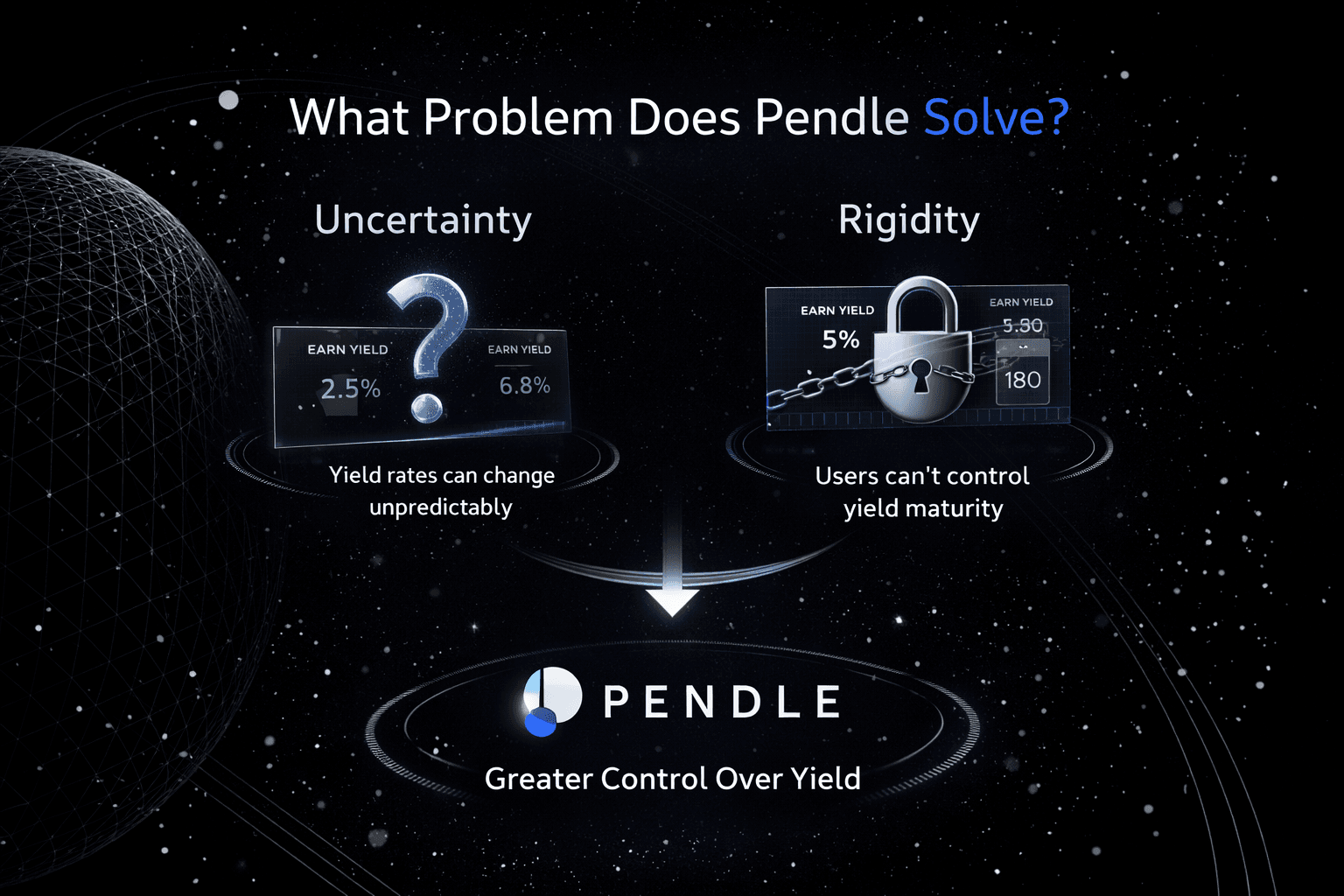

Separating Yield From Principal To Unlock New Trading OpportunitiesPendle matters because most DeFi yield products still force users into a passive role. You deposit a yield-bearing asset, watch the rate move around, and accept whatever outcome the market gives you. That works when yields are stable and expectations are low. It works far less well when rates swing sharply, incentives dry up, or users want more precision over how they earn.

Pendle steps into that gap by separating principal from future yield. That sounds technical at first, but the user benefit is simple. It gives people more control over uncertainty, liquidity, and portfolio construction. Instead of treating yield as one bundled stream, Pendle turns it into something users can shape, price, and trade.

That changes the experience meaningfully. The protocol is not just chasing higher APYs. It aims to address the fact that DeFi yield is often unpredictable, difficult to manage, and too rigid once capital is deployed.

Variable Yield Uncertainty

This is the clearest problem Pendle addresses. In traditional DeFi, yield is often unstable by design. Lending rates move with utilization, staking rewards change with participation, and incentive programs can inflate returns one month and disappear the next. For users, this creates a constant mismatch between expected and realized yields.

To compare major protocols like Aave, Curve, and Yearn in one place, see our DeFi yield farming platforms comparison guide

The issue is not only that returns fluctuate. The bigger problem is that users usually have no direct way to isolate or manage that fluctuation. If they want asset exposure, they often have to accept the associated yield uncertainty as well. If they want the yield, they remain exposed to whatever changes the protocol or market throws at them over time.

Pendle breaks that bundled structure apart. Through PT, users can move toward a fixed-yield style outcome by buying principal at a discount and holding to maturity. On YT, users can take the opposite side and speculate on future yields if they believe the market is underpricing them. This creates a real market for yield expectations rather than leaving users trapped in a passive-earn product.

That is a real upgrade in DeFi terms. Yield stops being an opaque output and becomes something the market can price in advance. For sophisticated users, that means clearer decisions. For example, they can choose predictability when market conditions look unstable, or they can lean into yield volatility when they see mispricing.

Capital Locked In Yield Positions

A second problem is that yield-bearing assets are often productive but not especially flexible. In many DeFi systems, once capital is placed into a vault, staking product, or reward-bearing wrapper, it becomes harder to separate what the user actually owns from what they are waiting to earn. The position may look liquid on paper, but in practice, the yield exposure stays bundled and awkward to manage.

That creates friction. A user may want to keep the principal exposure but exit the uncertain part of the trade. Or they may want direct exposure to future rewards without tying up as much capital in the full asset. Traditional yield products rarely make either choice easy.

Pendle improves this by making the future yield component tradable. Once a yield-bearing asset is tokenized into PT and YT, the user no longer needs to treat the entire position as a single block. They can sell the yield, keep the principal, buy only the yield, or rebalance depending on the market view. That makes capital more modular.

This matters for capital efficiency. In most DeFi protocols, yield is something you wait for. In Pendle, yield becomes an active part of the position that can be priced and traded separately. That gives users more ways to unlock value from the same underlying asset rather than simply parking it and hoping the return stays attractive.

There is another layer here, too. Locking capital in DeFi is not only about liquidity in the narrow sense. It is also about strategic flexibility. Pendle gives users more room to respond when rates change, sentiment shifts, or a better opportunity arises elsewhere. That optionality is one of the protocol’s strongest practical advantages.

Limited DeFi Risk Management Tools

This is where Pendle starts to look more mature than a standard yield platform. DeFi offers plenty of ways to earn. It offers far fewer tools for managing yield exposure with intent. Most users can choose where to deploy capital, but they have limited ways to separate interest rate views, hedge yield compression, or structure positions around time and maturity.

Pendle introduces a more flexible toolkit. PT gives users a cleaner path to defined returns, which can matter when variable yields look unreliable or when portfolio stability matters more than upside. YT, on the other hand, gives traders a direct way to express a view on future yield. If they believe the actual yield will come in above what the market currently implies, they can position around that view explicitly.

That creates something closer to a yield market than a yield farm. Instead of asking a vague question-"Which protocol pays the most right now?"-Pendle lets users ask more precise ones. Is the market overpricing future yield? Underpricing it? Would a fixed-yield style position be smarter here than chasing floating rewards? How much time to maturity is changing the trade's attractiveness?

This is one of Pendle’s strongest differentiators because it adds structure to a part of DeFi that is usually messy. It gives advanced users tools to hedge, speculate, rotate risk, and shape exposure with more accuracy. In a sector where yield products often blur everything together, that sharper separation is valuable.

At the same time, this is also where the protocol becomes harder for beginners. Better risk management tools only help if users understand what they are managing. So the feature is powerful, but it raises the learning curve, too. That tension sits at the heart of Pendle’s appeal. It solves more complex problems, but it expects a more sophisticated user in return.

Key Features Of Pendle Finance

Main Functionalities Driving Yield Trading And Protocol Efficiency

Main Functionalities Driving Yield Trading And Protocol EfficiencyOnce you move past the main mechanics, Pendle starts to look less like a niche yield experiment and more like a full product stack for yield management. Its best features are not random add-ons. They all revolve around the same central idea: giving users more control over how yield is priced, traded, and distributed across time. Pendle’s documentation frames the protocol around SY-based yield tokenization, PT and YT markets, a specialized AMM, and incentive systems tied to governance and liquidity.

What makes the feature set stand out is that each part solves a different user need. One feature helps fixed-yield seekers, another helps yield traders, another keeps time-decay markets functional, and another turns governance into an economic layer rather than a cosmetic token utility. That is why Pendle feels more complete than a simple “earn” interface.

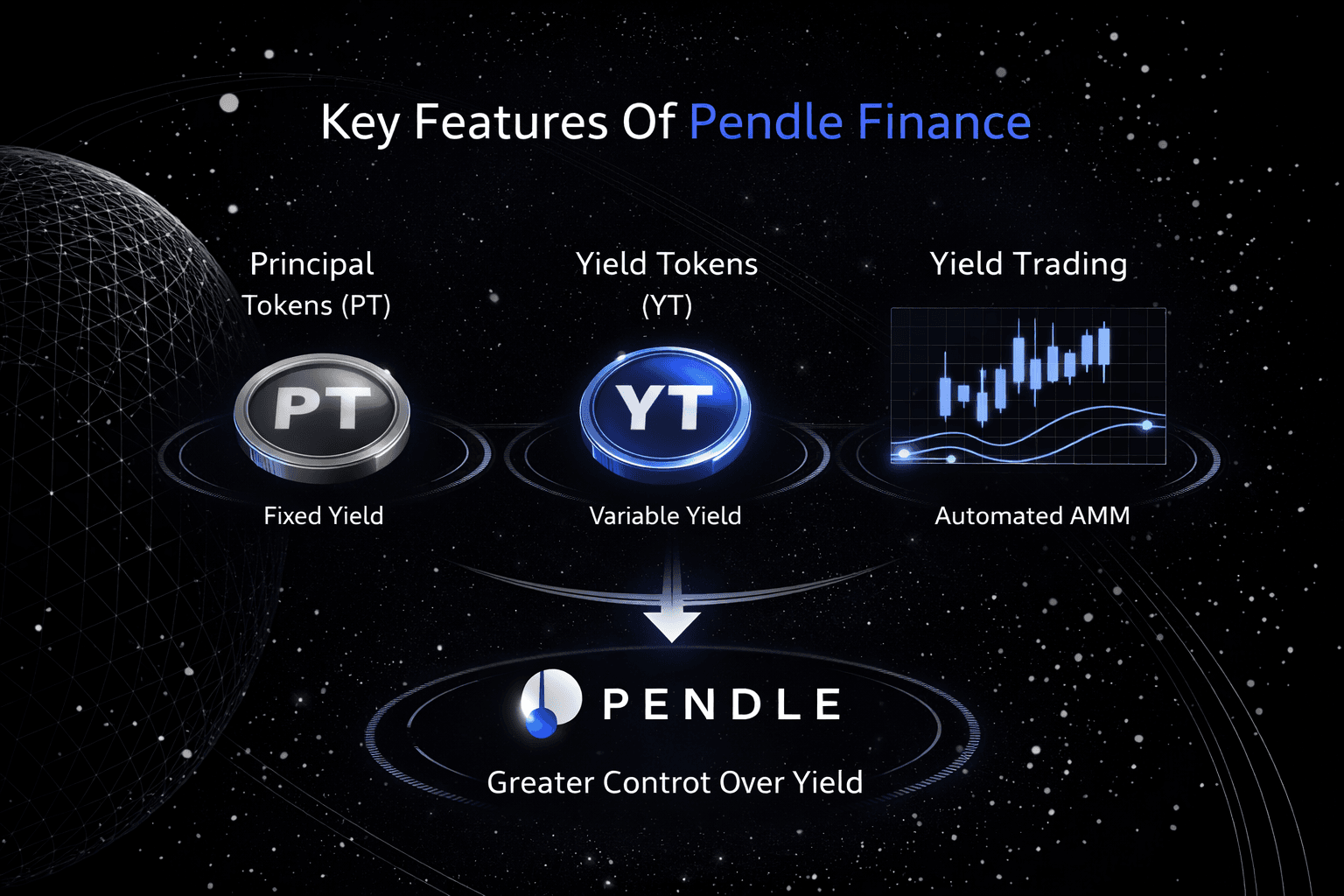

Fixed Yield Via PT

PT is one of Pendle’s most practical features because it gives DeFi users a way to access fixed-yield exposure without forcing them into a traditional lending product. PT typically trades below its redemption value before maturity, so users who buy PT and hold it until maturity can capture the discount as an implied yield. Pendle’s own glossary and tokenization docs position PT around that maturity-based redemption logic.

Why does that matter? Because many DeFi users are not trying to squeeze every last bit of upside from floating rewards. Many would rather know what kind of return profile they are targeting. PT helps that group by removing future yield volatility, leaving a cleaner principal claim. For users managing treasury assets, stablecoin strategies, or more conservative DeFi allocations, this is one of Pendle’s strongest product advantages.

This feature is especially relevant in markets built around liquid staking tokens, liquid restaking tokens, and stablecoin yield assets. Once those positions are tokenized, PT becomes a way to turn a variable-yield source into something closer to a defined-return position, which is a rare thing in DeFi.

Yield Trading Via YT

If PT is the stability side of Pendle, YT is the higher-conviction trading side. YT gives the holder exposure to future yield and associated rewards until maturity. That means traders can take an explicit view on whether realized yield will come in above or below what the market currently implies. Pendle treats YT fees as the main revenue source, which also shows how central yield trading is to the protocol’s design.

This matters because most DeFi protocols do not let users isolate yield expectations so directly. Usually, you either hold the full asset and accept whatever happens, or you leave. Pendle gives traders a sharper instrument. If they think a market tied to assets like USDe, stETH, or eETH is underpricing future rewards, YT is the tool for expressing that view. If they are wrong, YT can decay hard into maturity, which is exactly why this feature is both powerful and dangerous.

For the right user, though, this is the feature that makes Pendle feel unique. It turns yield from a passive byproduct into an actively tradeable thesis. That is a real jump from standard DeFi design.

Specialized AMM For Time-Decay Assets

Pendle’s AMM is not there for novelty. It exists because PT and YT are time-decaying assets, and standard AMM designs are not well-suited to instruments whose value changes as maturity approaches. Pendle’s docs explicitly frame swap fees and pricing around maturity-sensitive mechanics rather than ordinary spot-token behavior.

This is more important than it sounds. A protocol can invent clever tokens, but if trading them is clunky, illiquid, or too expensive, the product falls apart in practice. Pendle’s AMM is one of the reasons the broader design works. It helps the protocol handle pricing efficiency, slippage, and liquidity in markets where time itself changes the asset's economics.

For users, the benefit is straightforward. They get a market structure built for yield claims rather than one awkwardly borrowed from generic DeFi swaps. That helps Pendle feel more like purpose-built infrastructure than a patched-together experiment.

Multi-Chain Availability

Pendle is no longer just an Ethereum-only idea. Its official deployment documentation lists support across Ethereum, Optimism, BNB Chain, Sonic, HyperEVM, Mantle, Base, Arbitrum, and Berachain. That broad deployment matters because yield opportunities no longer live on a single chain, and users increasingly move between ecosystems to chase better assets, incentives, and liquidity.

In summary, this is a meaningful feature because it widens Pendle’s addressable market. A protocol that only works in one corner of DeFi is easier to dismiss as niche. Pendle’s cross-chain footprint gives it more relevance across liquid staking, liquid restaking, and stablecoin yield markets wherever those assets are gaining traction.

It also makes the dashboard and position-tracking layer more useful. Pendle’s dashboard is built to show balances, claimable yield, rewards, and historical performance across positions, which becomes far more valuable once users are active across multiple chains and markets.

vePENDLE Governance And Fee Incentives

This is where Pendle stops being just a trading venue and begins to look like an ecosystem. Historically, vePENDLE has been the protocol’s vote-escrow model for governance, fee sharing, and liquidity incentives. Holders lock PENDLE, receive vePENDLE, vote on incentive direction, receive base APY, share in fee-related rewards, and can boost LP rewards by up to 250%, according to Pendle’s documentation. Fees from YT and swap activity are also partially distributed to vePENDLE holders.

Why does that matter for users? Because it ties governance to actual economic outcomes. In weaker DeFi projects, governance is often decorative. Here, the vote-escrow layer influences where liquidity incentives go and who captures fee-related upside. That creates a tighter connection between trading activity, liquidity depth, and tokenholder participation.

There is one caveat about freshness worth being clear about. Pendle’s current docs label vePENDLE as legacy and state that sPENDLE is fully replacing it. So for a 2026 review, vePENDLE still matters as a central part of Pendle’s design history and incentive structure, but it should be described with that transition in mind rather than as an untouched, permanent end state.

Taken together, these features explain why Pendle still stands out in DeFi. Fixed yield via PT, directional yield trading through YT, an AMM built for maturity-based assets, multi-chain reach, and governance-linked fee incentives all serve the same broader purpose. They give users more control over yield than most protocols are willing, or able, to offer.

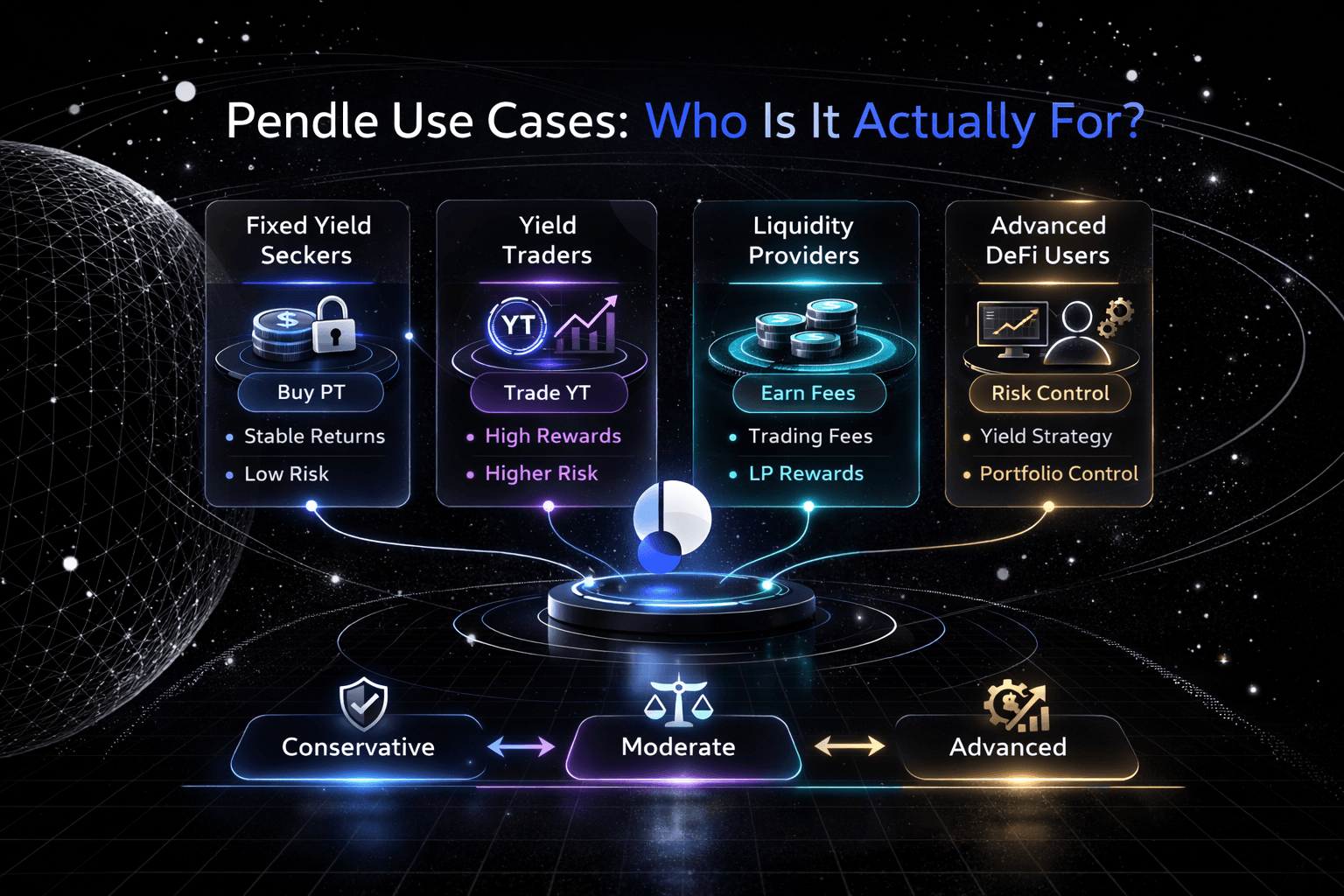

Pendle Use Cases: Who Is It Actually For?

Identifying Ideal Users Based On Yield Strategies And Risk Profiles

Identifying Ideal Users Based On Yield Strategies And Risk ProfilesPendle is one of those DeFi protocols where the fit matters almost as much as the feature set. On paper, it can serve several types of users. In practice, it works best for people who already know what kind of yield exposure they want and why. That is because Pendle does not just help users earn. It helps them choose between fixed yield, yield speculation, hedging, and capital flexibility with far more precision than a standard DeFi app.

That makes Pendle powerful, though not universally appealing. For the right user, it opens up strategies that are hard to replicate elsewhere. For the wrong one, it can feel like too much machinery for a simple yield goal.

Best for DeFi Users Seeking Fixed Yield

Pendle is a strong fit for DeFi users who want a clearer return profile rather than chasing a variable-yield curve. In most protocols, users deposit a yield-bearing asset and accept whatever rate the market produces over time. Pendle gives them another route. By buying PT, users can lock into a known return profile based on the discount to maturity rather than remaining exposed to the full uncertainty of future rewards.

This matters for users who care more about predictability than upside. A PT position can feel more structured than a typical DeFi earn strategy because the user knows what they are targeting if the token is held to maturity. That makes Pendle especially relevant for stablecoin-focused users, on-chain treasury managers, and advanced investors who want fixed-yield exposure within DeFi without leaving the ecosystem entirely.

There is also a psychological advantage here. Variable yields can make portfolio planning messy, especially when returns fluctuate quickly. PT gives users a way to reduce that noise and anchor part of their portfolio to a more defined outcome.

Best for Traders Speculating on Yield Changes

Pendle is also built for a very different kind of user: traders who want to take a directional view on future yield. This is where YT becomes the main tool. Instead of buying a bundled yield-bearing asset and passively waiting for outcomes, a trader can buy YT to gain direct exposure to future yield until maturity.

That creates a cleaner expression of a market view. If a trader believes realized yield will come in above what the market currently implies, YT gives them a way to position around that belief. In other words, Pendle does not just let users earn yield. It lets them speculate on how yield itself will evolve.

This is one of the most unusual aspects of the protocol and one of the main reasons advanced users pay attention to it. Very few DeFi products isolate yield expectations this directly. Of course, the trade cuts both ways. If yields compress, market expectations cool, or the underlying asset underperforms, YT can lose value quickly. This use case makes Pendle exciting, though it also makes it less forgiving.

Best for Yield Farmers Seeking Capital Flexibility

Pendle also works well for users who want greater flexibility with assets that would otherwise remain bundled in a single yield position. In ordinary DeFi setups, principal and future income tend to travel together. Once funds are placed in a yield-bearing asset, the user often has limited control over which portion of the exposure they want to keep and which portion they want to exit.

Pendle improves that by separating principal from future income. That means a user can hold PT for the principal side, trade YT for the future yield side, or rebalance between them depending on market conditions. For yield farmers, this adds a layer of capital efficiency that many DeFi protocols still lack.

This matters because flexibility is not just about exiting a position. It is about shaping it. A yield farmer may want to keep principal exposure while monetizing future income today. Another may want direct exposure to future rewards without tying up as much capital in the full asset. Pendle supports that kind of portfolio design, which is why it appeals to users who actively consider liquidity, hedging, and yield exposure rather than simply chasing the highest headline APY.

Best for Advanced Users, Not Complete Beginners

This is the section where the review has to be blunt. Pendle is better suited to advanced DeFi users than to complete beginners. The interface itself is not the main issue. The harder part is understanding what the positions actually mean. Users need to understand maturity mechanics, pricing complexity, implied yield, time decay, and that smart contract risk never disappears just because a protocol is well-known.

That learning curve matters. PT and YT are conceptually elegant, but they are not beginner-simple. A new user who only wants passive yield may find Pendle far more complicated than a standard lending market or staking interface. The risk is not that the protocol is broken. The risk is that the user enters positions without fully understanding maturity risk, yield speculation, or how pricing changes as expiry approaches.

For experienced DeFi users, this complexity is often the attraction. It creates more strategy room, more tools, and more control. For beginners, it can become frustrating very quickly. Pendle is not impossible to learn, but it is rarely the first protocol I would point to for someone who just wants an easy place to park assets.

- Pendle Is A Better Fit If You…

Want fixed yield exposure, want to trade future yield, care about hedging yield changes, or actively manage DeFi positions across maturity dates and market conditions. - Pendle Is Probably Not For You If You…

Want simple passive income, dislike pricing complexity, do not want to track maturity risk, or prefer a more straightforward DeFi app like a basic lending market.

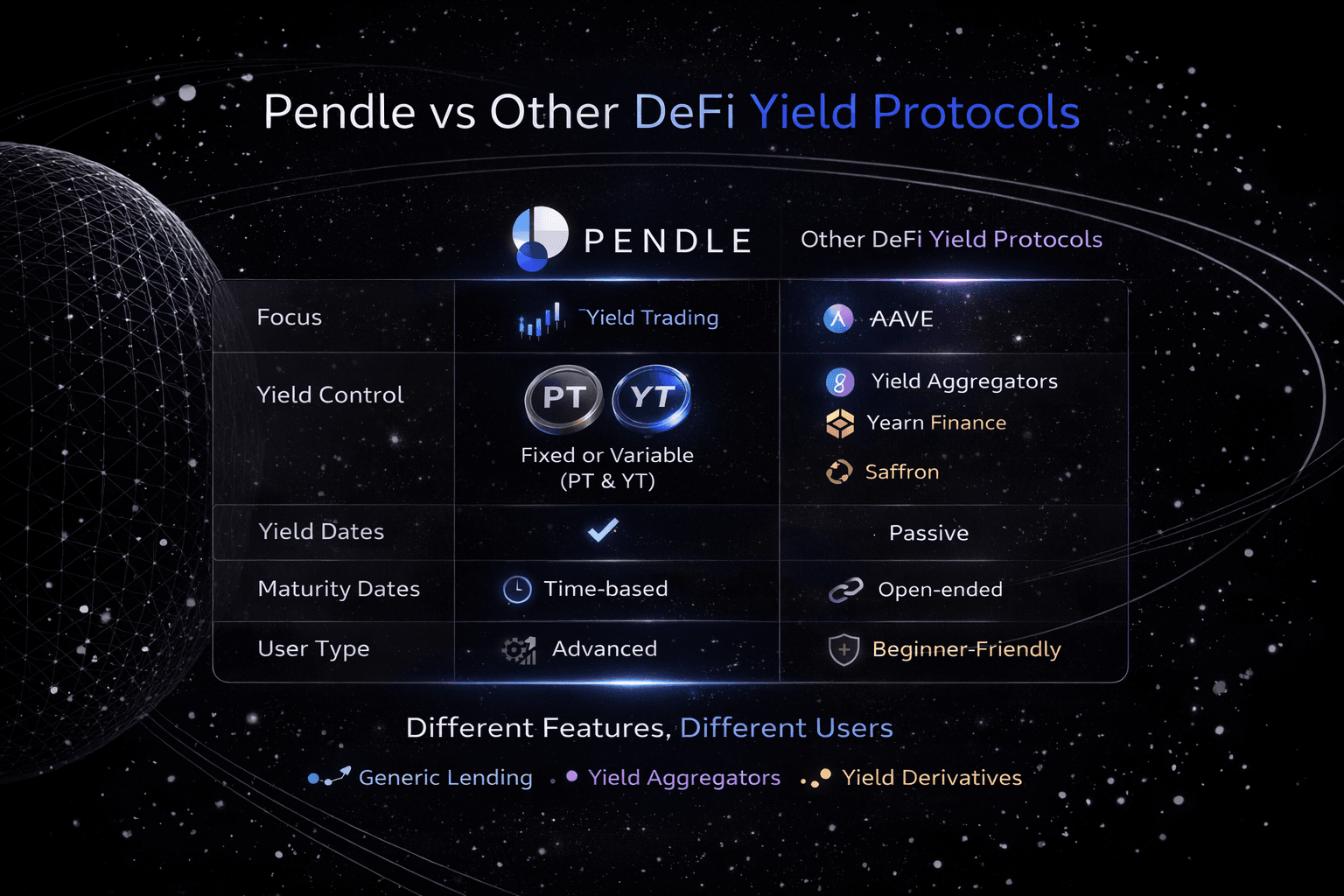

Pendle vs Other DeFi Yield Protocols

Comparing Pendle With Leading Yield Protocols Across DeFi Ecosystem

Comparing Pendle With Leading Yield Protocols Across DeFi EcosystemPendle sits in a more specialized corner of DeFi than most yield protocols. Aave is easier and built around variable yield lending markets. Notional is more direct for fixed-rate borrowing and lending. Element Finance is the closest historical comparator because it also focused on fixed yield design. Pendle stands apart because it combines yield tokenization, a tradable yield component through YT, and a maturity-aware AMM in one system.

Pendle vs Element Finance vs Notional vs Aave

| Protocol | Primary Focus | Fixed Rate Support | Yield Tokenization | Tradable Yield Component | AMM / Market Structure | Best For | Main Limitation |

|---|---|---|---|---|---|---|---|

| Pendle | Tokenized yield and active yield strategies | Yes, via PT discount to maturity | Yes | Yes, via YT | Specialized AMM for maturity-based assets | Advanced DeFi users who want fixed yield, yield trading, and maturity-based positioning | More complex than mainstream DeFi apps |

| Element Finance | Historical fixed-yield DeFi design | Yes | Yes | Yes | Fixed-term yield market design | Users comparing older tokenized-yield models | Smaller current relevance than Pendle |

| Notional | Fixed-rate borrowing and lending | Yes | No | No separate tradable yield token | Native fixed-term market structure | Users who want more direct fixed-rate borrowing or lending | Narrower strategy range for active yield trading |

| Aave | Variable yield lending and borrowing | Limited, not core | No | No | Standard money market/liquidity pool model | Mainstream DeFi users who want a simpler product | No yield tokenization or separate future-yield exposure |

Pendle is better suited when the goal is active yield management, fixed-yield positioning, or trading future yield through a dedicated yield tokenization framework. It is not better when the goal is simplicity. In that case, Aave is easier for mainstream DeFi users, while Notional is cleaner for users who just want fixed-rate borrowing or lending without Pendle’s added complexity.

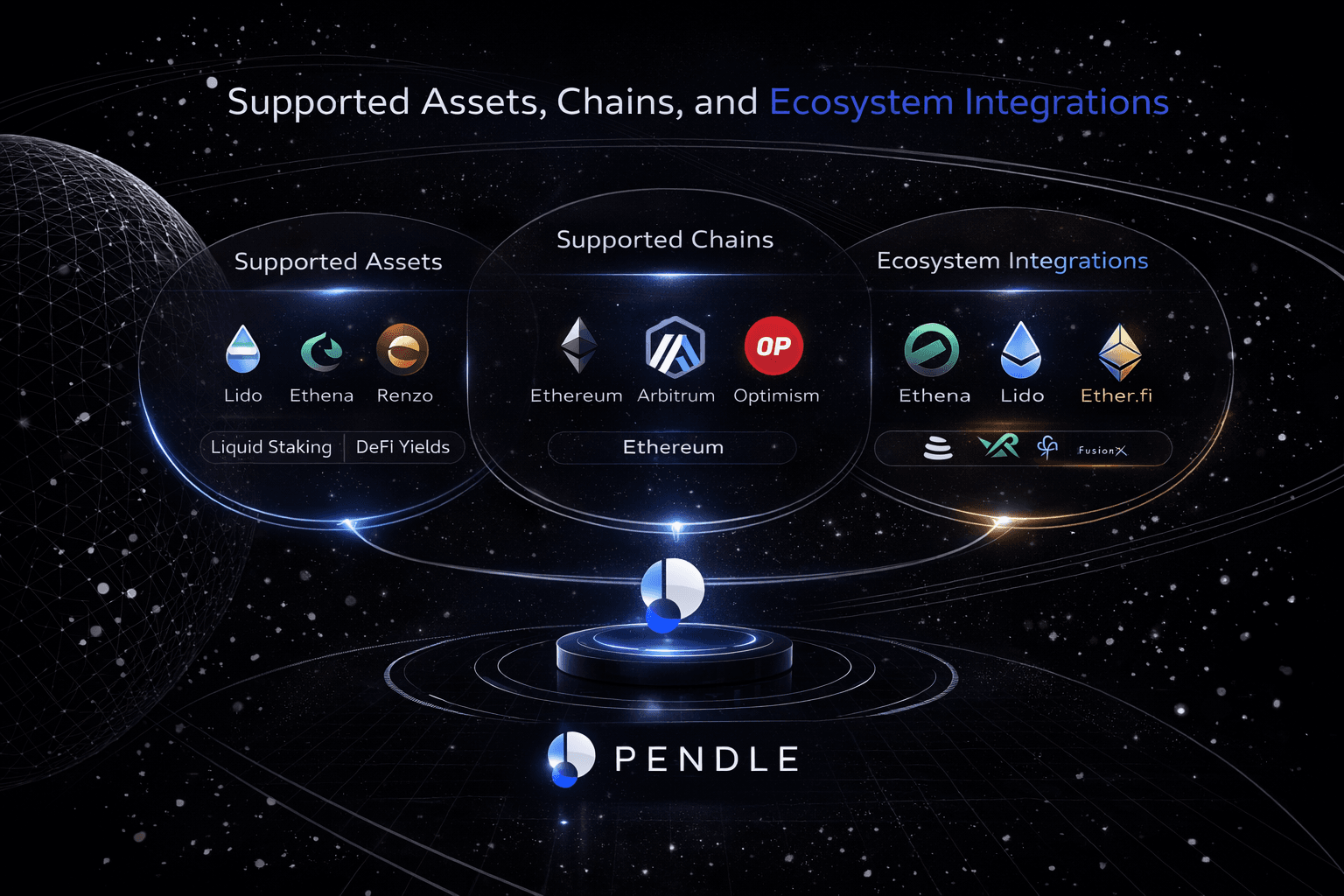

Supported Assets, Chains, and Ecosystem Integrations

Assets Chains And Integrations Powering Pendle’s Expanding Ecosystem

Assets Chains And Integrations Powering Pendle’s Expanding EcosystemThis section needs to stay controlled because Pendle’s live markets change over time. The useful way to frame it is by focusing on supported chains, the main asset categories Pendle keeps attracting, and the ecosystem names that signal where its relevance actually comes from. Pendle’s own deployment docs show that the protocol is live across Ethereum, Optimism, BNB Chain, Sonic, HyperEVM, Mantle, Base, Arbitrum, and Berachain.

Supported Chains

Pendle is no longer tied to one chain or one narrow yield niche. Its official deployment documentation lists Ethereum-

Optimism, BNB Chain, Sonic, HyperEVM, Mantle, Base, Arbitrum, and Berachain are supported chains. For this review, the main chains worth emphasizing are Ethereum, Arbitrum, Optimism, and BNB Chain because they are the easiest for most DeFi users to recognize, and they carry much of the protocol’s practical relevance.

That multi-chain presence matters for two reasons. First, yield opportunities in DeFi are fragmented, so a protocol limited to one ecosystem will naturally feel narrower. Second, Pendle’s appeal depends on having enough variety in assets and enough liquidity across markets for PT and YT strategies to stay useful. A wider chain footprint helps support both.

Common Asset Categories on Pendle

Pendle works with yield-bearing assets, but the article should stay at the category level rather than turning into a giant pool list. The main buckets to highlight are liquid staking tokens, liquid restaking tokens, stablecoin yield assets, and money market positions. Pendle’s own docs use examples like stETH and cDAI to explain how yield-bearing tokens are wrapped into SY before PT and YT are created.

That framing is useful because it shows the protocol’s breadth without pretending every pool matters equally. In practice, Pendle’s ecosystem relevance has been strongest where yield is already meaningful: LSTs, LRTs, and synthetic or stablecoin-linked yield products. That is why names like stETH, eETH, and USDe keep surfacing around the protocol. Pendle is most interesting when it sits on top of assets that already have credible yield sources and meaningful TVL.

Important Integrations in Pendle’s Ecosystem

The clearest relevance signals in Pendle’s ecosystem come from recognizable DeFi names. Lido matters through stETH. Ethena matters through USDe and related stablecoin yield markets. Ether.fi matters through eETH. Morpho matters because Pendle PT and LP positions have increasingly shown up in collateral and capital-efficiency workflows around lending markets. Pendle’s own docs explicitly use stETH as an example for yield tokenization, and external ecosystem updates show PT and LP collateral activity expanding on Morpho.

EigenLayer adjacency is also worth mentioning carefully. Pendle has benefited from the broader rise of liquid restaking tokens and restaking-linked yield markets, even when the direct integration story depends on the specific asset and market. That is the right level of precision here. This is a review section, not a live pool screener.

The broad takeaway is straightforward. Pendle’s ecosystem matters because it sits at the intersection of major DeFi yield sources, not because it invented those underlying assets itself. It plugs into where LST, LRT, and stablecoin yield demand already exists, then adds yield tokenization on top.

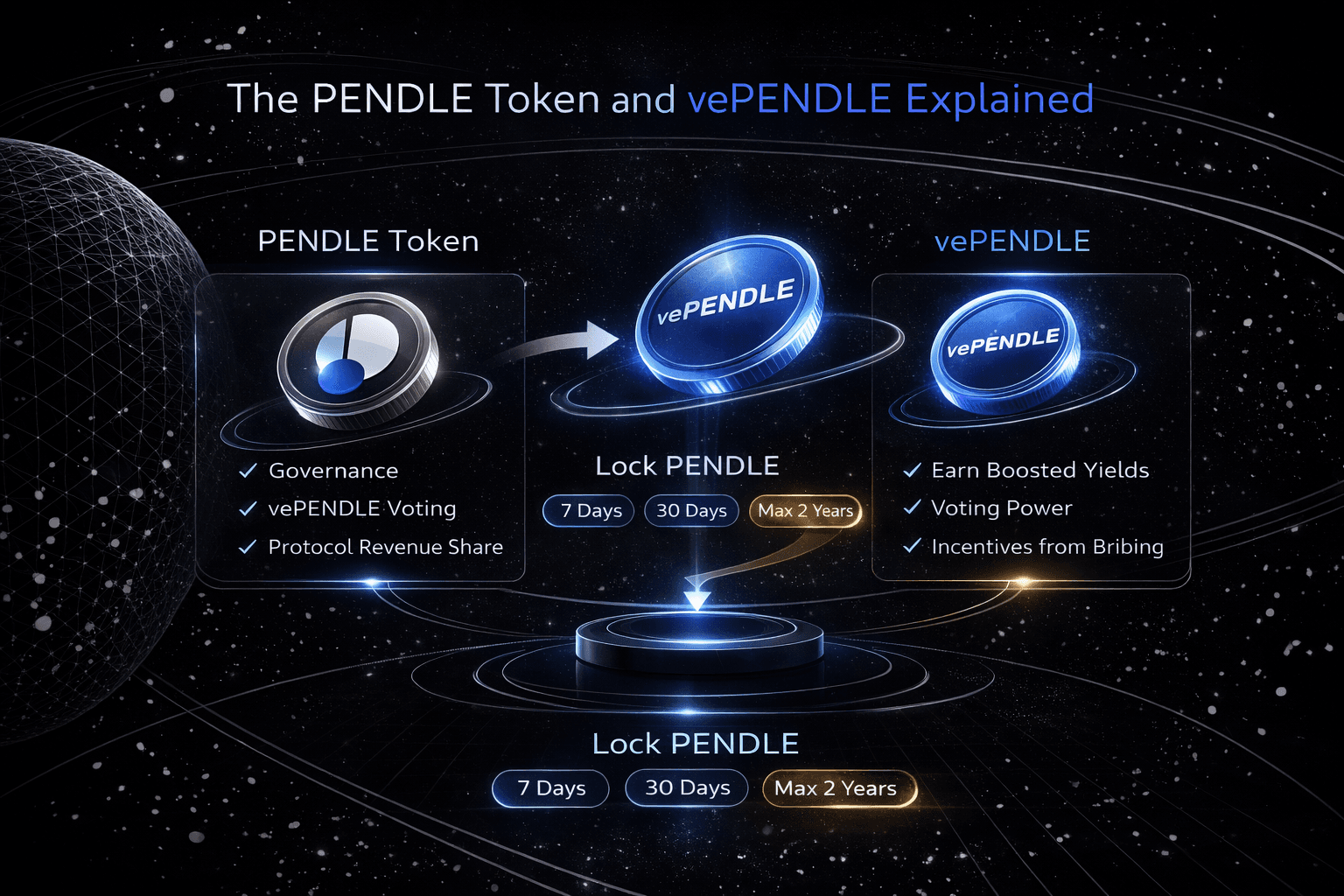

The PENDLE Token and vePENDLE Explained

Utility Governance And Incentives Behind PENDLE And vePENDLE Tokens

Utility Governance And Incentives Behind PENDLE And vePENDLE TokensThis section matters more than it looks. A lot of Pendle content explains PT, YT, and yield tokenization well enough, then rushes through the token layer as if it were just another governance coin. That would be a mistake here. The PENDLE token sits at the center of Pendle’s governance, incentives, and protocol participation. vePENDLE, in turn, was the vote-escrow layer that tied long-term token holders to fee sharing, emissions, and liquidity incentives. In 2026, there is one update you have to keep straight from the start: Pendle’s docs now label vePENDLE as legacy and say sPENDLE is fully replacing it. So when you explain vePENDLE today, the right framing is historical and structural, not “this is the untouched current system.”

That said, vePENDLE still deserves a full explanation because a huge part of Pendle’s reputation, tokenomics, and ecosystem incentives was built around it. Users still encounter the term constantly in older guides, forum posts, analytics dashboards, and “Pendle Wars” discussions. More to the point, you cannot really understand why PENDLE has had durable utility unless you understand what the vote-escrow system was designed to do: lock tokens, reduce floating supply, direct emissions, capture fees, and align governance power with long-term commitment.

What the PENDLE Token Does

At the most basic level, the PENDLE token is the protocol’s native token. But that bare description does not tell you much. Its real function is to coordinate the economic side of the Pendle ecosystem: governance, ecosystem incentives, protocol participation, and the broader tokenomics that keep liquidity and activity flowing through Pendle markets.

Start with governance. Pendle is not just an app for trading PT and YT. It is a protocol whose incentive design has to decide where emissions go, how fee capture works, and how long-term participants are rewarded. The PENDLE token is the asset that gives users a stake in that process. Historically, that governance power was not exercised by simply holding liquid PENDLE in a wallet. It became meaningful when users locked PENDLE into the vote-escrow system to receive vePENDLE. That distinction matters. A liquid token can be traded. A vote-escrow token is meant to signal commitment.

Then there are ecosystem incentives. Pendle’s tokenomics page says that, as of September 2024, all team and investor tokens had fully vested, and any increase to circulating supply would come from incentives and ecosystem building. The same page says weekly emissions were 216,076 PENDLE as of September 2024, decreasing by 1.1% each week until April 2026, after which the system moves to a terminal inflation rate of 2% per year for incentives. That is a very important point for readers because it shows PENDLE is not a dead utility token sitting passively beside the protocol. It is part of an ongoing emissions system used to support activity and liquidity.

That brings us to protocol participation. PENDLE is not only about abstract governance rights. It has historically been the token users' key to participate more deeply in the protocol’s incentive layer. If a user wanted stronger alignment with fee capture, voting power, and boosted LP rewards, the token mattered. This is why PENDLE carried more functional depth than many DeFi governance tokens, which often grant nominal voting rights but little economic relevance. On Pendle, the token linked users to real protocol mechanics, especially through the vote-escrow model.

There is also a supply-side angle worth making explicit. Pendle’s docs state that circulating supply excludes PENDLE staked in the sPENDLE contract, PENDLE in the vePENDLE contract while it winds down, and tokens sitting in ecosystem, governance, and team-controlled addresses. That means token locking has not been cosmetic. It has directly affected how much PENDLE is actually floating in the market at a given time. In any discussion of tokenomics, that is crucial because emissions matter, but so does how much supply is effectively taken off the market by staking and lockups.

So what does the PENDLE token actually do in plain English? It gives the protocol a way to reward participation, distribute influence, and shape liquidity. In earlier phases of Pendle’s design, it also served as the raw input for vePENDLE, where most of the richer utility appeared. That is why it is not enough to say “PENDLE is the governance token.” A better way to say it is: PENDLE is the token that integrates Pendle’s governance, emissions, liquidity incentives, and long-term alignment into one economic system.

What vePENDLE Is

vePENDLE stands for vote-escrowed PENDLE. Historically, users got vePENDLE by locking PENDLE for a chosen duration. Pendle’s documentation says vePENDLE value was proportional to both the amount locked and the duration locked, up to a maximum of 2 years. It also says each wallet had a single vePENDLE expiry date, and the vePENDLE balance decayed over time, eventually reaching zero when the lock expired and the underlying PENDLE unlocked.

This is where the vote-escrow model becomes important. In a normal token system, your power is mostly linear and static: hold tokens, keep voting power. In a vote-escrow system, your power depends on how much you are willing to lock and for how long. That changes behavior. It rewards users who commit capital for longer periods instead of those who simply swing in and out of the token. Pendle used that structure to build a more durable governance and incentive mechanism.

The easiest way to understand vePENDLE is to break its role into four parts: voting power, fee sharing, emissions direction, and liquidity incentives.

First, voting power. vePENDLE holders could vote to channel PENDLE incentives into specific pools. Pendle’s docs describe this as the incentive channeling mechanism. Votes were taken at the start of each epoch, and the reward rates for the pools were adjusted accordingly. In simple terms, vePENDLE holders decided where emissions flowed. That gave the token real governance utility, because it did not just affect an abstract proposal process. It affected where the protocol actually sent incentives.

Second, fee sharing. vePENDLE holders were entitled to a share of protocol-generated value. Pendle’s docs state that voting for a pool entitled vePENDLE holders to 80% of the swap fees collected by that pool, distributed pro rata among all voters for that pool. The docs also say the protocol collected a 5% fee on all YT yield, including points, and that a portion of the yield from matured unredeemed PTs was distributed to vePENDLE holders. Those rewards were converted to USDT and distributed periodically. So fee sharing on Pendle was not a vague promise. It was wired directly into how the protocol routed revenue.

Third, emissions. vePENDLE holders did not just earn from fees. They also influenced emissions, meaning the protocol’s ongoing PENDLE incentive distribution across pools. This is a big deal in DeFi because emissions shape liquidity. If a pool receives more emissions, it becomes more attractive to liquidity providers. If it receives less, liquidity may migrate elsewhere. By giving vePENDLE holders control over emissions direction, Pendle turned governance into a market force rather than a symbolic feature.

Fourth, liquidity incentives. Pendle’s docs state that vePENDLE holders could boost LP rewards by up to 250%. The boost depended on vePENDLE value and the user’s relative ownership share. This turned vePENDLE into more than a governance receipt. It became a way for committed users to deepen their participation and amplify rewards on the liquidity side of the protocol.

There is also a subtle but important tokenomics role here. Pendle’s docs say vePENDLE served as an additional sink for reducing the liquid supply of PENDLE. That matters because token models are not only about what the token can do. They are about what incentives exist to hold, stake, or lock it rather than sell it. vePENDLE improved PENDLE’s utility by giving users reasons to lock it, while also reducing immediately circulating supply. That creates a tighter relationship between governance commitment and market structure.

Now for the 2026 reality check. The current documentation explicitly states that vePENDLE is legacy and being replaced by sPENDLE. The docs say the final vePENDLE vote was scheduled for January 21 and that vePENDLE renewal ceased on January 29, with a transition and loyalty bonus mechanism tied to the move toward sPENDLE. The newer sPENDLE docs describe a staking model in which PENDLE is staked 1:1 into sPENDLE, with protocol revenue distributed to active sPENDLE holders, and a 14-day exit period or immediate unstaking with a fee.

So, when explaining vePENDLE in 2026, the accurate phrasing is: vePENDLE was Pendle’s vote-escrow governance and fee-sharing layer, built around locking PENDLE for voting power, emissions control, and liquidity incentives; it is now a legacy mechanism being phased out in favor of sPENDLE.

Why vePENDLE Matters to Long-Term Users

Even as a legacy system, vePENDLE matters because it shows how Pendle became more than just a trading venue. Many DeFi protocols let users trade, farm, and withdraw. Pendle’s vote-escrow model sought to solve a harder problem: how to align governance, liquidity, fee capture, and long-term token holding so that the protocol is not driven solely by short-term mercenary capital? vePENDLE was Pendle’s answer to that.

That alignment worked in a few layers at once. Users who locked PENDLE got a say in where incentives flowed. Pools with real activity and fee generation became more attractive in the vote market. vePENDLE holders captured part of the value generated by swap and YT fees. Liquidity providers could boost rewards by participating more deeply in the governance layer. In other words, the system connected long-term holding to actual economic advantage instead of relying on loyalty as a vague virtue.

This is why Pendle developed a reputation for having stronger token utility than many DeFi peers. The token was not just there to farm and dump. It had a defined role in emissions, fee sharing, and liquidity incentives. That does not mean the design was simple. It was not. But it did mean the protocol had a more coherent economic loop than a lot of governance-token-first DeFi projects.

Long-term users should also understand why the transition away from vePENDLE is noteworthy. Pendle is not abandoning governance or tokenholder economics. It is changing the mechanism. The sPENDLE docs suggest the protocol is moving toward a simpler staking-and-participation model, where protocol fee flows are used for buybacks and distributions to active stakers. That is a different architecture from classic vote-escrow. So vePENDLE still matters because it explains how Pendle’s original tokenomics worked and why the protocol took governance and emissions seriously from the start.

For a reader trying to understand the token layer in one clean takeaway, here it is:

- PENDLE token is the native token that powers governance, incentives, and protocol participation.

- vePENDLE was the vote-escrow version created by locking PENDLE.

- vePENDLE gave users voting power, fee sharing, influence over emissions, and access to stronger liquidity incentives.

- This made Pendle more than a place to trade PT and YT. It turned the protocol into an ecosystem where long-term holders could shape liquidity and capture part of the value created.

- In 2026, vePENDLE is a legacy system being replaced by sPENDLE, so any accurate explanation must clearly mention the transition.

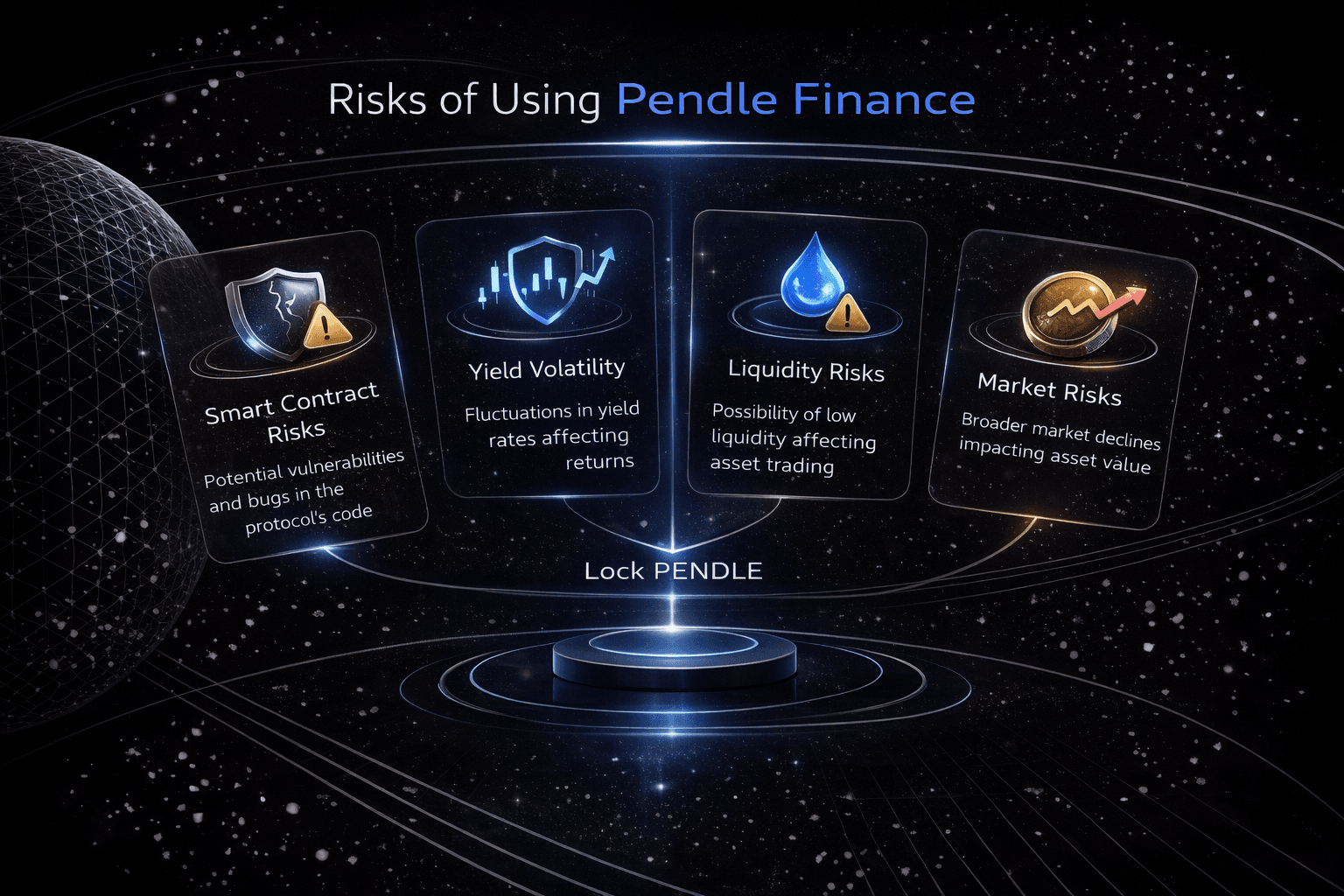

Risks of Using Pendle Finance

Key Risks Linked To Yield Trading And Market Volatility Exposure

Key Risks Linked To Yield Trading And Market Volatility ExposurePendle is one of the more sophisticated yield protocols in DeFi, and that sophistication is a double-edged sword. The upside is flexibility. The downside is that risk does not come from one place alone. It comes from Pendle’s own smart contracts, the underlying yield-bearing assets plugged into the protocol, the pricing of PT and YT before maturity, the liquidity available when you want to exit, and plain old user error. Pendle’s own FAQ answers by saying the protocol is audited, but it also warns that users should still exercise caution and deploy funds prudently. It also states clearly that Pendle interacts with third-party protocols and contracts, so users inherit risk from those systems too.

That is why “Pendle risk” should never be treated like one generic label. PT buyers, YT buyers, and LPs are all exposed to different things. A PT position can look conservative relative to YT, but it is not free of downside. A YT position can offer sharp upside, but it is highly sensitive to time decay and yield expectations. LP positions can earn fees and incentives, but they bring their own liquidity and pricing risks. To use Pendle properly, you have to understand which risk bucket you are actually stepping into.

Smart Contract Risk

The first layer is the familiar DeFi one: smart contract risk. Pendle’s security page says its smart contracts have been audited by Ackee, Dedaub, Dingbats, and Code4rena wardens, and that the contracts are open source. That is a solid trust signal. It reduces blind-protocol risk. It does not remove it. Pendle still tells users to be cautious, and the Terms make clear that the protocol is self-directed and non-custodial, which means users bear the consequences of using it.

There is another catch here. Pendle sits on top of non-Pendle underlying protocols and yield-bearing assets issued elsewhere. Its Terms explicitly say those assets and blockchains are not issued, operated, or controlled by Pendle. So even if Pendle’s own contracts work as intended, users can still be hit if the upstream asset, wrapper, or connected protocol fails. That matters a lot in practice because Pendle often interfaces with exactly the kinds of DeFi assets that carry their own operational, oracle, or redemption risk.

Underlying Asset and Third-Party Protocol Risk

This is one of the biggest things newcomers miss. Pendle does not create yield out of nowhere. It restructures the yield that comes from somewhere else. So the quality of a Pendle market depends heavily on the quality of the underlying yield-bearing asset.

If that underlying asset depegs, faces a negative yield, suffers an exploit, or simply performs worse than expected, Pendle users feel the impact. Pendle says this plainly: the protocol carries inherent risk because it interacts with third-party systems, and Pendle is not responsible for funds lost due to exploits in third-party contracts. That is not legal fluff. It is one of the most useful warnings in the whole documentation set.

This is why users cannot evaluate Pendle markets by APY alone. They also need to ask where the yield is coming from, how that asset behaves in stress conditions, and whether the broader protocol stack behind it is actually trustworthy.

Yield Compression and Market Risk

Pendle lets users trade future yield, which means users are exposed not only to asset risk, but also to expectation risk. If the market is pricing future yield too optimistically and actual yield comes in lower, positions can underperform even without a hack or systemic event.

This shows up differently across Pendle’s products. PT is often treated as the steadier side because it converges toward redemption at maturity. That is broadly true, but only within normal conditions. Pendle’s Negative Yield documentation makes this much clearer than most summaries do. It explains that if an interest-bearing token’s exchange rate falls below the watermark rate, PT can redeem below its expected value at maturity, leading to losses. The same document says YT will stop earning yield until the exchange rate recovers to the watermark rate.

That means even PT is not a pure bond substitute. It is safer-looking, not riskless. And YT is much more fragile because its entire value depends on future yield actually showing up before maturity. Pendle also notes in its FAQ that YT has no value after maturity; that is not a side detail, but the core of the trade. If you buy expensive yield and the underlying underdelivers, time works against you.

Liquidity and Exit Risk

Pendle’s model only works well when PT, YT, and LP positions can be entered and exited efficiently. That brings us to liquidity risk. A Pendle position may look attractive on entry, but if liquidity is thin or market conditions worsen, getting out can become much harder or much more expensive than expected.

Pendle’s PT collateral documentation discusses “insufficient PT liquidity for liquidation in a short duration” and warns that if the PT price drops significantly and does not recover, there may not be enough liquidity to liquidate PT collateral quickly, which can lead to bad debt in downstream money market settings. The LP collateral documentation makes the same point for LP tokens, noting “insufficient LP liquidity for liquidation in a short duration.”

For regular users, the practical translation is simple: do not assume displayed pricing equals guaranteed exit quality. PT can feel predictable if held to maturity, but it may be much less neat if you need to exit early. YT can be even tougher because it is more sensitive, more time-dependent, and more likely to deteriorate as maturity approaches. Liquidity is part of the strategy on Pendle, not an afterthought.

Maturity and Time-Decay Risk

Pendle’s entire design revolves around maturity, and that creates a risk profile many DeFi users are not used to. Pendle claims says each PT and YT has a maturity date. After that date, PT can be redeemed for the full underlying yield-bearing token, while YT only accrues yield until maturity and has no value after that point.

This matters because time is not neutral on Pendle. Time helps PT converge toward redemption. Time hurts YT because the remaining future yield window keeps shrinking. That makes timing crucial. A user can be directionally right about a market and still lose money if they enter too late, pay too much for future yield, or fail to understand how fast value can compress as maturity gets closer.

This is one reason Pendle is not beginner-friendly. The protocol does not just ask whether you think a yield source is good. It asks whether you understand how that yield is being priced over time.

Strategy Complexity and User Error

This is probably the most common risk in practice. Not the dramatic one, just the one people keep stepping on. Pendle’s tools are conceptually elegant, but they are not simple. PT, YT, implied yield, maturity, watermark rate, negative yield behavior, and liquidity conditions all matter. A user can lose money without any exploit happening simply because they misunderstood what they bought.

PT can be misread as “safe fixed yield” when it is really “more predictable under normal conditions.” YT can be misread as a high-upside yield bet without enough appreciation for time decay. LP positions can be misread through headline incentives while ignoring liquidity and exit conditions. Pendle is the kind of protocol where a clean interface can fool users into thinking the mechanics underneath are simpler than they are.

That does not make Pendle flawed. It just means the protocol rewards understanding and punishes casual clicking.

Regulatory and Infrastructure Risk

Pendle’s Terms were last revised on 9 December 2025 and make clear that the protocol is a self-directed, non-custodial infrastructure. The Terms also emphasize that Pendle relies on other blockchains, protocols, and externally issued yield-bearing assets. That means users are also exposed to broader infrastructure risk, including wallet issues, chain congestion, oracle dependencies, and regulatory pressure that may affect access or usability around the protocol stack.

This is the broadest risk category, but it still matters. DeFi protocols do not exist in isolation. Even if Pendle itself works fine, problems in the wider environment can still hit the user.

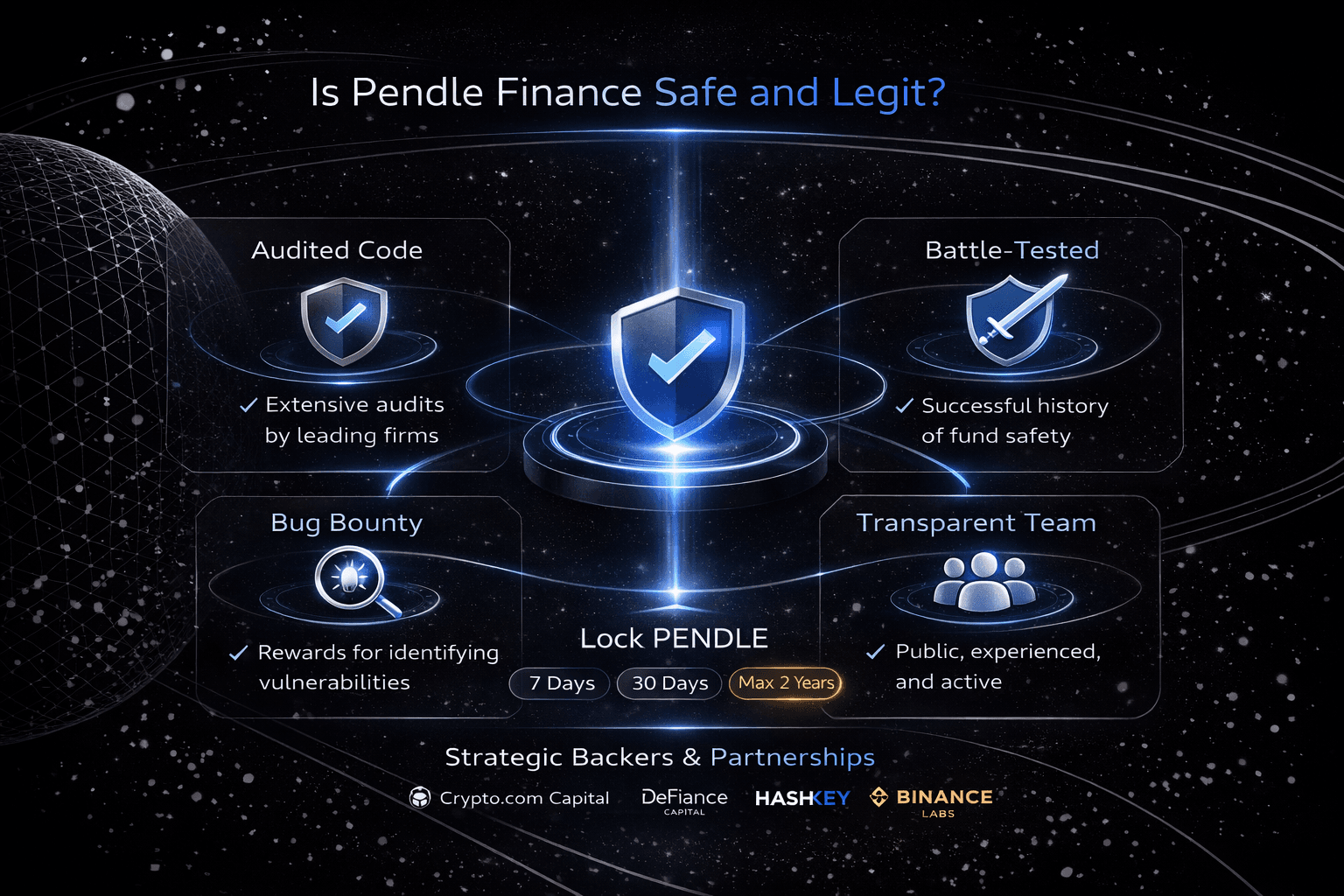

Is Pendle Finance Safe and Legit?

Security Model Trust Assumptions And Legitimacy Of Pendle Finance

Security Model Trust Assumptions And Legitimacy Of Pendle FinancePendle Finance is a legitimate DeFi protocol, but it is not risk-free. The legitimacy case is strong: Pendle has public documentation, open-source smart contracts, external audits, and a large on-chain footprint. Pendle’s security page says its smart contracts have been audited by wardens from Ackee, Dedaub, Dingbats, and Code4rena. DefiLlama also lists Pendle as audited and shows it with multi-chain TVL, active fees, and ongoing usage across the protocol.

That said, “safe” needs to be framed properly in DeFi. Pendle can be legitimate yet still carry real smart contract, liquidity, and underlying asset risks. A PT position may look steadier than YT, but neither exists in a vacuum. Pendle sits on top of yield-bearing assets and broader DeFi infrastructure, so users are also exposed to the quality of the underlying assets they choose and the systems those assets depend on. What this really means is simple: Pendle is credible, established, and widely used, but it still demands caution and understanding from the user.

A current trust signal worth mentioning is scale. DefiLlama’s Pendle page shows the protocol live across multiple chains and records large TVL, fee generation, revenue, and DEX volume. Those are useful signs of protocol legitimacy because empty or short-lived DeFi projects usually do not sustain such activity. Still, TVL is a confidence signal, not a guarantee of safety. A large protocol can still face losses if an underlying asset breaks, yields compress sharply, or a connected protocol fails.

So the clean answer is this: Pendle Finance is legit, audited, and relevant in DeFi, but it is not “safe” in the casual retail sense of the word. It is better described as a serious protocol for users who understand smart contracts, the quality of the underlying asset, and that DeFi risk never fully disappears.

Final Verdict: Is Pendle Finance Worth It in 2026?

Pendle Finance is one of the more genuinely original DeFi protocols still earning its place. It excels at turning yield into something users can actually manage instead of just passively receiving. For advanced users, that matters. The protocol offers fixed yield through PT, yield trading through YT, and a more deliberate approach to risk management than most DeFi earn products even try to provide.

Pendle’s own docs describe it as a permissionless yield-trading protocol built on yield tokenization and a dedicated AMM. At the same time, its app guide makes clear that users can buy PT to fix yield, buy YT to increase exposure to yield changes, or provide liquidity around those markets. That gives Pendle a sharper identity than generic lending or farming apps.

Where Pendle falls short is where it becomes impressive: complexity. This is not a clean fit for beginners who just want passive DeFi income without thinking about maturity, implied yield, time decay, or underlying asset quality. Pendle explicitly states that YT loses value after maturity and that users still face third-party protocol risk, even though Pendle is audited. So the protocol is legit and well-established, but it still requires attention, understanding, and greater tolerance for structured DeFi risk than simpler alternatives such as standard lending markets.