As cryptocurrencies like Bitcoin become increasingly popular many people have wondered if it’s worth their time to mine crypto at home. The real question though is whether it’s worth the investment to mine cryptocurrencies at home.

Other than the time spent initially setting things up, your time requirements in mining are quite small, since the computer hardware does all the work.

Sure, you might have some time involved with updating drivers or troubleshooting some hardware or software issues, but the real investment isn’t your time, it’s the cost of the mining equipment, or rig, and the cost of the electricity used to power your mining rig.

So, right from the start I’m going to go ahead and answer the question of whether it’s worth it to mine cryptocurrencies at home. The answer is “Maybe”.

Home Cryptocurrency Mining Considerations

I know that the maybe answer seems like a cop-out, so I’ll explain further.

There are a number of considerations to take into account before you can answer the question of whether home mining is going to be profitable. It certainly can be, but you have to make the right decisions if you want to make money with home crypto mining.

And it’s not likely you’re going to get rich, although you could create a nice little stake, especially if the cryptocurrency you choose to mine increases dramatically in value. So, here are some things to consider:

- Will you use your existing computer equipment, or will you be buying new equipment?

- Which coin will you mine? You can even decide on multiple coins you might mine, and this will affect your decisions regarding what hardware to use.

- Will you be CPU mining, GPU mining or ASIC mining?

- Will you solo mine, or will you join a mining pool?

- Do you even need mining hardware, or are there other alternatives that are acceptable to you?

Can You Mine with your Current Computer

Unless you have a very high end system you won’t have much success in mining. At the very least you’ll need to add additional GPU’s to your system specifically for mining. This is going to mean you’re incurring additional costs, and will extend the amount of time you need to mine before you break even.

If you’re thinking of buying additional equipment you’ll probably want to dig a little deeper before you decide what equipment to buy. This is because your hardware could dictate which coins you can mine.

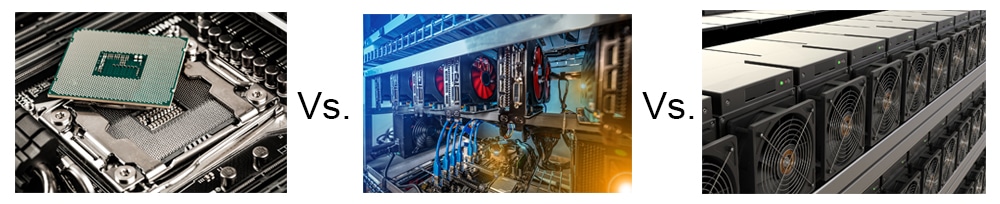

CPU, GPU or ASIC?

CPU mining these days isn’t profitable at all, so you’ll be deciding between GPU mining and ASIC mining. GPU mining has some definite advantages going for it, although an ASIC miner will be far more powerful, giving you the greatest hash power.

If you decide to go the GPU mining route you can start small and scale up later. You’ll want to do your research to see which graphics cards perform best for mining, but with so many to choose from you’ll also be able to balance your costs.

If you’re cash strapped you can start off with cheaper cards, like the Radeon RX 470 or Radeon RX 480, which run around $200 each. As you begin to make profits you can later scale up, adding more graphics cards to your rig, or better performing cards.

Images via Fotolia

Images via FotoliaGPU mining also gives you more flexibility as most cryptocurrencies can be mined using a GPU, although some are certainly more suited to GPU mining. Zcash and Monero are both favorites for GPU mining, and Ethereum is also very popular with home GPU miners.

Finally, you may be able to find used GPU’s at even cheaper prices, lowering your initial investment further. Try looking on gaming sites for cards rather than on cryptocurrency sites, because gamers will tend to sell the cards at lower prices, and you don’t run the risk of buying a card that has already been hard-used for mining, and not necessarily running at its optimum performance.

ASIC mining has the obvious benefit of more raw hashing power. That said, these ASIC rigs are quite an upfront investment, with prices running in excess of $2,000 and up to $5,000+ in some cases. You’ll also have much higher running costs with an ASIC rig as it uses a lot of electricity.

Finally, you lose your flexibility with an ASIC card as each one is made specifically for one coin. And many cryptocurrencies, cannot be mined with ASICs as no card specific to the coin has yet been developed. If all you’re interested in is hashing power though, an ASIC rig is definitely the way to go.

I should also note that even though the ASIC rig is more expensive upfront, you’ll typically recover your initial investment faster with an ASIC card versus a GPU. You can see a comparison of the costs of many popular GPUs and ASICs here. You’ll also get all the relevant information you need to plug into a cryptocurrency mining calculator to determine profitability.

Solo Mining or Pool Mining

Image via bitcoininvestment.news

Image via bitcoininvestment.newsSolo mining is going it alone. The benefit is that you get to keep all the rewards of any block you successfully mine. So, in the case of Bitcoin, if you mine a block, you get to keep the full 12.5 Bitcoin for yourself.

You also get to keep the network transaction fees that are generated. The downside is that your earnings can be very erratic with solo mining. Perhaps this month you mine two blocks – Hooray! – but then you don’t mine another block for several months.

Pooled mining is a protocol that allows miners to “pool” their resources. All the hashing power goes into the same pool. This increases the chance of successfully mining a block. However, any rewards are split between all the members of the pool. Pooled mining can also come with fees, which obviously lower your rewards. And in pooled mining the transaction fees are not distributed.

Other downsides to pooled mining is that it is subject to attacks, such as DDOS attacks, and it can be subject to downtime as well, although it is possible to configure your software to use another pool or solo mine if your main pool goes offline.

The major benefit that keeps most miners in pools is that earnings are more consistent, even if they are lower by 1-2% over time versus solo mining. With pool mining you can be reasonably certain of seeing similar earnings each month, without the huge variation that solo miners are subject to.

One criticism of mining pools is that they centralize mining by controlling so much of the hashpower. For example, back in 2014 the mining pool GHash.io controlled 42% of Bitcoin hashpower. That’s dangerously close to the 51% attack level. Currently the largest pool BTC.com has 27.8% of the Bitcoin hashrate.

There are many different mining pools to choose from. One of the largest is AntPool, which is owned and operated by BitMain, a company that specializes in the development, manufacture and sale of ASIC cards. The oldest and third largest is SlushPool, which has pools for Bitcoin and Zcash currently. You can find pools for many popular coins with a simple Google search.

Alternatives to Home Mining

If all of this sounds expensive and like too much trouble, there are alternatives to setting up your own mining rig at home. One of the most popular is known as Cloud Mining. In cloud mining you contract with another company to lease hashpower.

They setup and maintain all the hardware and all you need to do is pay for the hashrate and collect the rewards. Obviously there are fees involved in this, so it isn’t going to be as profitable as setting up your own mining rig, but it is far less hassle.

One of the largest and most well-known cloud mining companies is Hashflare.io. There you can lease hashrate for Bitcoin, Litecoin, Ethereum, Zcash and DASH mining. The company has been opating since early 2015 and is respected in cryptocurrency circles.

Another choice is Genesis Mining, which offers mining contracts for Bitcoin, Litecoin, Ethereum, Zcash, DASH and Monero. And with Genesis Mining you can switch your hashrate to whichever coin is most profitable at the time. The downside to Genesis Mining is very high contract rates. There’s no way to purchase a small plan here, so expect to spend several hundred dollars at the least. Another downside is that they are frequently out of stock or hashpower, and so you may need to wait to get a contract.

Staking as Mining

Some Coins For Staking

Some Coins For StakingYou might also consider “mining” a different consensus mechanism. For example, coins that use Proof of Stake pay miners who simply hold the coins. Some interesting choices are available for those who would be happier doing their mining simply by holding coins.

One is NEO, which is a good choice because it doesn’t require you to keep your wallet open at all times to collect your rewards, nor does it require you to run a masternode. PIVX and OkCash are two staking coins that are easy to start with as they have no minimum staking requirement.

If you have a substantial amount of money (or have been mining it already), DASH is a hybrid that allows for staking. However you have a minimum of 1,000 DASH coins to run what is called a masternode. At a current price of $439 that means you’d need $439,000 worth of DASH to take advantage of the staking option.

Interestingly, Ethereum is supposed to move to the Casper proof of stake system sometime in 2018, so you could mine it now, and then when it switches over you’d already have some Ether for staking.

In Conclusion

Mining cryptocurrrencies at home can be a fun hobby, a side gig, or a way to make substantial cryptocurrency profits if done correctly and scaled up.

It may not be for everyone, but if you don’t mind the technical nature of building your own rigs and maintaining them, along with configuring the appropriate software for running your rigs, it could be a way for you to build up a stake of your favorite cryptocurrency.

Or you can take the simple route of purchasing a cloud mining contract or coins that work on a proof of stake mechanism. Either requires no additional work on your part, and can yield decent returns.